How To Manage the Risk of PEPs in Banking?

PEP

April 23, 2026

November 18, 2024

- What Does Politically Exposed Person Mean In Banking?

- Why Do Banks Struggle To Manage PEP Risk?

- Which PEP Categories Present The Highest Risk For Banks?

- Global Regulatory Frameworks For PEP In Banking Management

- Major Challenges For PEP Screening In Banking

- Managing PEP Risk Requires More Than Static Screening

“For too long, public figures and their families have suffered discrimination from the banks. This is at least a start in unraveling the debanking scandal that has hurt so many individuals and small businesses. Much more is needed.”

Nigel Farage

Nigel Farage, a prominent public figure in the UK, shares his thoughts on how politically exposed persons are mistreated by the banking sector. But what led him to call out the banking sector so publicly?

Farage personally experienced “debanking”, a practice where financial institutions ban accounts based on political views rather than financial eligibility.

After this incident, a troubling trend emerged where multiple banks stopped offering financial services to individuals based on their reputation or political ideologies.

With the growing number of politically exposed persons in banking, authorities worldwide expect obliged entities to manage PEPs with greater responsibility.

What Does Politically Exposed Person Mean In Banking?

Financial institutions define politically exposed persons as individuals who hold or have held prominent public functions and therefore present higher exposure to corruption, bribery, or misuse of public authority within the banking system.

Regulatory frameworks such as the Financial Action Task Force (FATF), FinCEN under the Bank Secrecy Act, and the UK Financial Conduct Authority require banks to apply enhanced due diligence when onboarding or monitoring such individuals.

In banking operations, politically exposed persons typically include individuals linked to government leadership, judicial bodies, military positions, or state-controlled enterprises. Their financial activity is not considered illegal by default; their positions create higher vulnerability to financial crime risks, which therefore requires continuous monitoring and stronger verification controls.

Banks also treat exposure differently based on jurisdiction. Foreign politically exposed persons are often assessed with higher scrutiny compared to domestic profiles, due to cross-border complexity and limited visibility into the source of wealth.

Why Do Banks Struggle To Manage PEP Risk?

Banks face operational and regulatory challenges when managing politically exposed persons due to the complexity of identifying true risk levels within large and diverse customer bases.

One major difficulty is the inconsistency of data sources used in screening processes. Different vendors and databases often produce conflicting or outdated information, which leads to inaccurate risk classification and operational inefficiencies.

Another challenge arises from the high volume of alerts generated during screening. Large datasets combined with incomplete or outdated records often create false positives, requiring manual review and slowing down onboarding and monitoring workflows.

Cross-border financial activity adds further complexity, especially when dealing with individuals linked to multiple jurisdictions or politically sensitive regions. This limits visibility into beneficial ownership structures and source of wealth verification.

The result is an operational imbalance where banks must balance regulatory compliance expectations with the need to maintain a smooth customer experience and avoid unnecessary account restrictions.

Banks also face reputational and regulatory pressure when managing politically exposed persons, particularly in cases linked to account closures or restricted services. High-profile incidents involving public figures such as Nigel Farage and policy discussions involving figures like Jeremy Hunt have highlighted the consequences of overly cautious or poorly justified decisions.

These cases demonstrate that ineffective PEP risk management can lead to compliance gaps as well as public and regulatory scrutiny.

Which PEP Categories Present The Highest Risk For Banks?

Not all politically exposed persons carry the same level of financial crime exposure. Banks assess risk based on jurisdiction, position, influence level, and financial activity patterns.

Foreign politically exposed persons generally present the highest risk due to limited transparency across international regulatory systems and difficulty in verifying the source of wealth across borders. These profiles often require enhanced due diligence under FATF-aligned frameworks.

Domestic politically exposed persons are also considered high-risk; however, in many jurisdictions, such as the UK and Canada, they are assessed with comparatively lower risk weighting unless additional red flags are present.

Individuals linked to state-owned enterprises or sovereign funds may also present elevated risk due to access to public financial resources and procurement influence.

Close associates and family members of politically exposed persons represent another critical risk category. These individuals are often used to obscure ownership structures or conduct indirect financial transactions that bypass direct scrutiny.

Effective banking risk frameworks, therefore, prioritize dynamic risk scoring instead of static classification to ensure proportional monitoring across all categories.

Given these operational and reputational challenges, regulatory frameworks play a central role in shaping how banks manage politically exposed person risk.

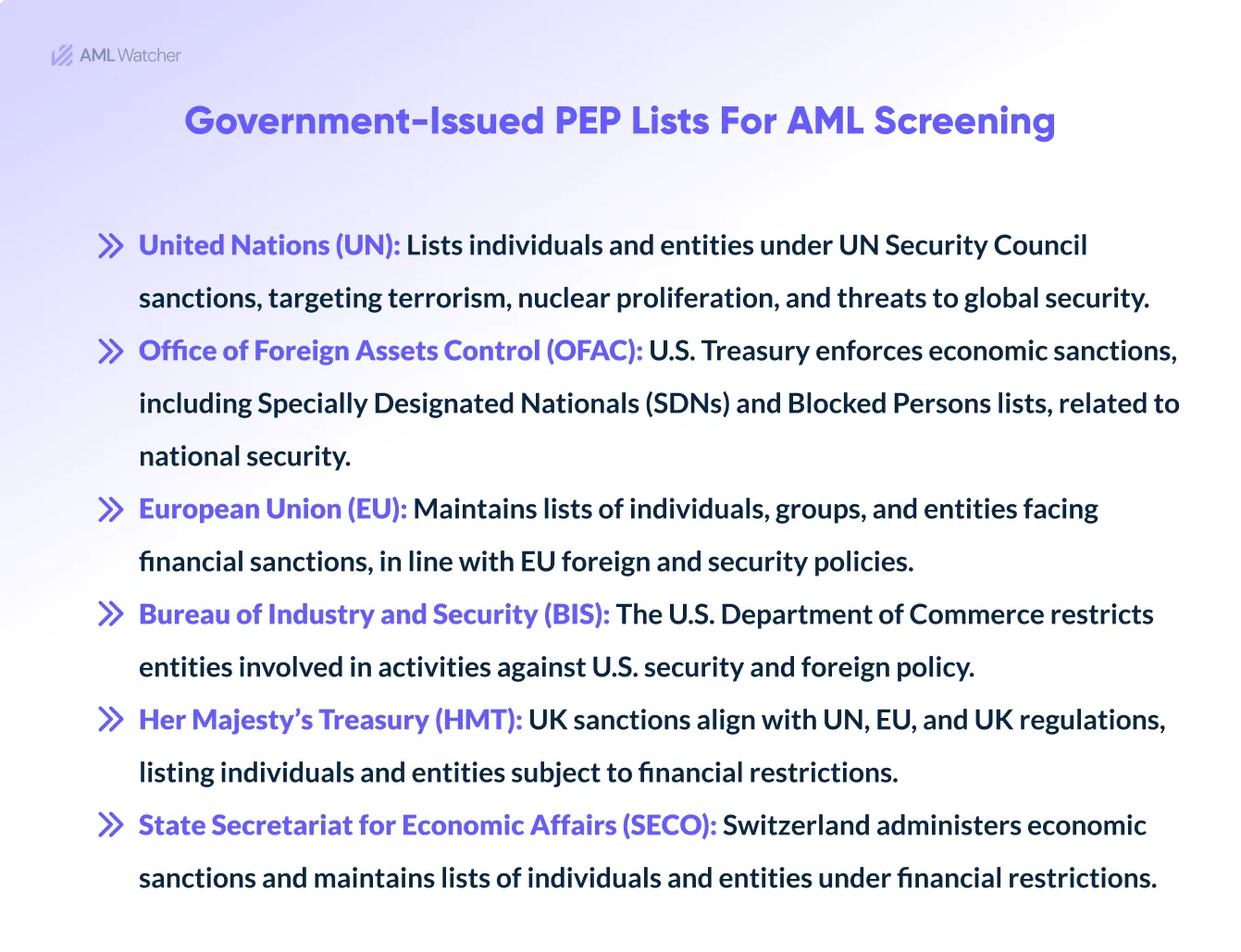

Global Regulatory Frameworks For PEP In Banking Management

The legal landscape for managing Politically Exposed Persons (PEPs) in banking has changed dramatically, with recent legislative updates increasing due diligence obligations.

Notable national regulations and international entities include:

Financial Action Task Force

FATF’s Recommendations 12 and 22 regulate PEP screening, mandating enhanced due diligence to mitigate risks associated with money laundering and terrorism financing.

The European Union

EU’s Directive (5AMLD & 6AMLD) outlines PEPs, with several European nations following the FATF’s recommendations for effective screening.

The United States

FinCEN and OFAC enforce PEP laws under the Bank Secrecy Act and the PATRIOT Act, with additional due diligence and suspicious activity reporting requirements for foreign officials.

Australia

The Anti-Money Laundering and Counter-Terrorism Financing Act (AML/CTF Act) of 2006 requires the identification of PEPs and their families, as well as obliging increased due diligence and comprehensive risk management systems.

The United Kingdom

The Money Laundering Regulations 2017 are in line with the FATF’s definition of PEPs, and the FCA and Joint Money Laundering Steering Group give detailed PEP management instructions.

Canada

The Proceeds of Crime and Terrorist Financing Act of 2001 establishes reporting obligations, with domestic PEPs remaining active for five years after leaving office and international PEPs permanently.

Singapore

MAS Notice 626 mandates increased due diligence for PEPs and their close affiliates to ensure comprehensive risk management.

Middle East and North Africa Financial Action Task Force (MENAFATF)

MENAFATF guarantees that the FATF’s 40 recommendations are implemented throughout the MENA area, with a particular emphasis on PEP inspection.

South Africa

The Financial Intelligence Center Act was revised to include politically influential individuals (PIPs), such as private sector officials involved in public service procurement.

Regulatory guidance emphasizes that financial institutions should adopt enhanced due diligence and effective PEP screening measures rather than relying on account closures as a primary risk response.

Regulatory expectations continue to evolve, requiring banks to strengthen how politically exposed persons are identified, monitored, and risk-assessed across jurisdictions.

Major Challenges For PEP Screening In Banking

PEP screening in banks is necessary for AML compliance procedures, but it poses various obstacles. When not appropriately managed, these issues can increase the likelihood of AML violations and reputational harm. Key challenges include:

Inconsistent PEP Definitions

The lack of a universally accepted definition causes inconsistencies in identifying and monitoring PEPs across jurisdictions. FATF has broader criteria for considering any person as a PEP, whereas the US, UK, Canada, and other countries have different explanations for PEPs.

Limited Jurisdictional Coverage

Effective PEP screening must include PEP data from occupied, controversial, or less-recognized territories; however, many vendors ignore these regions, resulting in significant AML risk management gaps.

Ignoring Close Associates

Effective PEP screening should extend beyond the actual individual to include close acquaintances, including family members and business partners, who could be exploited to avoid detection. Identifying and measuring these people’s risk levels is difficult and resource-intensive.

Outdated PEP Lists

A person’s PEP status may vary over time as they move between politically exposed roles. This delay in changes to PEP lists creates significant hurdles with higher false positives and negative alerts.

Inefficiency Due to Language Barriers

PEP data is available in a variety of languages, complicating cross-jurisdictional coordination and increasing the likelihood of inaccuracies and false positives. Many solution vendors focus on certain locations, resulting in coverage gaps and increased occurrences of missing data or erroneous outcomes.

The Nigel Farage case underscores the risks of debanking clients without a proper risk assessment. Banks should adopt a risk-based approach to AML screening, focusing on actual risks rather than indiscriminately removing clients based on a one-size-fits-all solution.

Managing PEP risks requires more than just basic screening—it demands a dynamic, risk-based approach that is responsive to the changing regulatory landscape.

Managing PEP Risk Requires More Than Static Screening

Banks often struggle with inconsistent data, excessive false positives, and growing regulatory scrutiny when managing politically exposed persons. Without a structured and risk-based approach, these challenges can lead to operational inefficiencies and reputational exposure.

AML Watcher supports financial institutions with advanced PEP screening capabilities designed to improve accuracy, reduce false positives, and provide real-time risk insights across global jurisdictions.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries