Does the Difference in Rules and Regulations Affect AML Compliance?

AML Compliance

May 23, 2025

- What Are Rules?

- What are Regulations?

- Exploring the Historical Development of Rules and Regulations

- Significance of AML Rules and Regulations

- Effective AML Rules: Best Practices for Compliance

- How AML Regulations Influence Rule-Making and Organizational Compliance

- AML Supervisory Authorities around the World

- AML Watcher: AML Compliance Solutions Aligned with Rules and Regulations

A bank from Canada named “Exchange Bank of Canada” has been penalized with a $2.45M fine for breaching AML/CFT regulations on 11 December 2024.

What do you think upon hearing or reading “rules and regulations”? Do they sound similar?

Although rules and regulations differ in many aspects, like purpose, at the same time, they seem similar. Both terms tell the reader what one should do or must follow.

Similarly, AML rules and regulations are “a set of laws, regulations, and guidelines” enforced by regulatory and enforcement bodies to preserve the integrity of regulated businesses and financial institutions.

Failure to comply with these rules and regulations can result in penalties for the parties who are liable to follow them.

Mixing their meaning and concepts can confuse and cost you a lot, as they are both different in compliance terms, despite having similarities. If you are running a business, doing a job in the compliance world, or managing internal policies, you need to understand what are rules and regulations.

Comprehending the rules and regulations meaning, as well as the difference between them, is especially important for AML-obligated sectors such as financial institutions that must comply with complex and often conflicting AML requirements.

Let’s clearly understand AML rules and regulations to implement internal policies and government-issued workplace regulations effectively.

So, why not go through this article to learn what are rules and regulations?

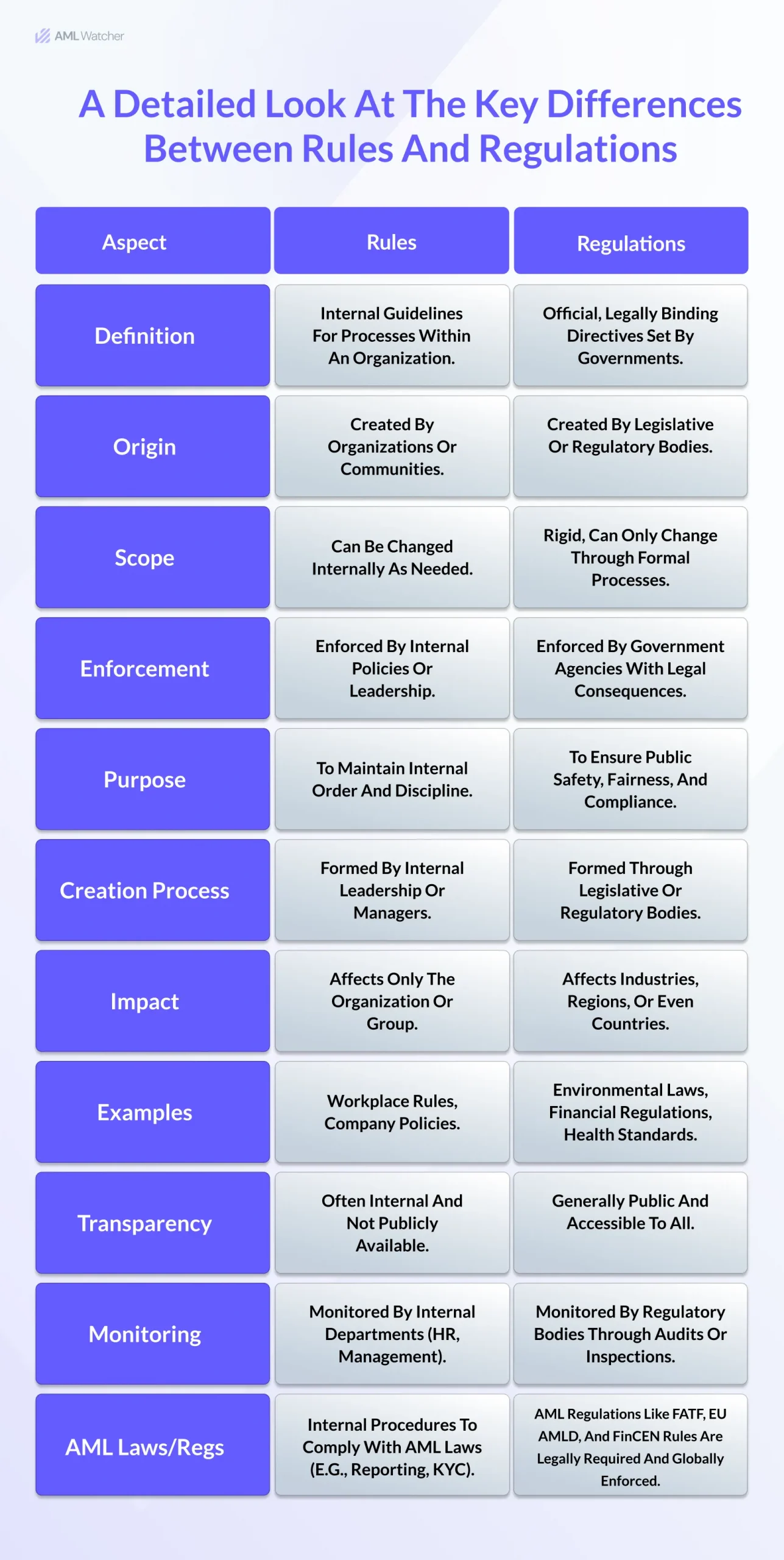

The main difference between rules and regulations lies in who implements them and the consequences of non-compliance.

What Are Rules?

In a broader term, rules are a set of clear “instructions or guidelines” describing what actions are permitted within a particular community or group and what are not permissible.

Generally, Rules are established by a specific group, individual, or organization to direct people’s behavior within a specific community and impact their decisions.

Specific characteristics of rules are mentioned below:

- Rules are usually intended to apply to anyone within a specific group or community, or organization, and offer a structure that promotes uniformity and equality in behavior.

- Any entity that has power or authority within an organization or community can create rules, such as

- Teachers can make decisions for the classroom

- A manager can establish rules in the workplace

- Parents can make rules in a household

- Usually, rules are implemented by the same authority that creates the regime or are self-enforced.

- Individuals or entities that fail to adhere to these regulations or exhibit noncompliance may face severe penalties depending on the severity of the breach.

- Considering different situations and conditions, rules can be modified or altered entirely by the same authority.

What are Regulations?

Regulations are legally and officially announced and implemented guidelines by a legal authority or regulatory body, such as a “government body”.

Regulations are more serious than rules, as they are backed up by law, and any non-compliance can have legal consequences in the form of penalties.

Characteristics of regulations are described below:

- Enforcement bodies implement legal AML penalties for failing to comply with regulations.

- Regulations are established by a legal government body or authority on different levels, like local, state, national, or even international.

- Rules are restricted to particular groups or communities, while regulations apply to everyone (individuals and entities) in a state or country.

- The main goal of regulations is to smoothly integrate fairness and safety in every financial and regulated organization to help the community.

- The community will follow the same standards and treat the public equally.

Exploring the Historical Development of Rules and Regulations

Rules and regulations have guided human societies for centuries. Early civilizations based their laws on moral and religious values to maintain justice and harmony.

As societies grew complex, formal legal systems emerged, with regulatory bodies creating and enforcing regulations to manage industries, public services, and governments.

Shifting from informal societal rules to formal written laws brought clarity, justice, and consistency. With technological advances and expanding industries, new rules became necessary to ensure safety, fairness, and trust, especially in today’s digital era.

Issues like data privacy, cybersecurity, and cryptocurrencies have influenced regulators to evolve laws and implement new standards to address modern challenges.

Significance of AML Rules and Regulations

Any regulated and organized industry or business requires defined, clear, organized rules and regulations to ensure stability, protection, transparency, and fairness within that sector/industry.

Financial institutions, regulated businesses, and designated non-financial businesses and professions (DNFBPs) are vulnerable to Financial crimes such as “money laundering, terrorist financing, and other”.

Regulatory bodies and enforcement agencies collaborate to address these financial risks through established AML rules and regulations.

The goal of AML regulations is to prevent the conversion of illicit funds into legitimate funds, stop informal money flows into the legal financial system, and disrupt criminal networks.

AML rules are established to bring stability and transparency to the financial ecosystem. AML guidelines are established for businesses and individuals to keep trust among shareholders and establish a safer environment for clients and business partners.

Financial organizations and businesses achieve financial stability and transparency by complying with anti-money laundering rules and AML regulations.

Understanding AML Rules: An Overview

While not all AML rules are directly linked to regulations, organizations and authorities that create these rules must still follow the AML regulations established by governments. AML Rules often help in the effective implementation of AML regulations.

Internal policies are made by regulated businesses, fintech companies, and financial institutions like banks to prevent illicit activities.

AML compliance rules, typically integrated within a company’s internal compliance program, are developed by considering the company’s risk exposure and aligned with the AML laws of the relevant jurisdiction.

- Anti-money laundering Rules are set for internal onboarding, such as what steps must be followed in the Know Your Customer procedure.

- Rules have been established for specific thresholds regarding transaction monitoring.

- Rules for training employees to detect suspicious activities and submit reports.

Explaining AML Regulations: Key Insights

Regulatory bodies and enforcement agencies set international standards to be followed, such as “FATF’s 40 Recommendations, FinCEN’s AML Program Rule, EU’s AML Authority (AMLA) regulatory framework, and OFAC sanctions compliance in the U.S.”

Penalties for Non-Compliance

Failure to comply with AML regulations can lead to penalties and fines. The Nevada Gaming Control Board (NGCB) has fined “Resorts World Las Vegas” for breaching AML laws and regulations.

A detailed 31-page complaint has been registered against AML Laws violations, resulting in “multi-million dollar fines” on 15 August 2024.

The violations include:

- Failing to file Suspicious Activity Reports (SARs) as required by the Bank Secrecy Act.

- Neglecting to implement an effective AML compliance program.

- Not conducting enhanced due diligence on high-risk customers.

- Breaching Nevada state regulations by allowing individuals with criminal backgrounds to operate on the premises.

- Failing to verify the source of funds for large transactions.

- Maintaining inadequate AML internal controls to detect suspicious activities.

Effective AML Rules: Best Practices for Compliance

Financial institutions and other regulated businesses are mandated to implement AML rules in their AML Compliance program to ensure effective compliance with AML regulations established by enforcement bodies and regulators.

Best practices for implementing compliance actions are given below.

Customer Due Diligence (CDD)

Before starting a business relationship, one must conduct Customer Due Diligence (CDD) by verifying their identities through collecting official data and assessing their risk profile.

Enhanced Due Diligence (EDD)

When high-risk clients such as PEPs are involved, enhanced due diligence (EDD) should be performed to evaluate and mitigate financial risks such as money laundering and terrorist financing.

Ongoing Monitoring

Continuous monitoring of transactions detects suspicious activities and ensures the client’s behavior aligns with their risk profile.

Record Keeping

Data-related transactions and client information must be stored safely for at least five years. Record keeping helps with further investigation and audits.

Suspicious Activity Reporting (SAR/STR)

If a transaction is flagged as suspicious, then organisations must report the suspicious activity to the relevant authority for further compliance action.

Risk-Based Approach (RBA)

A risk-based approach is followed to assess a client’s risk level, and clients with higher risks require stricter measures.

AML Training and Awareness

AML training should be delivered to Staff members to communicate to them about AML rules of the organization and how to use AML risk screening and transaction monitoring software.

Conducting Periodic Audits

Internal and external AML audits must be performed to review AML systems and implementations of AML rules and regulations, and ensure gaps are identified and filled effectively.

How AML Regulations Influence Rule-Making and Organizational Compliance

AML regulations set by supervisory authorities provide the foundational legal framework that guides countries in developing their own AML rules.

Regulatory authorities define these regulations based on international standards such as the FATF Recommendations, tailoring them to national contexts.

Financial institutions and regulated businesses must align their internal AML rules and policies with these regulatory guidelines to ensure effective compliance and risk management.

Understanding and familiarizing oneself with the varying AML regulations across jurisdictions is crucial for organizations.

It enables the formulation of AML rules that are not only compliant with local laws but also responsive to evolving risks, thereby enhancing the effectiveness of AML programs.

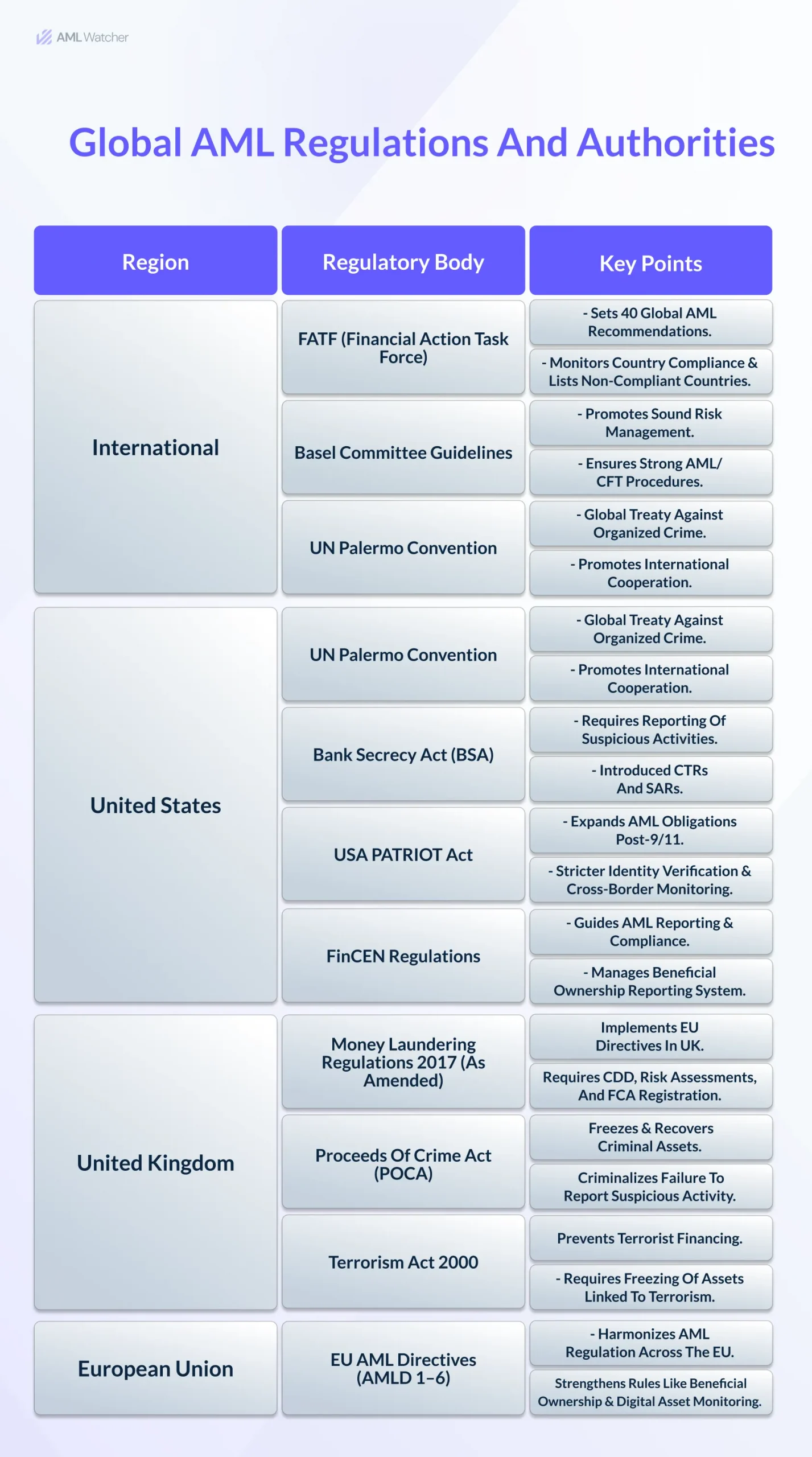

AML Supervisory Authorities around the World

National supervisory authorities monitor, guide, and sometimes audit financial institutions to enforce compliance with AML laws.

The following are key AML supervisory authorities worldwide, along with their latest regulatory guidelines and initiatives:

AUSTRAC (Australian Transaction Reports and Analysis Center)

AUSTRAC collects SARs implementations of AML/CFT laws and monitors compliance. A major recent update involves the implementation of Tranche 2 reforms, strengthening AML requirements and expanding reporting obligations to address emerging financial risks.

Monetary Authority of Singapore (MAS)

It enforces AML/CFT rules in Singapore and monitors FIs to comply with laws according to the delivered MAS requirements. MAS regularly updates its Notice 626 and related guidelines to address evolving threats.

Hong Kong Monetary Authority (HKMA)

HKMA oversees AML compliance within Hong Kong’s financial sector, covering customer due diligence (CDD), transaction monitoring, and suspicious transaction reporting.

European Union (EU)

While the EU is not a supervisory authority in the traditional sense like MAS or AUSTRAC, It establishes “regional AML laws” through directives like “AMLD 4, 5, and 6,” which create guidelines for member states.

The EU has created a central AML authority (AMLA) operational in 2027 to uniform and streamline operations and supervision.

Financial Conduct Authority (FCA)

FCA is the central regulatory body in the UK, implements AML regulations such as the “Money Laundering Regulations 2017,” and supervises AML compliance.

As of January 2024, the FCA’s guidance emphasizes a risk-based approach to Politically Exposed Persons (PEPs), classifying domestic PEPs as lower risk than foreign PEPs, requiring proportionate Enhanced Due Diligence (EDD) and regular status reviews.

AML Watcher: AML Compliance Solutions Aligned with Rules and Regulations

AML Watcher offers tailored screening solutions to help organizations comply with AML regulations and set strong internal policies. Features include PEP screening, adverse media detection with sentiment analysis, and worldwide watchlist screening across 235+ countries.

Sanctions screening ensures compliance with 215+ sanction regimes, while custom risk scoring and ongoing monitoring allow real-time risk assessment and alerts to stay aligned with required regulations.

Transaction monitoring provides insights into client transactions, enabling rule-setting for further investigation or enhanced due diligence.

Biometric AML uses advanced image matching to screen identities and reduce false positives, helping organizations mitigate financial risks and avoid penalties.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries