Sanctions Screening for NFIs (Non-Financial Institutions): Who Is In Scope Now?

Sanctions

April 1, 2026

For years, sanctions compliance was treated as a banking problem. Banks usually screen customers, freeze assets, and file reports. Non-financial institutions such as real estate brokers, accountants, lawyers, jewelers, and casino operators worldwide largely operated at the margins of the regime. But now that era is over.

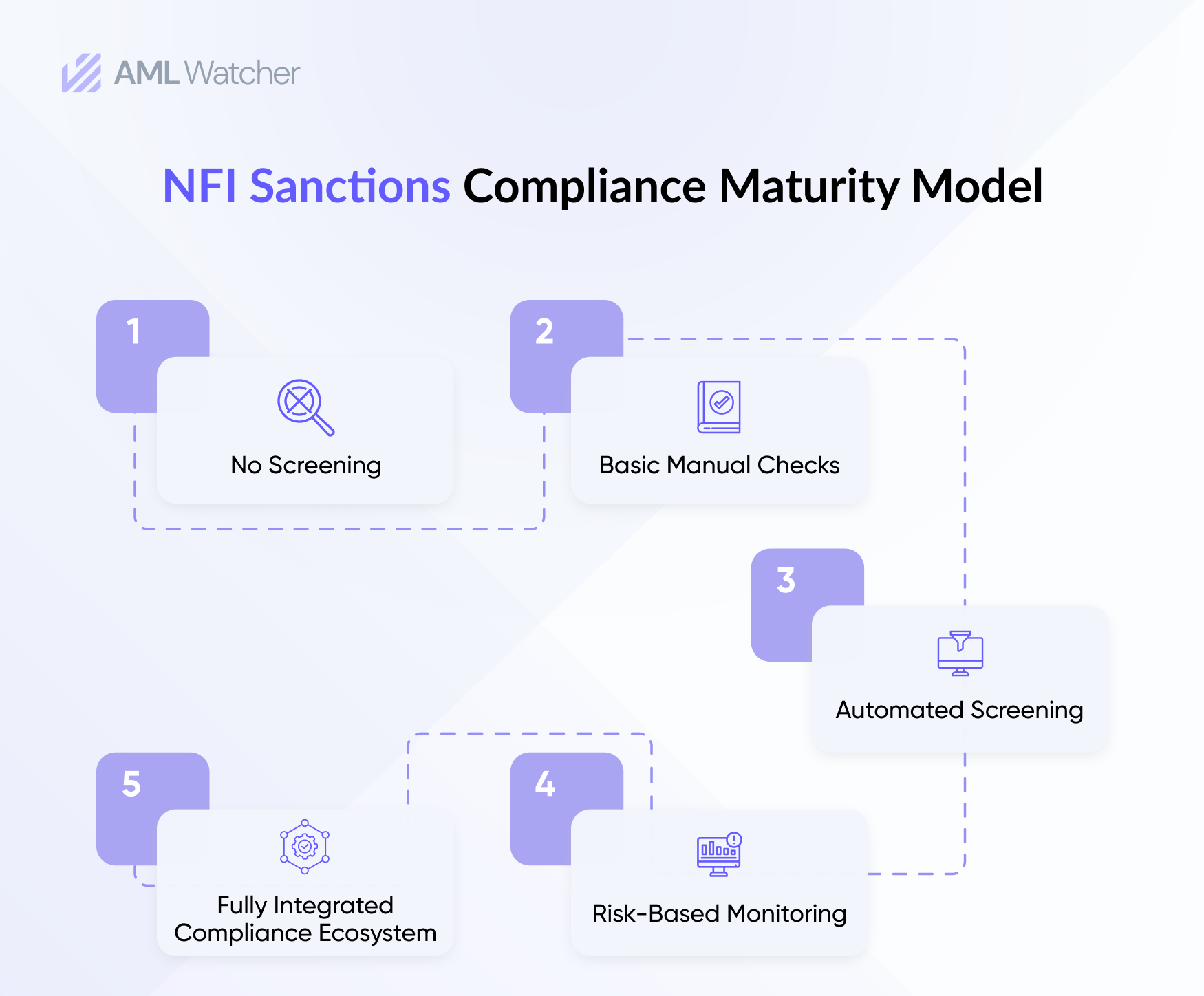

Sanctions screening for NFIs has moved from a best-practice recommendation to a hard regulatory obligation in jurisdiction after jurisdiction. Driven by updated FATF standards, aggressive national legislation, and a surge in enforcement actions, Designated Non-Financial Businesses and Professions (DNFBPs) now face the same compliance expectations that banks have navigated for years, but with much fewer resources to meet them.

This guide explains exactly who is in scope today, what the global regulatory framework requires, where the greatest enforcement pressure is concentrated, and how purpose-built technology can make NFI sanctions compliance for DNFBPs equally attainable and audit-ready.

The Regulatory Pivot: Why NFIs Are Now in the Crosshairs

The traditional boundary between financial and non-financial sector compliance began to dissolve when the Financial Action Task Force (FATF) recognized a simple truth: criminals do not restrict their laundering activity to banks. Real estate purchases, legal structures, precious metals, and trust arrangements all assist as strong vehicles for placing, layering, and integrating illegal income, and they often do so while bypassing the customer due diligence controls that banks routinely apply.

In October 2020, the FATF adopted landmark amendments to Recommendations 1 and 2, formally extending proliferation financing risk assessment obligations to banks and DNFBPs.It also obliged non-financial bodies to actively identify, assess, understand, and mitigate risks associated with evading targeted financial sanctions, i.e., asset freezing and dealing prohibition measures stipulated under UN Security Council Resolutions.

However, during the FATF Plenary held in February 2025, FATF took further steps in this regard by amending Recommendation 1, which obliges financial bodies and DNFBPs to differentiate their approaches based on types and levels of risks they are exposed to, while also requiring supervisors to review risk mitigation approaches to avoid overcompliance. Most notably, however, FATF also affirmed its Horizontal Review of DNFBPs, a risk valuation exercise to assess how effectively FATF countries have implemented AML/CFT regulations for lawyers, accountants, trust and company service providers, and real estate agents, and urged countries to address existing gaps in this regard.

The June 2025 report of FATF on Complex Proliferation Financing and Sanctions Evasion Schemes reinforced the urgency. The report revealed that only 16% of FATF-assessed countries have demonstrated high or substantial effectiveness in applying targeted financial sanctions under UN Security Council Resolutions, a damning indictment of global readiness. With the DPRK-linked ByBit theft of USD 1.5 billion fresh in the enforcement record, regulators are no longer patient with DNFBPs that treat sanctions screening as optional.

Who Is a DNFBP? Understanding the Scope of NFI Sanctions Compliance

The FATF defines DNFBPs in its Glossary, and while domestic implementation varies, the core categories are broadly consistent across jurisdictions. Sanctions compliance obligations apply when entities in these sectors engage in specific, high-risk activities.

Casinos

Casinos are perhaps the highest-risk DNFBP category. The ability to exchange cash for chips and back again creates a natural layering mechanism. FATF Recommendation 24 mandates that casinos operate under a license and apply fit and proper criteria to individuals involved in ownership or management. Sanctions screening is required for all consumers and proceedings that meet threshold triggers.

Real Estate Agents

Real estate is always identified as a high-tier risk in the context of money laundering. The purchase of high-value real estate provides an opportunity for illicit actors to launder large sums of money in a single transaction. In the EU, the CDD, which includes sanctions checks, must be performed by the real estate broker when the client is making a purchase involving cash payments over €10,000. In Australia, the 2025-2026 Tranche 2 AML/CFT reforms clearly include real estate agents as reporting entities, closing the gap that FATF had identified as an issue in its 2015 mutual evaluation report.

Lawyers, Notaries & Independent Legal Professionals

Lawyers have a particularly critical role in the DNFBP structure, where they have the capacity to create shell companies, structure trusts, handle money, and offer guidance in transactions, which could be unwittingly or deliberately utilized for breaching sanctions. AML requirements, in this case, pertain only to situations where lawyers are part of financial or real estate transactions, and not where there is only legal FATF DNFBP guidance or representation in litigation.

Accountants & Auditors

External accountants and auditors who provide tax advice, handle financial data, or audit firms with complex ownership frameworks are squarely within the DNFBP scope. Their position as financial gatekeepers means they are often the last professional line of defense before suspicious funds are integrated into the regulated economy.

Trust and Company Service Providers (TCSPs)

TCSPs’ firms that create or manage legal entities, provide registered office services, or act as nominee shareholders carry heightened risk because of their capability to conceal beneficial ownership. Sanctions screening non-bank is particularly critical here: a sanctioned individual who cannot open a bank account may attempt to route funds through a shell structure administered by a TCSP.

Dealers in Precious Metals and Precious Stones (DPMS)

High-value, portable, and easily convertible, including valuable metals and gems, are ideal for value transfer between jurisdictions. DPMS are in scope for sanctions screening when they engage in cash transactions above applicable thresholds, which differ by jurisdiction but commonly range from USD/EUR 10,000 to 15,000.

Emerging Categories: VASPs and Beyond

As of the 2025-2026 regulatory cycle, Virtual Asset Service Providers are now included in the national DNFBP regulatory landscape in line with the FATF’s updated guidance of October 2020 and subsequent iterations.

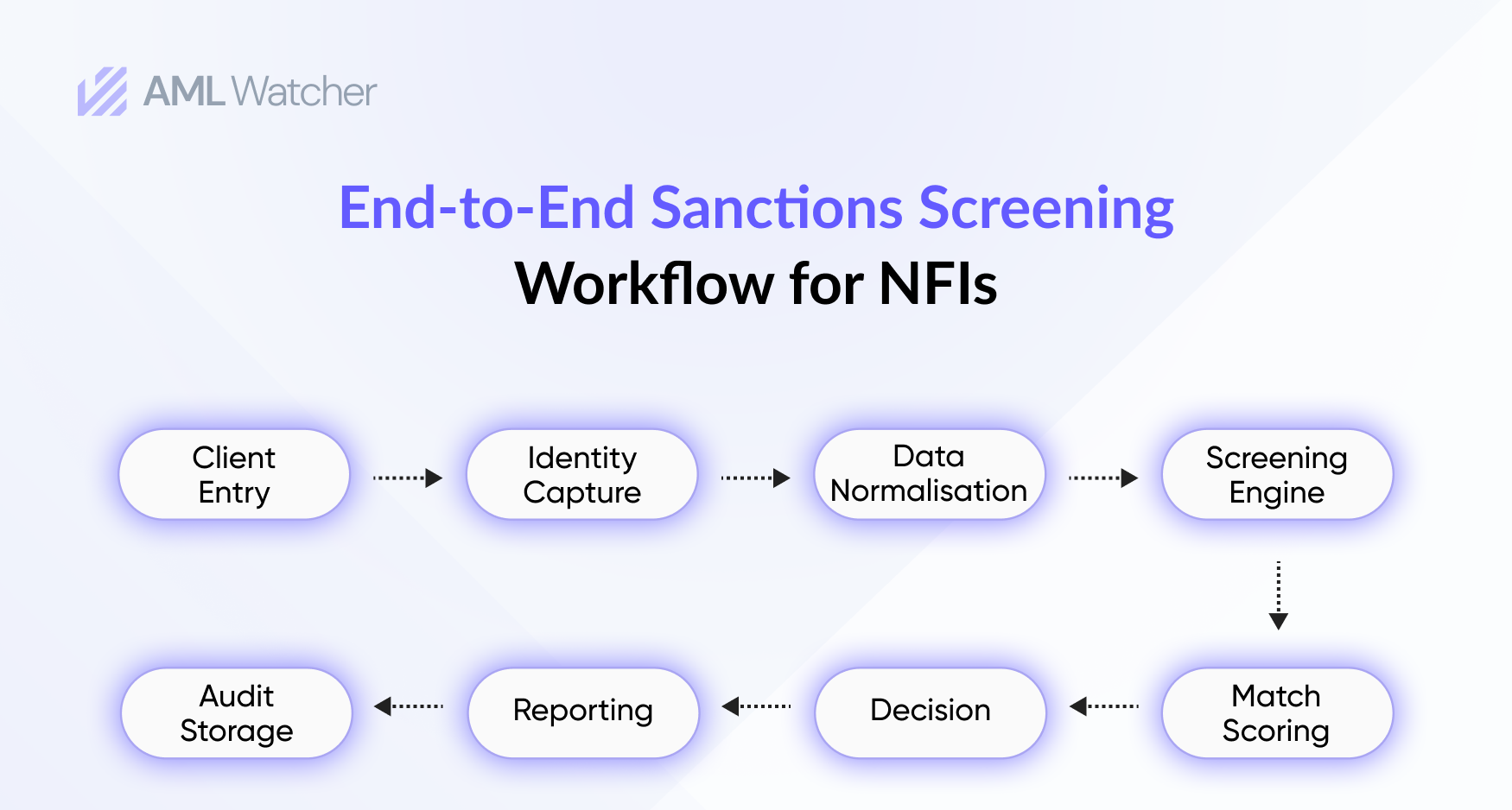

What Does Sanctions Screening for NFIs Actually Require?

DNFBPs’ sanctions screening requirements are similar to those of the financial sector in what they require, with the triggers, supervision mechanisms, and thresholds being the only differences. To comply with sanctions regulations for NFIs:

Customer Screening at Onboarding

All new customers are required to undergo sanctions screening before the onboarding process is complete. This entails checking the customer and, in the case of a corporate customer, the beneficial owner of the customer against consolidated and domestic sanctions lists. An example of a real estate agent’s customer is a corporate structure requiring the real estate agent to look through to the ultimate natural person beneficiary.

Ongoing Monitoring

While a one-time process might be enough, there needs to be constant awareness that there are constant updates in sanctions lists. It is possible for fresh designations to be made, either by OFAC, the UN, the EU, or domestic regulators, at any given time. It is critical, therefore, for DNFBPs to ensure that if one of their existing clients has been subjected to a sanction after the establishment of a relationship, there are mechanisms in place to identify this.

Transaction-Level Screening

Transaction-level screening is important for DPMS and casinos, especially with regard to cash and high-value dealings that trigger the threshold. It is not sufficient to only perform name matching against the sanctions lists. It is important to be able to perform counterparty and entity screening.

Beneficial Ownership Verification

FATF Recommendation 10 is applicable to DNFBPs through Recommendation 22. It is important to identify the Ultimate Beneficial Owners (UBOs) and to verify these UBOs against the sanctions lists. Beneficial ownership verification is non-negotiable for the compliance of the DNFBPs. Shell companies and nominees do not excuse the liability of the DNFBPs if the underlying sanctioned party can be identified.

Record-Keeping

All results of the screening processes, CDD records, and transaction records must be maintained for at least five to six years. They must be producible on demand.

SAR/STR Reporting

Where a DNFBP compliance obligations identifies a match or a credible suspicion of sanctions evasion, it must report to the relevant Financial Intelligence Unit (FIU) without tipping off the customer. Failure to file a Suspicious Activity Report (SAR) or Suspicious Transaction Report (STR) is itself a criminal offense in most jurisdictions.

How AML Watcher Supports Sanctions Screening for NFIs

AML Watcher is designed to make sanctions screening simple, accurate, and reliable for DNFBPs and other non-financial institutions. It aggregates global and local sanctions lists, which are frequently updated, to help you stay compliant and avoid critical risks. Sophisticated name matching minimizes the risk of overlooking hidden connections, even in different languages and spellings. The ability to easily categorize sanctions means that decision-making can be made more quickly and with confidence.

With AML Watcher, which offers integrated screening for sanctions, PEPs, and adverse media, there are no gaps in screening, which can be the case when relying on standalone solutions. Batch screening and API integration make it easy to screen large numbers, and existing workflows can be integrated. With built-in reporting, AML Watcher ensures that all screening activities are fully audited and compliant.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries