Guide to Enhanced Due Diligence (EDD) in AML For High-Risk Customers

Due Diligence

August 2, 2024

Implication of anti-money laundering and combating the financing of terrorism (AML/CFT) laws are not limited to financial institutions (banks) only.

But, the regulatory tsunami is engulfing businesses that deal with financial and investment advisers for instance.

Enhanced due diligence (EDD) in AML is a savior for businesses in this war of tug between financial fraudsters and global watchdogs.

Endorsing the identification and verification of clients, the Director of SEC (Security and Exchange Comissions) issued an official statement a few days ago:

“The SEC’s rule requires that investment advisers establish, document, and maintain a written customer identification program (CIP) as part of an AML/CFT program. The CIP must include procedures for verifying the identity of customers that allow the investment adviser to form a reasonable belief that it knows the customer’s true identity.”

He added, “This is essential to prevent criminal enterprises and sanctions evaders from using investment advisers as a gateway to the U.S. financial system and as a means of circumventing the safeguards in place at banks and broker-dealers and avoiding detection of illicit activities.”

The effectiveness of any AML/CFT program relies on the functionality of AML risk assessment and EDD processes.

At this point, I assume, we are aware of the term due diligence that literally means knowing and verifying your clients or business partner to ensure stability of financial systems.

One might ponder on questions like what is enhanced due diligence, what are enhanced due diligence attributes and how to employ EDD compliance when corrupt actors are all about inventing advanced and sophisticated tactics to bug the financial ecosystem.

This article will briefly answer these questions while offering an insight on the plausible solutions to meet increasing regulatory demands and protect the business from bad guys.

What is Enhanced Due Diligence?

Enhanced Due Diligence is a risk-based strategy for customer identity verification. This is one of the elements of the KYC (Know Your Customer) procedure ensuring your clients are not involved in any suspicious activity such as terrorist funding, money laundering, and associated predicate crimes.

In simpler words EDD meaning, is more of an extensive screening into a potential business relationship, investment, or successful transaction.

This procedure involved a detailed review of the financial, legitimate, and regulatory content of the subject along with other aspects such as user character and reputation.

EDD in AML is usually executed when the risk is associated with a transaction or when the client carries higher AML risks such as politically exposed persons (PEPs) and individuals from sanctioned countries.

Implementation of increased scrutiny measures enables businesses to protect customer relationships and investments.

It is recommended to apply a risk-based approach while orchestrating AML/CFT controls and policies within a compliance framework.

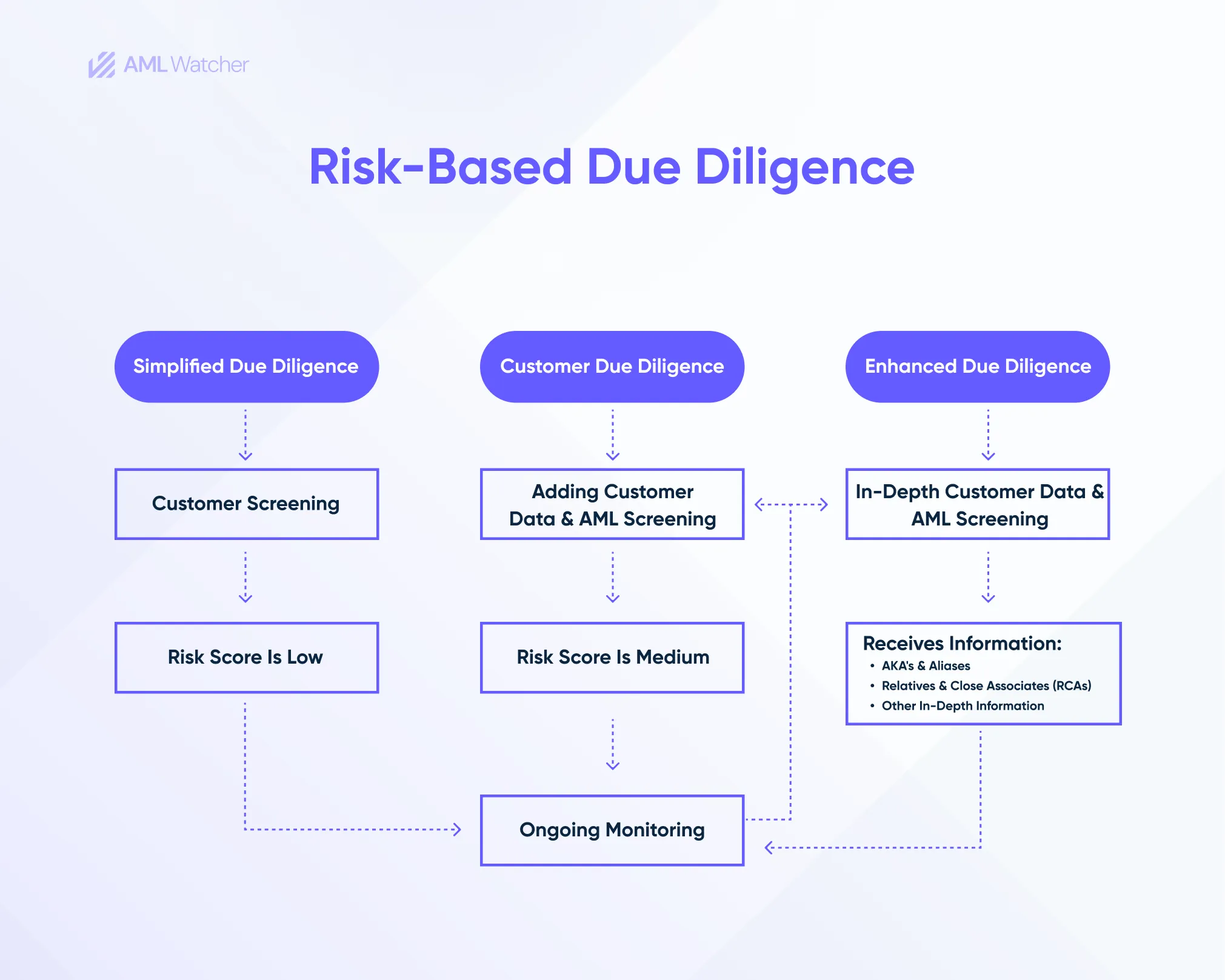

Based on various AML risk factors, due diligence is categorized in three sections.

Three Types of Due Diligence You Should Be Aware Of

Simplified due diligence (SDD) and customer due diligence (CDD) is followed by the high-level scrutiny measures, enhanced due diligence. The only thing that draws a thin line among all three is the customer risk profile.

Simplified Due Diligence: Low-Risk Category

Simplified due diligence in AML compliance is the lowest or minimum level of investigation that is required to be conducted during onboarding a new client.

This type of diligence is applied when the risk scores of financial crimes are lower. The purpose of SDD is to verify customer identity and evaluate any possible risks associated with them.

Customer Due Diligence: Medium-Risk Category

Medium risk customers are assessed and verified by implementing customer due diligence that is the most common and standard compliance protocol.

This procedure involves collecting user information and investigating it to verify customer identity and associated risk against elevated factors.

Global regulatory bodies enforces institutions particularly financial institutions to conduct CDD as an integral part of compliance framework while dealing with low to medium risk jurisdictions.

Increasing compliance challenges are taking a toll on financial sustainability. Learn how CDD in AML helps businesses to overcome regulatory burden.

Enhanced Due Diligence: High-Risk Category

As discussed earlier, EDD for businesses highlights the cruciality of assessing money laundering risks in the AML regime.

Powered by a risk-based approach, enhanced due diligence in AML is all about incorporating anti-money laundering measures into corporate social responsibility policies.

In addition to employing due diligence motivated by various financial risk levels, globally recognized financial intelligence units require businesses to empower AML regimes with ongoing monitoring to stay alert of risk dynamics.

Entangled amidst the financial and regulatory chaos, businesses must develop a clear understanding on when to unlock a particular compliance weapon, dubbed as integrity risk management.

Five Key Areas Where EDD is Required

For more than two decades, regulatory and law enforcement bodies have come up with unified efforts to counter predicate crimes and encourage financial service providers to adhere to AML laws for a sustainable financial system.

EDD requirement is to implement curated measures in the following circumstances, extendable to areas where required otherwise.

- A new customer applies for a service or product from the company or requests to open a bank account.

- If the client is recognized as PEP and RCA in these circumstances the possibilities of the customer being involved in money laundering or corruption are higher.

- When there’s a risk of money laundering like an anonymous transaction without any specific reason.

- In case the user provides incorrect information or stolen identification documents to the financial institution during the onboarding process.

- If the client has connections with higher-risk organizations such as gambling or mass proliferation industries.

PEPs and RCAs can taint the integrity of financial systems like no one else, revealed in the biggest leaks of history. Lift the curtain off the Panama Papers Leak with endorsement of enhanced due diligence in the AML regime.

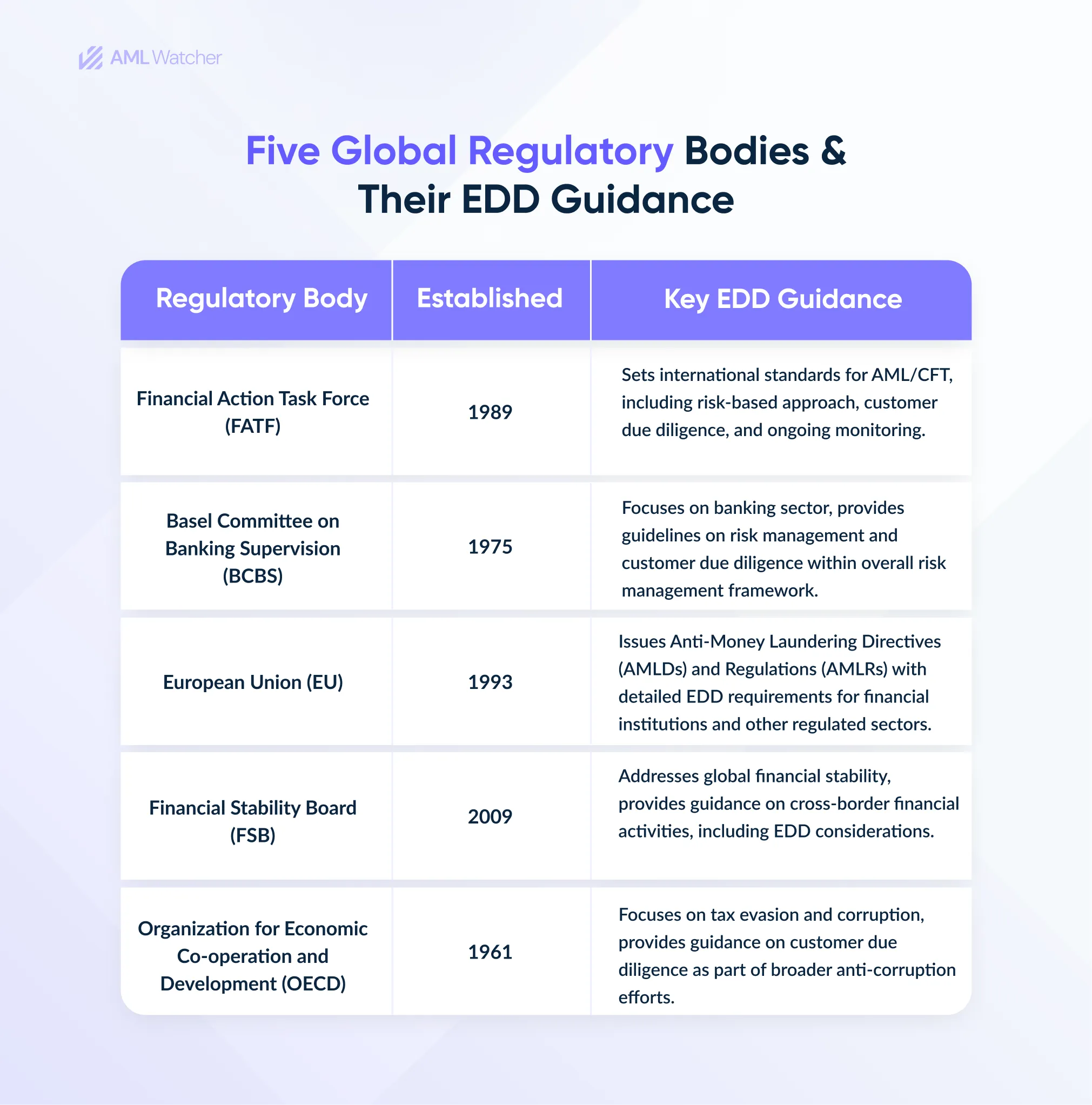

Before delving into critical aspects of EDD checks and specific measures, let’s take a look at the globally recognized regulatory bodies who offer guide on standard EDD practices.

5 Regulatory Bodies Governing EDD in AML

Encouraging the consultation for EDD compliance on specific AML risks, the regulatory guidelines may vary based on business nature, jurisdictions, and geographic location where it operates.

Below are globally recognized regulatory bodies addressing the need for EDD and AML measures.

- FATF (Financial Action Task Force)

- EU (European Union)

- Financial Stability Board

- OECD (Organization for Economic Co-operation and Development)

- Basel Committee on Banking Supervision

If someone thinks that these guidelines are just for paper then think again because failure to meet regulatory expectations and closing eyes to implementation of EDD/AML measures has cost businesses legal, reputational, and monetary consequences.

Being aware of the importance of EDD in AML is crucial but knowing how to implement the EDD measures will protect your business from getting into non-compliance wrath. Let’s dig into them.

7 Specific Measures for Enhanced Due Diligence in AML

Financial institutions can build strong resistance against fraudsters from exploiting global financial systems through money laundering and associated predicate crimes. It takes accountability for EDD compliance and below mentioned measures.

Enhanced Customer Identification

Other than conducting KYC, businesses exposed to higher AML risks are required to collect customers’ information relevant to their business nature, source of wealth, and transactional activities and patterns.

Verification of such information can be done by utilizing local and national databases while detecting red flags can be empowered by advanced data analytics.

Beneficial Ownership Verification

Crucial to adhere to BOI (Beneficial Ownership Information) rule set by the FinCEN (Financial Crimes Enforcement Network), businesses are obliged to acquire ultimate owner information of client or business partner by using reliable resources.

It is crucial to navigate complex ownership structures particularly when money laundering through Shell Companies is taking a toll of AML laws.

Ruling over all white-collar crimes, illicit financial activities through letterbox companies are polluting financial landscapes. Dig into the details on how money laundering works through Shell Companies.

Geographic Targeting

Jurisdictions with compromised EDD/AML laws shine bright in FATF’s grey and black lists. Business with entities from such high-risk regions requires extensive scrutiny measures.

EDD due diligence must be taken in place before developing a business relation with jurisdictions having weak anti money laundering controls. The guidelines suggest considering corruption indexes and unstable political patterns of countries in the EDD/AML regime.

Politically Exposed Persons (PEPs)

Political exposed persons are privileged with public offices having more power and potential to exploit the loopholes and be involved in illicit financial activities.

The higher AML risks associated with PEPs require businesses to employ critical EDD measures including taking approval from upper management before developing partnerships with them. PEP screening is not the only thing that requires it to be done but their RCAs should be screened and observed through ongoing monitoring.

Customer Risk Rating

Effective EDD in AML requires businesses to develop customer’s risk profiles based on various risk factors including location, business type, transactional behaviors, and public status.

These risk profiles must be updated from time to time so not a single red flag goes unnoticed. An effective EDD in business can be measured through the risk profiles of the customers.

Ongoing Monitoring

Once the initial due diligence has been performed, functional AML controls require businesses to monitor clients and partners on a continuous basis.

Ongoing monitoring and periodic reviews allows businesses to proactively catch changes in risk profiles and detect AML red flags.

Documentation & Reporting

EDD in AML compliance does not stop at screening and monitoring potential risks but requires businesses to maintain clear records of the enhanced due diligence process and collect trails of reviews and reports on suspicious financial activities.

Collection and maintenance of compliance reports can be achieved by leveraging efficient risk assessment systems.

Let’s Wrap It Up

Whether you own a startup that struggles to thrive in the global market or an enterprise dreaming to touch heights while not compromising on integral compliance requirements, a reliable AML compliance partner is the key to a transparent future.

EDD and AML regimes are not as scary as it sounds because if you find it hard to find your way around intricate compliance measures, your compliance partner will.

To help you overcome regulatory and technology challenges, AML Watcher brings you a realistic and simplest compliance solution with its carefully collected authentic and reliable dataset that empowers EDD checks.

Contact compliance experts at AML Watcher to streamline your compliance processes.

Frequently Asked Questions

Key Factors that Demand Enhanced Due Diligence

Different attributes of a customer can influence the decision whether to apply enhanced due diligence. The following is a list of key attributes used to identify high-risk customers for enhanced due diligence monitoring:

- Customer Type: Politically exposed persons (PEPs), high-net-worth individuals (HNI), non-resident or offshore companies, non-profit organisations (NPOs)

- Geographic Risk: Customer resident or registered in a high-risk country, Ties to sanctioned countries)

- Nature of Business: Dealing in virtual assets, cash-intensive business, complex corporate structure, import/export businesses)

- Customer Behaviour: non-cooperative and evasive, third-party transactions, structuring

Some sectors like cryptocurrency providers, high-value dealers, real estate, art participants, and company formation service providers, etc., are generally considered to be higher risk. Especially, the real estate sector is likely to attract enhanced due diligence due to involvement in large value transactions, the ability to purchase through complex corporate structures, and cross-border investments.

The frequency of getting KYC for high-risk customers as an EDD typically involves updates at least annually, and on an ongoing basis as soon as red flags or discrepancies are detected.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries