Why a Due Diligence Checklist is Essential for AML Compliance and Risk Management?

AML Compliance

January 1, 2025

Did you know the German payment processor Wirecard AG was involved in a huge financial scam known as the Wirecard affair?

Two Ex Wirecard executives “Alexander von Knoop and Susanne Steidl” have been accused of approving risky loans without implementing proper due diligence that shows the significance of customer due diligence compliance checks in the prevention of financial crimes.

Back then, in December 2019, they approved “€40 million loans” in just an hour upon a baseless email, and they did the same in March 2020 when they approved another loan of “€100 million” to a company that was already in deep debt.

Wirecard went bankrupt in June 2020 when the company admitted that “2 billion in cash never existed.” This loss caused the company reputational damage, and they lost a huge amount of investors.

This case highlights the need for a “rigorous due diligence requirements checklist” to confirm customer identities, evaluate financial transactions, and monitor risks associated with economic crimes. Thus, a due diligence checklist preserves the integrity of the business.

Donald Trump has been accused of misprinting the worth of his assets to obtain better loans from his primary lender “Deutsche Bank.” The bank had not properly conducted due diligence checks and got caught in legal trouble.

Financial institutions must check their customers’ identities, screen their profiles regularly, and monitor the purpose of the business relationship to evaluate the risks associated with financial crimes like money laundering (ML) and terrorist financing (TF).

Read this Article to find out how due diligence and Screening of customers is essential to ensure robust AML compliance.

What Is Due Diligence?

Due diligence meaning is, “the organized process of screening the profiles of customers by implementing AML/KYC (Know Your Customer) measures, evaluating financial risks associated with customers by analyzing their transaction patterns, and categorizing them on high, medium, or low levels.”

The goal of conducting due diligence is ensuring regulatory compliance by complying with AML laws and local and international standards “such as FATF recommendations or EU directives.”

Non-compliance leads to legal consequences, hefty fines, and damage to a business’s reputation.

The ongoing due diligence requirements checklist covers other practices, such as performing adverse media screening to detect negative news indicating businesses or entities are linked with illicit activities.

Monitoring transactions to identify unusual transactions is necessary so reporting of suspicious transactions is essential. Update and review customer profiles regularly to account for changes in risks.

What is a Due Diligence Checklist?

Financial institutions ensure AML compliance and mitigate financial risks by implementing a due diligence checklist. It lists key steps, such as

AML due diligence checklist covers the following steps :

Conduct a Risk Assessment

- According to FATF recommendation 1, follow a risk-based approach.

- Identify the risks associated with clients and understand thoroughly to mitigate the risks.

- Assess risks associated with the client by monitoring their transaction patterns.

- Establish how many risks organizations can take according to their business goals.

- Flag unusual transactions that deviate from known legitimate practice.

- Define specific transaction limits; after exceeding the transaction, alerts will be generated.

Internal AML Policies

- Establish a document on AML compliance practices and identify the gaps in internal AML policies.

- Develop clear procedures for monitoring transactions and reporting suspicious transactions.

- Hiring skilled AML professionals to ensure robust AML compliance.

Watchlist and Sanction List Screening

- Screen clients against AML Watchlists and international sanction lists such as OFAC and UNSC.

- Update data by using automated screening tools to address changes.

- Take Actions accordingly to manage risks.

Customer Due Diligence (CDD) and Enhanced Due Diligence (EDD)

- Implement CDD measures to verify the identities of clients using reliable sources.

- Perform Enhanced Due Diligence (EDD) for high-risk customers.

- Asses risks by evaluating the profiles and transaction patterns of clients.

Transaction Monitoring and Reporting

- Monitor financial transactions regularly.

- Identify unusual patterns in transactions.

- Report suspicious transactions when

- Transactions exceed the predefined threshold

- Unusual patterns are detected while dealing with PEPs

- Found negative information through adverse media screening

- Dealing with High-risk countries and mitigating the risks.

Conduct Regular AML Training

- Conduct AML training for staff and compliance officers to make them aware of ML/TF risks.

- Train employees to adopt legislative updates and regional AML regulations.

Report Suspicious Activities

- Detect unusual transaction patterns and file a suspicious activity report (SAR)

- The report will include “Organizational details, Transaction information, Justification for suspicion, and Relevant activities under scrutiny.”

This promotes transparency in business and protects it against financial crimes.

Who is Obligated to Conduct the AML Due Diligence Checklist?

Financial Institutions, Designated Non-Financial Businesses and Professions (DNFBPs), Cryptocurrency, and FinTech Companies are obligated to conduct a due diligence checklist to ensure compliance with AML regulations.

“Conducting thorough due diligence money assessments is essential to ensure compliance and mitigate risks associated with financial crimes.”

Due diligence processes have three types: Simplified Due Diligence (SDD), Standard Due Diligence, and Enhanced Due Diligence (EDD).

The compliance officer decides what type of due diligence will be applied according to customer risk levels.

-

Simplified Due Diligence (SDD)

Customers that pose low or no risks can be verified through simplified due diligence.

Basic Detection

Collect necessary and basic information for the detection of customers.

- Such as the full name and date of birth of individuals involved in transactions.

- for example, collected registered business names for entities

- Verify the identity of individuals through the government-issued ID

- For entities, check the registration documents of the company

Risk-Based Assessment

Evaluate the client’s risk profile based on pre-existing “low-risk criteria.”

- Such as living or working in a country that poses low risk

- Involving in a transparent transaction

- Publicly Listed in a well-known company and has “well-regulated reporting.”

Simplified Screening

Cross-check information against “global databases, public registers, and other reliable sources.”

Ongoing Monitoring

Regularly perform checks to ensure the client is on the same level of risk over time. Monitor transaction activities throughout the business relationship to determine if any risk profile changes are detected.

Even in SDD, adverse media screening or AML transaction monitoring is conducted to flag unusual activities.

-

Customer Due Diligence (CDD)

The collection of information for detecting a customer’s name and evaluating the financial risk associated with a client is called Customer Due Diligence (CDD).

Basic requirements

- Check the information using official papers “such as Driving licenses, Passports, and Utility bills.”

- CDD is a basic requirement for the KYC process. KYC is required in business to understand who their customer is and what kind of and how much risks they can pose.

As a part of AML/CFT legislation, all FATF members must implement CDD measures as it is obligated under “FATF Recommendation 10.”

Risk Assessment and Record-Keeping

After detecting customers’ identities, categorize the clients according to their risk levels.

- Maintain the record for at least five years in AML software.

- So future regulatory checks and audits can access it easily.

- Meet the requirements mentioned under FATF’s recommendation 10

- Grant access to this information upon request

Need for Enhanced Due Diligence (EDD)

Determine the need for EDD while dealing with high-risk clients such as “politically exposed persons (PEPs) or sanctioned individuals/entities.”

Ongoing Monitoring and Reporting Suspicious Transactions

Regularly checking the business relationship to assess the risk levels and changes in client information. Identifies unusual patterns in transactions to mitigate the risks on time.

Report suspicious activities to FIU and do not disclose the information to clients they submitted SAR.

-

Enhanced Due Diligence (EDD)

EDD covers additional measures to assess high-risk clients like PEPs and sanctioned persons. Monitor transactions to evaluate financial risks like “money laundering or terrorism financing (ML/TF).”

FATF Recommendations

According to FATF Recommendation 19, EDD measures for transactions linked to high-risk clients or countries should be implemented.

- Collect more information from liable sources for screening of clients’ profiles.

- Through extra steps, verify the source of funds (SOF) and source of wealth (SOW).

- Get additional details related to the business to learn its nature and purpose.

- Obtain authentic information related to beneficial owners.

Risk-Based Measures

- Customize the EDD measures according to the risk level a client may pose

- Thoroughly examining the purpose of business to promote transparency

- Conduct ongoing transaction monitoring to determine any change in their risk level.

- Monitoring transactions may indicate new risks or detect suspicious activities.

Record Keeping

The 11th recommendation from the FATF requires the implementation of measures for record-keeping.

- Maintain a Record of Client’s transactions for at least five years

- Provide the record upon request and for audits.

Adverse Media Screening

- Adverse media screening allows you to get information related to clients

- Sources like news articles or any other platform provide data

- Thus, the risks associated with them can be identified.

EDD for High-Risk Clients and Industries

According to “Article 18 of 4AMLD,” EDD measures are required for high-risk individuals like PEPs and high-risk countries in Europe.

Global AML Legislation Related CDD and EDD

The requirements for CDD and EDD, which are components of due diligence checklists, vary across different countries due to differences in AML regulations.

However, they all generally coordinate with international standards set by the Financial Action Task Force. AML legislation related to CDD and EDD in different countries is explained below:

United States

In the U.S., AML regulations are implemented in financial institutions by complying with the “Bank Secrecy Act (BSA) and the USA PATRIOT Act.”

Financial institutions are mandated to include CDD measures in their AML programs.

- Verify the customer identities by collecting reliable data

- Understand the nature and purpose of the business relationship

- Perform ongoing monitoring to report suspicious transactions

EDD measures are implemented for

- Higher-risk clients, such as PEPs

- Clients that are linked with higher-risk countries

- FinCEN supervises the implementation of these acts.

European Union

The EU has also established centralized registers of beneficial ownership information to aid CDD processes. The EU follows AMLD directives for implementing AML regulations in their financial institutions to prevent financial crimes.

The sixth AML Directive (6AMLD) is the latest and updated directive. According to AML legislation in the EU, obligated entities must perform CDD measures while

- Starting Business relationships

- Dealing with High-value transactions

- Detecting Suspicious transactions

EDD measures are conducted when

- Deals with risk clients like PEPs

- Enages with High-risk countries

- Huge transactions are involved

The EU has created a “centralized register of beneficial ownership information” to assist in fulfilling the requirement of a due diligence checklist.

United Kingdom

According to UK’s Money Laundering Regulations 2017,” CDD and EDD measures are mandatory. CDD is applied to transactions that have low risks.

EDD is applied to high-risk countries and clients. Higher-risk countries are identified by authentic sources such as FATF’s grey list and black list.

Australia

The AML regime in Australia is followed according to the “Anti-Money Laundering and Counter-Terrorism Financing Act 2006.”

AUSTRAC supervises AML compliance in financial institutions and mandates CDD to verify customers’ identities and implement EDD measures for high-risk countries and clients.

Germany

The AML Regulatory body in Germany is “The Federal Financial Supervisory Authority (BaFin).”

The act followed is“Germany’s Anti-Money Laundering Act (GwG),” which works per EU directives.

A risk-based approach is followed. EDD is applied for “PEPs, clients from high-risk jurisdictions, or unusual transactions.”

Singapore

In Singapore, obligate entities are required to comply with the “Corruption, Drug Trafficking, and Other Serious Crimes Act (CDSA) and Mutual Assistance in Criminal Matters Act (MACMA).”

According to these laws, CDD and EDD measures are implemented when conducting the AML/KYC process. Recently, AML regulations have been strengthened by the Inter-Ministerial Committee (IMC) of Singapore.

Simplify Your Due Diligence Checklist with AML Watcher

AML Watcher simplifies due diligence by offering innovative AML screening solutions to ensure compliance with Anti-Money Laundering (AML) requirements.

From real-time watchlist checks to continuous monitoring, it provides institutions with the tools they need to spot threats, expedite AML compliance, and remain ahead in the fight against financial crime.

It offers:

1. Comprehensive Data Coverage

Access to over 200 global sanctions lists, including OFAC, EU, UN, and HMT, to ensure full compliance across diverse jurisdictions.

This comprehensive sanction data coverage empowers organizations to confidently screen high-risk entities and maintain alignment with international AML regulations.

2. Extensive Watchlist Screening

Detects high-risk persons and businesses by screening against over 1,300 official watchlists, which include enforcement lists, fugitive lists, debarment lists, and more.

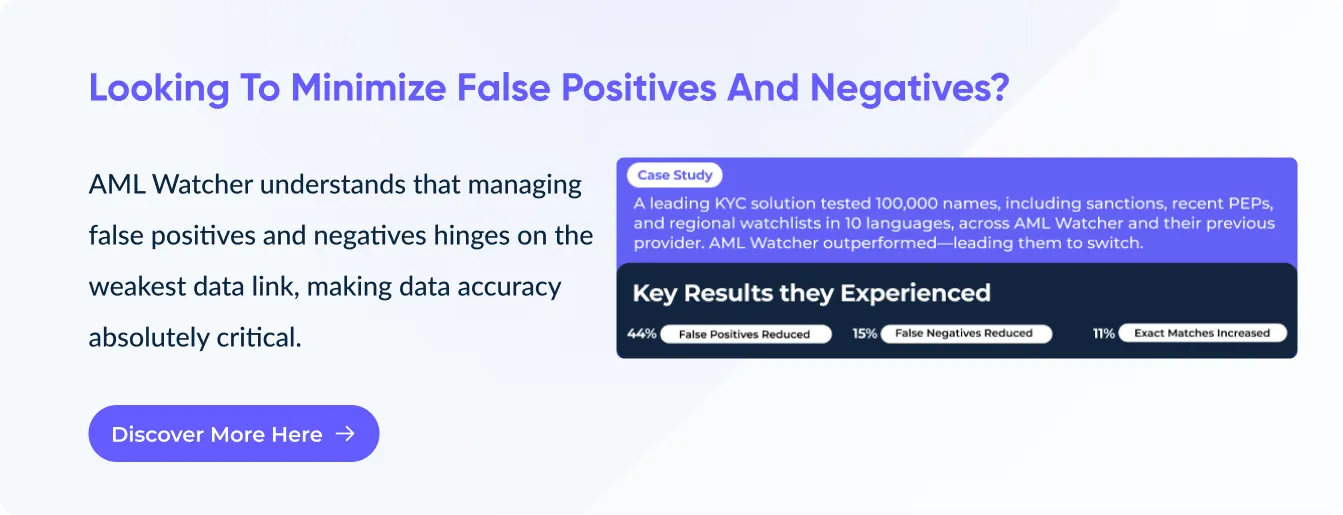

3. Adverse Media Screening

Monitors over 5,000 credible news sources worldwide, using intelligent tagging and natural language processing (NLP) to discover unfavorable news about customers, assisting in early risk assessment.

4. Politically Exposed Persons (PEP) Screening

PEP screening streamlines due diligence by providing universal PEP definitions and risk categorization into PEP risk levels 1–4.

It is tailored to populations of less than 100,000 and enables quick risk assessment, allowing firms to prioritize high-risk situations while meeting compliance requirements with confidence.

5. Advanced Biometric Screening

Incorporates biometric data matching, combining name, image, date of birth, and unique identifiers to enhance accuracy in client verification and reduce false positives.

6. Configurable Risk Scoring

Offers customizable risk scoring models, allowing institutions to assign risk levels during Customer Due Diligence (CDD) and Enhanced Due Diligence (EDD), aligning with specific compliance policies.

7. Ongoing Monitoring and Alerts

Provides continuous monitoring of client activities, with automated alerts for any changes in status or new risk factors, ensuring proactive compliance management.

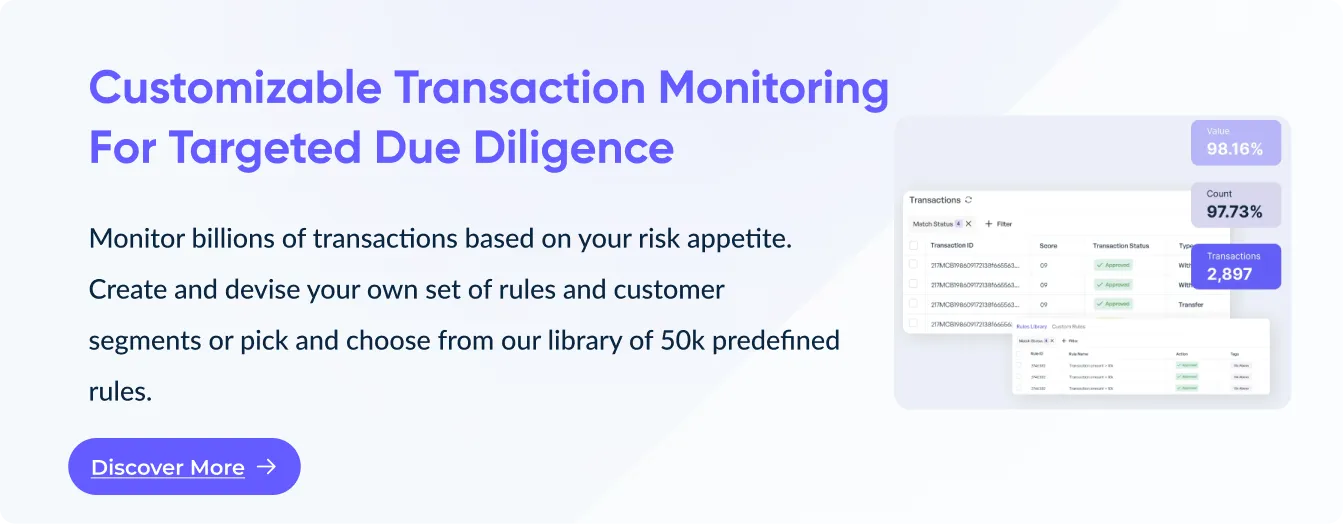

8. Transaction Monitoring

AML Watcher delivers real-time insights into client transactions, allowing for the early discovery of anomalous patterns or behaviors that might suggest financial crime.

- Customizable Rules: The platform uses an intelligent rules-based system with basic, aggregate, behavioral, and risk pattern rules that can be adjusted to analyze AML/CTF risks relevant to your business activities.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries