What UK AML Regulations Are Really About?

Sanctions

February 21, 2025

Do you know money laundering is estimated to cost about £255 to every household in the UK each year?

This issue not only impacts household finances but also enables criminals to profit from their illicit actions, which can affect the overall financial system.

As the world’s largest financial metropolis, the United Kingdom’s financial system handles trillions of pounds in transactions annually.

Given its highly developed industry, the British financial markets are vulnerable to exploitation by individuals laundering illicit funds from both transnational criminals and state actors.

As per the World Bank rankings, the United Kingdom has a GDP of $3.1 trillion (2022), making it the sixth largest economy in the world.

In the United Kingdom, the city of London alone manages $3.8 trillion in daily FX transactions, accounting for more than one-third of all global trades. This is greater than the three largest centres Hong Kong, New York, and Singapore combined.

Every year, approximately £100 billion is laundered through and across the United Kingdom by UK-registered corporations.

Currently, the government lacks an exact understanding of the extent of financial crimes like high-end money laundering, terrorist financing, corporate fraud, tax evasion, etc. due to the hidden and cross-border nature of these crimes.

Large amounts of illegal money passing through the UK may result in criminal and regulatory penalties levied by UK, EU, and US authorities. This might result in large financial firms withdrawing from the country or the eventual collapse of its regulated financial industry.

A National Crime Agency report on National Strategic Assessment estimates that the UK’s annual illicit cash generation is probably going to exceed £12 billion, and the scope of money laundering activities within the country’s economy has already reached billions of pounds.

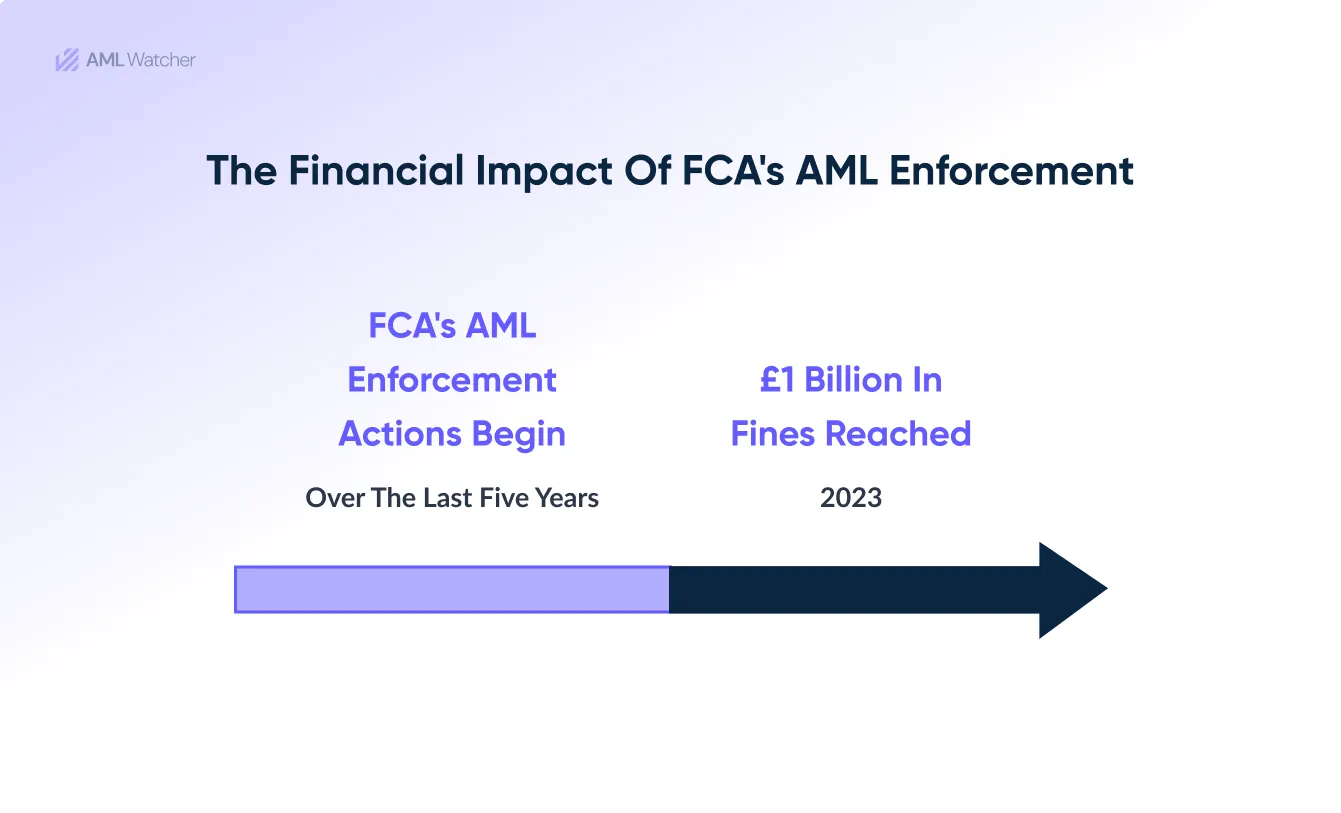

Given the ever-increasing threat of financial crimes that cost billions of pounds of loss, the British government has put in place strong and dynamic UK money laundering regulations to safeguard the integrity of Britain’s financial system and its credibility abroad.

Let’s take a quick look at UK AML regulations and the ongoing efforts.

How UK’s AML Regulations Evolved Overtime?

Back in the 1980s, when the modern banking system was really starting to come together and the world began to understand the risks of money laundering, the UK made a significant move.

They rolled out their first anti-money laundering rule with the Money Laundering Regulations 1993.

This was all about spotting and handling suspicious activities to keep illegal money from flowing through their financial system.

These days, financial institutions are finding it tougher to keep up with anti money laundering regulations UK, and the enforcement of these regulations has massively ramped up.

Money Laundering Regulations 1993

Under this regulation, financial institutions need to set up ways to stop money laundering and assist law enforcement in spotting cases of it. This is a key part of the UK’s efforts to implement the EU Directive on Money Laundering.

The following areas of the financial and professional services sector have to follow the UK AML Regulations.

- a) every building society, bank, and lending organization;

- b) any insurance company that falls under the EC Life Directives, including the life insurance sector of London-based Lloyd’s;

- c) all individuals and businesses that are allowed by the Financial Services Act of 1986 to participate in investment activities.

Proceeds of Crime Act (POCA)

Passed by the UK Parliament in 2002, the Proceeds of Crime Act (POCA) is the main law tackling UK money laundering regulations.

It clearly lays out what money laundering looks like for the first time, including things like getting or sharing illegal money, helping move that cash around, and hiding it.

Thanks to POCA, banks and financial institutions now have to follow certain anti-money laundering (AML) rules.

This includes keeping an eye on transactions, doing proper checks on customers (known as Customer Due Diligence or CDD), and reporting anything suspicious to catch money laundering activities early on.

The Financial Services and Markets Act 2000 (FSMA)

The Financial Services and Markets Act 2000 (FSMA) (c. 8) established by the United Kingdom Parliament created regulatory bodies for insurance, investment business, and banking through the Financial Services Authority (FSA) and formed the Financial Ombudsman Service to offer a cost-free dispute resolution method outside of court.

The Financial Services and Markets Act 2000 went through big amendments through the Financial Services Act 2012 and the Bank of England and Financial Services Act 2016.

The act governs the financial services sector and market operations throughout the United Kingdom.

The Financial Services and Markets Act (FSMA) seeks to safeguard consumers while boosting trust and competitive practices in the financial services sector.

The framework regulates financial markets and services in the UK by setting conduct standards and ensuring that firms operate with sufficient funding and management.

The Money Laundering, Terrorist Financing and Transfer of Funds Regulations 2017

This regulation, which took effect on 26 June 2017, embodies a significant transformation by replacing the 2007 Money Laundering Regulations and the 2007 Transfer of Funds (Information on the Payer) Regulations.

It successfully implements key aspects of the Fourth Money Laundering Directive, inspiring businesses to embrace robust anti money laundering regulations UK.

The 2019 amendment, which transposed the 5th AML Directive into national law, drew special attention to the UK’s commitment to a safe and transparent financial landscape, even as it chose not to adopt the 6th AML Directive, recognizing that much of its essence was already woven into existing UK law.

AML Regulatory Organizations in the UK

Financial Conduct Authority (FCA)

Established on April 1, 2013, FCA is the biggest regulatory institution that regulates all financial markets in the United Kingdom. FCA is a non-government organization that works independently.

The unit, which oversees the UK financial industry, and the Parliament have power over the FCA.

Maintaining the financial integrity of UK-registered financial institutions and ensuring a fair financial market for the finance sector, which offers services to businesses, consumers, and the economy at large, are the key goals of this regulatory body.

The key responsibilities of the UK’s biggest financial regulatory is to:

The key responsibilities of the UK’s biggest financial regulatory is to:

- Protect British customers from the dissemination of misleading financial bits of advice and mistreatment of vulnerable consumers, as well as prohibiting businesses from offering financial services that are inappropriate for particular customer segments.

- Encourages healthy competition amongst the UK’s financial services providers.

- Maintains the stability of the financial services sector.

His Majesty Revenue and Customs (HMRC)

Established on 18 April 2005, HMRC is a non-ministerial department of the UK government and has over 66,000 employees nationwide. Its primary objective is tax collection, payment of certain types of state assistance, and management of various regulatory frameworks.

HMRC reported challenges in compliance with business tax regulations with 11.4% in 2005-2006 to a 13.9% increase in 2022-2023 in the Corporation Tax Gap.

HMRC also works as a law enforcement agency to prevent financial crimes like tax evasion smuggling, tax fraud, excise (alcohol and tobacco) fraud, and money laundering and maintaining the integrity of the financial system.

National Crime Agency (NCA)

Established on October 7th, 2013, the National Crime Agency (NCA) is the FBI of the United Kingdom. It is the country’s leading national law enforcement agency that goes after the criminals who pose a national security threat to British institutions, infrastructure, and the well-being of the general British public.

As per the Suspicious Activity Report (SARs) Annual Report 2022 published by NCA, 901,255 SARs were received and processed in the UK’s fiscal year of 2022, which is a 21% increase over the year before.

It deals with cybercrime, transnational economic crimes (like money laundering and tax evasion), drug and human trafficking, and smuggling of illegal weapons.

Put simply, it can be entrusted with investigating any crime. Therefore, it collaborates closely with local law enforcement, regional organized crime units (ROCUs), and other government ministries and organizations.

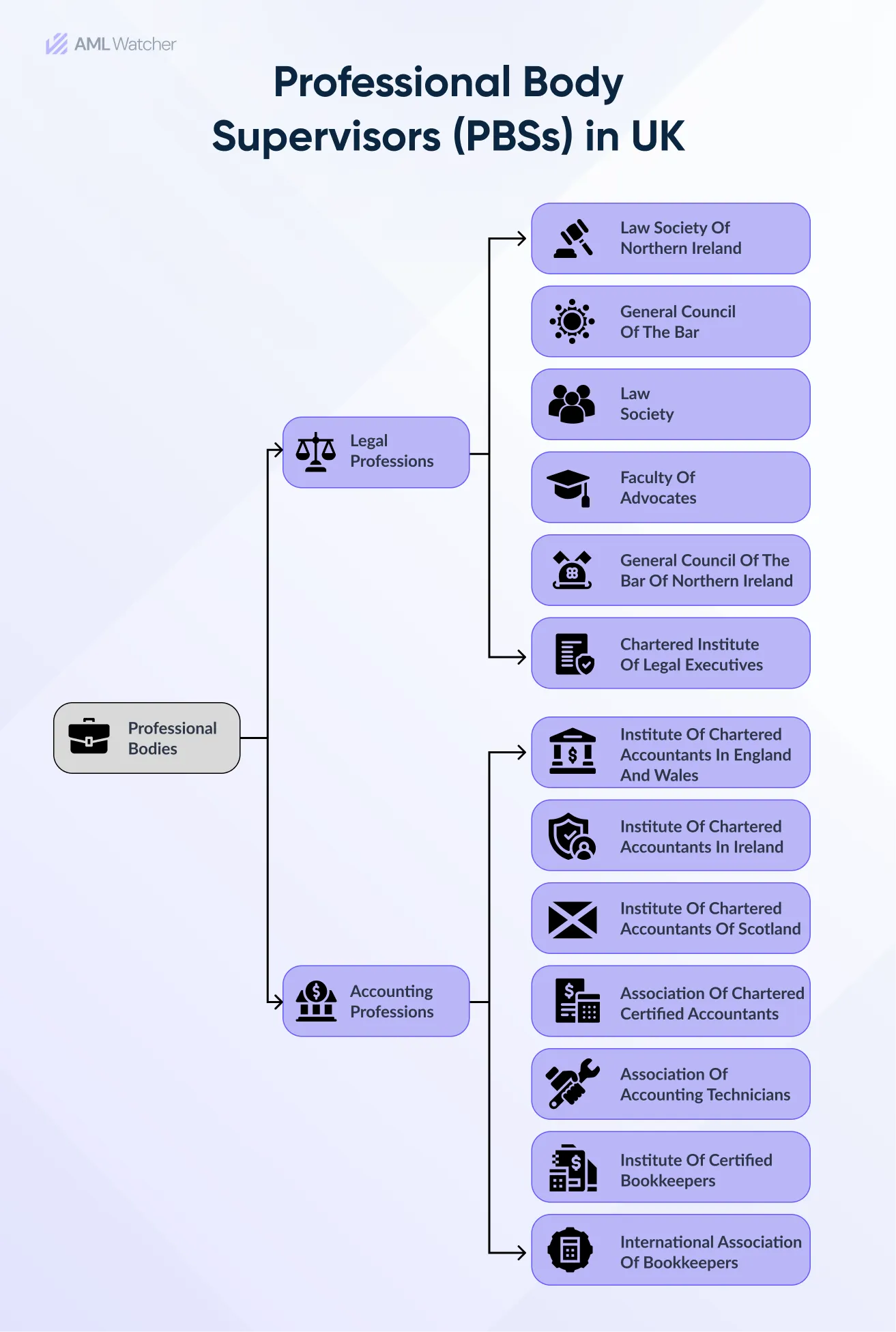

Other Regulatory Bodies for Particular Industries & Professions

Other than NCA, HMRC, and FCA, there are 22 professional body supervisors (PBSs) that supervise the accounting and legal, including:

All these regulatory bodies emphasize one thing, that, Organizations must have complete AML compliance systems, which include customer due diligence (CDD), transaction monitoring, and reporting of suspicious activity. These policies are intended to combat financial crime and ensure transparency in the financial sector.

How?

By adopting a reliable AML screening solution backed by comprehensive sanctions databases

How AML Watcher Ensures Your Compliance with UK AML Regulations?

AML Watcher is a trustworthy compliance partner for UK Money Laundering Reporting Officers, offering bespoke screening solutions to fulfill tough UK AML standards.

The key features include:

Comprehensive Sanctions Database

Access to worldwide sanctions lists (EU, UN, OFAC, FCA, etc.) to ensure complete compliance with AML regulations UK, and international rules.

Unified PEP Screening

Combines UK and global Politically Exposed Persons definitions, ensuring thorough screening of domestic and foreign PEPs and their associates.

Separate Watchlist Screening

Integrates over 3500 official watchlists, covering individuals flagged for financial crimes and terrorism.

Customizable risk management

Offers customized risk scoring algorithms to prioritize high-risk clients and transactions per FATF standards.

PEP Risk Categorization

Organizes PEPs into 1-4 risk tiers for focused due diligence on high-risk people as mandated by UK regulators.

Transaction Monitoring

Leverages powerful algorithms that detect questionable transactions in real-time, assisting enterprises in detecting money laundering activities and meeting UK regulatory requirements.

Risk-based Screening

Screening efforts are concentrated on high-risk jurisdictions and organizations, resulting in optimal resource allocation.

Real-time monitoring

Automated warnings and frequent updates keep institutions up to date with regulatory developments regarding global sanctions lists, PEP databases, and watchlists.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries