Why Customer Risk Assessment Is Essential for Effective AML Compliance?

AML Compliance

April 30, 2025

How effective is your AML process at mitigating the risks posed by a high-risk customer?

The Financial Conduct Authority (FCA) of the United Kingdom fined Starling Bank £29 million in October 2024 for major deficiencies in its anti-money laundering (AML) checks and sanctions screening.

Key flaws included insufficient sanctions screening and poor risk assessment, where the bank’s automated system failed to detect customers on sanctions lists, and the bank opened nearly 54,000 accounts for high-risk persons between 2021 and 2023.

Furthermore, the FCA criticized the bank’s senior management for lacking the ability to adequately implement AML risk assessment procedures.

As financial institutions require a thorough customer risk assessment to prevent potential misuse of the financial system.

Customer risk assessments are a regulatory requirement for entities subject to anti-money laundering (AML) regulations, such as banks and other AML-obligated organizations. These assessments should follow a risk-based approach (RBA) to analyze possible threats from high-risk customers.

Before moving further, why not explore what customer risk assessment is, why it is required, and its key components.

What Is A Customer Risk Assessment?

In anti-money laundering (AML), customer risk assessment is essential for detecting and managing risks connected with clients to avoid financial crimes such as money laundering and terrorism financing.

This process includes checking names, screening against sanctions lists, watchlists, and examining transaction patterns, services utilized, and jurisdictional linkages.

Financial institutions may comply with AML regulations and make sure they are successfully handling any risks by carrying out these evaluations.

Through a proper client risk assessment, institutions can determine if a customer:

- Appears on sanctions lists or blacklists

- Poses a money laundering risk

- Is a politically exposed person (PEP)

- Is involved in financing terrorism

- Has unusual transaction patterns

- Uses high-risk jurisdictions

- Has relationships with high-risk third parties

- Has a history of financial crimes

Key Considerations In Customer Risk Profiling

Customers’ risk profiles are determined by a variety of criteria, allowing institutions to analyze possible risks and expedite AML compliance processes. Important criteria include the industry sector.

Each institution will have a distinct level of risk tolerance for the customers it engages with, approving specific business connections depending on predetermined risk criteria.

Establishing clear criteria for customer risk scoring is essential for managing business risks and adhering to AML compliance standards.

Identifying Red Flags in Customer Risk Assessment

A Customer Risk Assessment is an ongoing process as risks with a client can change over time due to factors like new activities, dynamic financial behavior, or changes in AML regulations.

Thus, the risk assessment process should not end after the client is onboarded. Risk profiles should be monitored to detect changes.

Changes in risk profiles raise red flags that require reevaluation of their client risk assessment.

Some red flags that indicate the association of clients with financial crimes are

8 Key Components Of An AML Customer Risk Assessment

Institutions must incorporate a variety of measures into their AML screening process to successfully analyze the risks associated with each customer.

This involves checking customer names against sanction lists, identifying potential risks, and deciding the extent of due diligence needed.

For instance, the Financial Action Task Force (FATF) advises that business relationships should be avoided or terminated if appropriate due diligence cannot be performed.

The objective is to ascertain whether a customer is on any criminal or sanctions lists, is a politically exposed person (PEP), or is engaged in crimes like money laundering or terrorism funding.

To conduct a credible AML screening risk assessment, financial institutions must use a systematic, risk-based strategy that includes the following key steps:

1. Customer Due Diligence (CDD)

Customer Due Diligence verifies customer IDs and determines beneficial owners (for corporate clients). It helps that institutions know their customers and estimate the risk they pose, particularly during AML screening.

Businesses use different due diligence techniques based on the customer’s risk profile.

- Simplified Due Diligence (SDD) for low-risk customers.

- Customer Due Diligence (CDD) for standard risk customers.

- Enhanced Due Diligence (EDD) for high-risk customers, involving deeper evaluation and monitoring.

2. Risk Identification And Categorization

A complete AML screening evaluates several variables, including:

- Customers from high-risk areas or countries with lax AML rules must undergo more detailed screening.

- Certain industries, such as gambling, crypto, or medicines, may carry higher risks.

- Politically exposed individuals (PEPs) require further monitoring due to their increased risk of involvement in corruption or illegal activities.

- Analyzing the customer’s transaction pattern to detect any anomalies or irregularities that may suggest suspicious conduct.

3. Enhanced Due Diligence (EDD)

EDD is utilized when a client is considered high risk due to certain variables such as PEP status, suspicious transaction patterns, or linked with a high-risk jurisdiction.

Key Features of EDD include:

- Cross-references customer data against global sanctions, PEPs, and watchlists in real-time.

- Flags suspicious transaction behavior, such as large amounts or high-risk region activity.

- Assesses risk based on customer operations in high-risk or non-compliant jurisdictions.

- Continuously tracks customer activity and updates risk profiles as new data comes in.

- Scans global news outlets for negative media coverage related to the customer.

- Flag customers in high-risk industries, like gambling or arms trade, for deeper scrutiny.

- Detects inconsistencies between provided customer details and external data sources.

EDD ensures that financial institutions take extra steps to uncover hidden risks, such as money laundering or terrorist financing.

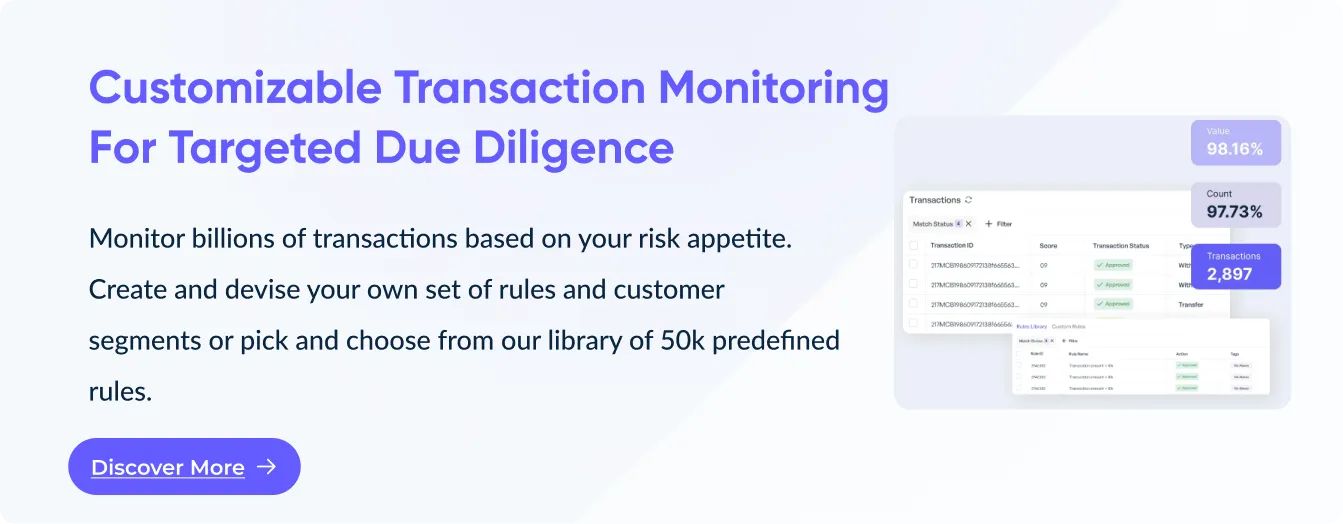

4. Real-Time Transaction Monitoring

This step requires to utilization of an efficient AML screening solution that scans real-time transactions for suspicious activity that differs from the customer’s regular behavior.

- Focus Areas:

- Unusual or large transactions

- Transactions involving high-risk jurisdictions.

- Potential structuring of payments (e.g., breaking up large amounts into smaller transactions).

Continuous monitoring allows for early discovery of illicit actions, which is crucial for ensuring compliance and limiting risks.

5. Politically Exposed Persons (PEPs) Screening

PEPs are individuals in prominent public positions who are more susceptible to involvement in corruption and financial crimes.

Financial institutions must identify PEPs and perform continuous monitoring on them, updating their risk profiles as their political or financial circumstances change.

PEP checks are not just a one-time procedure but an ongoing obligation under various AML laws.

6. Customer Risk Profiles

Effective AML screening entails classifying consumers based on risk criteria (e.g., transaction history, geography, PEP status, etc.).

- Low-Risk: Transparent customers with clear income sources.

- Medium-Risk: Customers who face certain risks due to geographical or commercial circumstances.

- High-risk Customers: With complicated ownership arrangements, a lack of transparency, or those associated with high-risk industries.

Prohibited or banned: Customers who have been recognized as engaging in illegal activity or posing a significant risk of financial crime.

7. Ongoing Monitoring and Review

Continuous monitoring requires that customer risk profiles be updated on a frequent basis to reflect new threats or regulatory changes. This involves a continuous analysis of sanction list changes, transaction trends, sanction delisting, and PEP status updates.

AML screening systems should be flexible enough to accommodate changes in customer data or new regulations, ensuring the institution remains compliant and proactive in risk management.

8. Integration of Advanced AML Technology

AML RegTech tools like AML Watcher play a critical role in automating AML screenings, real-time monitoring, and customer risk assessment updates.

These tools decrease human error, reduce false positives, boost productivity, and ensure that all client profiles are constantly updated with the most recent data from worldwide watchlists and regulatory updates.

Elevate Customer Risk Assessments with AML Watcher

A well-structured AML screening risk assessment is fundamental in preventing financial crimes, like money laundering and terror financing.

Institutions can ensure they remain compliant with AML regulations while safeguarding their operations from illicit activities by integrating technology, continuous monitoring, and a risk-based approach.

AML RegTechs, such as AML Watcher, streamline the risk assessment process

and enhance decision-making by automating key AML screening tasks.

AML Watcher helps,

- Implement a risk-based approach (RBA) by leveraging a proprietary data layer.

- Provides access to 6 million+ PEP profiles, data from 235+ countries, and screening against 3500+ international watchlists.

- Offers detailed information on 215+ international sanctions and provides timely alerts on regulatory enforcement actions.

- Real-time monitoring updates customer risk profiles in line with jurisdiction-specific regulations and provides insights into banking regulations.

- Detailed customer risk assessment evaluates entities across regions, sectors, and jurisdictions, with customizable risk thresholds based on institutional needs.

- Enhances decision-making by reducing unnecessary de-risking and applying customized risk thresholds.

- Advanced name matching detects aliases, nicknames, and uses unique identifiers like ID numbers or biometrics.

- Fuzzy matching technology reduces false positives, improving screening efficiency.

- Creates custom risk profiles that tailor risk scores and screening based on the institution’s risk appetite and sanctions exposure, ensuring precise alerts.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries