Difference Between Currency Transaction Report and Suspicious Activity Report

PEP

November 20, 2025

- What is a Currency Transaction Report (CTR)?

- What is a Suspicious Activity Report (SAR)?

- Common Challenges in CTR and SAR Reporting

- CTR Vs SAR: What is the Impact of a Filing Inefficiency?

- The Use of Advanced Technology for Effective SAR and CTR Filing

- How Compliance Units Can Calibrate CTR and SAR Filing?

- Make Every CTR and SAR Count with AML Watcher

In Anti-money laundering compliance (AML), it is crucial to understand the differences between the Currency Transaction Report (CTR) and the Suspicious Activity Report (SAR). Knowing when and how to file CTR in AML and SAR in AML enables financial institutions to minimize unnecessary filings and ensure in-depth examinations.

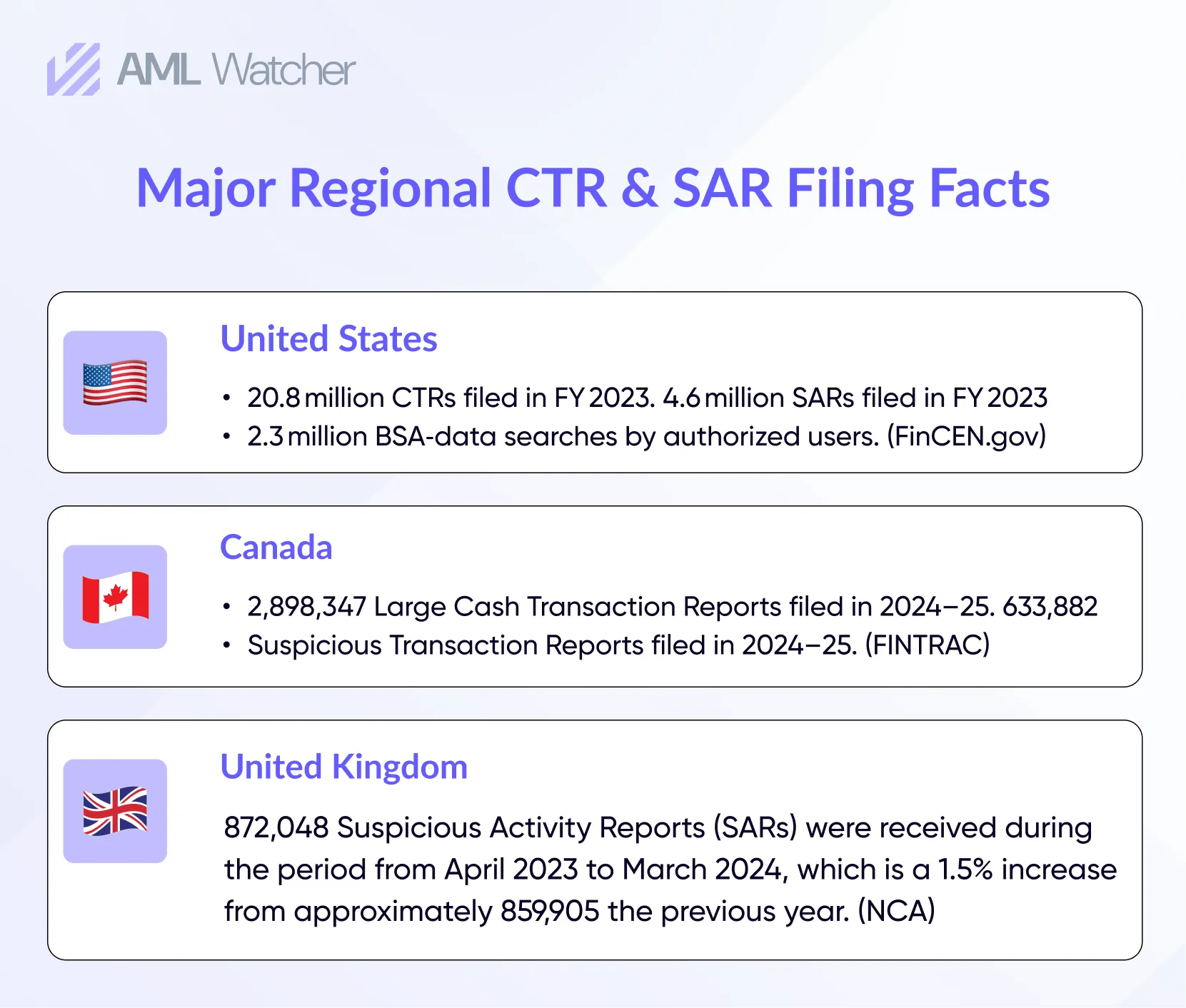

Compliance teams usually confront millions of filings annually, but only a fraction contribute to investigations. As per the records of the United States Government Accountability Office, approximately 170 million CTRs were filed by banks between the time period of 2013-2023. On average, only 0.44% of the 5.2 million CTRs resulted in follow-up inquiries. Now, if we look at the percentage of SARs, then approximately 4.6 million Suspicious Activity Reports were filed in 2023, and only 0.5% were involved in FBI investigations.

This incompetence results in an increasing focus on advanced and intelligence-driven reporting, where technology can divert institutions from unnecessary filings to the actual alerts. The continuous exercise will assist financial institutions (FIs) in filing only when necessary, benefiting the institutions, their clients, and regulators at the same time.

Let’s explore CTR Vs SAR to offer clarity on their significance for FIs and how they enhance efficiency within AML reporting.

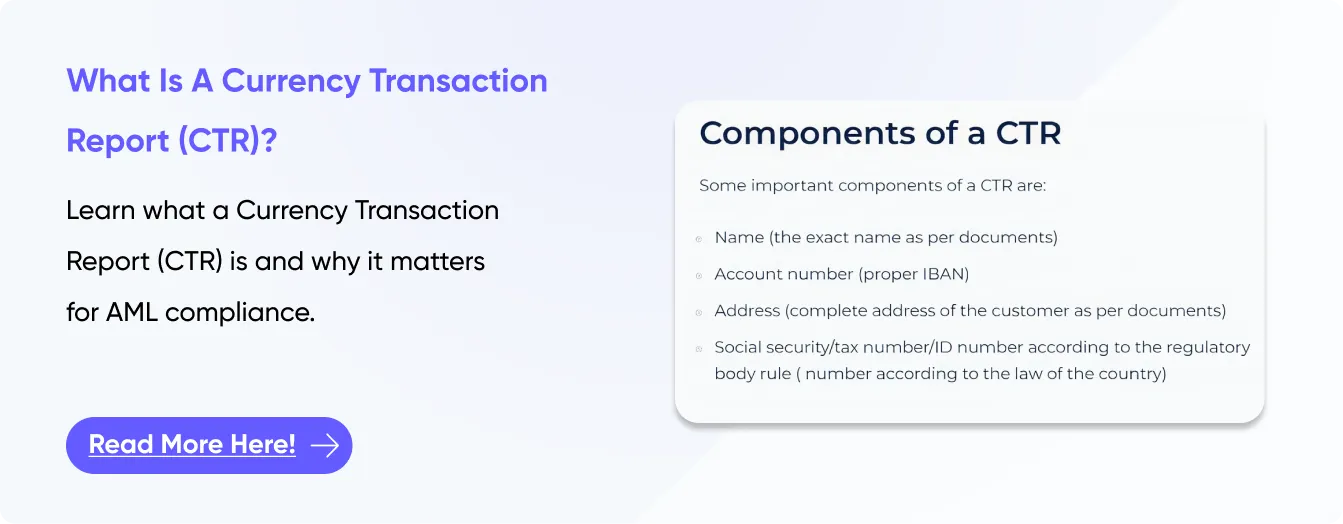

What is a Currency Transaction Report (CTR)?

A currency transaction report is an essential requirement for banks and financial institutions. They need to file this report whenever their client is involved in a huge cash transaction that triggers the limit of the CTR framework. This is a fundamental part of CTR in banking, which ensures transparency in large cash movements. For example,

- The maximum threshold is C$10,000 in cash in Canada.

- For a single day in the United States, the maximum threshold is $10,000.

And if an individual is exceeding this limit, they automatically trigger a CTR filing requirement.

FYI

The U.S. threshold of $10,000 has not changed since 1972, and if adjusted for inflation, that amount would be approximately $72,880 in 2023. This indicates that a lot of transactions that are reported today would not have triggered a report back then.

CTRs are intended to capture large cash flows, particularly to detect potential money laundering techniques which includes structuring, but they do not themselves check if the transaction is genuine or not.

CTRs are relatively simple to file, requiring only transaction and customer details. However, because filing is triggered solely by transaction amount, they often create a high volume of reports with limited investigatory value.

What is a Suspicious Activity Report (SAR)?

A suspicious activity report is a must for FIs to file whenever they suspect that the transactions are associated with some illegal actions, including, terrorist financing, tax evasion, money laundering and other associated financial crime acts.

Unlike CTRs, SARs do not have a fixed threshold for cash, but they require:

- A narrative describing why the activity is suspicious

- A proof and information for support.

- A guarantee that the report meets regulatory standards so that it can be used effectively.

For example, an SAR can be triggered by irregular patterns in a client’s behaviour, such as if the customer transfers a huge amount of funds to multiple offshore accounts. It can be triggered in case of a customer transmitting small chunks of payments to different local accounts at irregular time patterns.

According to a recent study, in the UK, the National Crime Agency (NCA) received approximately 500,000 SARs in a single year. A lot of them are from banks, yet only a fraction result in pragmatic audits.

Common Challenges in CTR and SAR Reporting

Several operational and regulatory hurdles reduce the effectiveness of CTR and SAR in banking processes:

- Defensive Filings: Some banks file suspicious activity reports just to evade huge regulatory consequences rather than to report an actual SAR. These defensive SAR filings result in a massive amount of poor-quality reports that make it difficult for law enforcement to identify and act on genuine cases.

- Weak Narratives: Suspicious activity reports that usually don’t have strong narratives and supporting evidence create ambiguity for the investigative agencies.

- Alert Overload: FIs receive numerous alerts in a day, which slows down the process of investigations and challenges the teams in identifying the actual risks.

- Global Complexity: Banks operating in different regions usually face the challenge of complying with the varied regulatory standards for each jurisdiction. Because every region has an independent regulatory system, deadlines, alerts and limitations, which makes the filing of CTRs and SARs a confusing process.

- Evolving Criminal Methods: Digital payments and instant transfers are increasingly exploited for money laundering, bypassing traditional rule-based systems. This makes suspicious activities difficult to detect, which results in more SAR-related risk indicators.

Such challenges increase operational inefficiency and weaken the intelligence that regulators receive.

CTR Vs SAR: What is the Impact of a Filing Inefficiency?

Office of the Comptroller of the Currency (OCC) Case

The Office of the Comptroller of the Currency (OCC) issued a comprehensive cease-and-desist order against USAA Federal Savings Bank in December 2024. The regulator cited unsafe or unsound practices, including deficiencies in suspicious activity reporting (SAR filings). The bank’s non-adherence to regulatory requirements under the OCC’s heightened standards for large banks is also a reason behind the scrutiny.

Here’s how the SAR deficiencies affected the USAA Federal Savings Bank:

- USAA didn’t report the suspicious activities properly, so they got scrutinized by the regulators.

- The weak reporting highlights that the bank has technical glitches which missed the financial crime alert.

- As a result of these shortcomings, the bank was restricted from launching the new products or growing until it fixed the issues.

- This case damaged the bank’s reputation and eroded its client’s and investors’ trust.

Trump Taj Mahal Casino Case

FinCEN fined the casino $10 million for failing to file Currency Transaction Reports (CTRs) for large cash transactions, violating AML/BSA rules in 2015.

Here’s what happened to the casino when it showed filing inefficiencies:

- They had to face a huge financial penalty of $10 million for not reporting large cash transactions.

- Missing reports create difficulties for the authorities to track funds appropriately.

- The case damaged the casino’s brand image and highlighted its weak controls.

The Use of Advanced Technology for Effective SAR and CTR Filing

The integration of advanced technology within the systems can easily resolve the emerging challenges with the help of intelligence-driven filings. It offers financial institutions with:

High-Risk Prioritization

Context-based data such as adverse media, PEP lists, and network connections, enables FIs to pay attention to the actual cases.

Enhanced Narrative Quality

Systematic information can auto-generate SAR narratives with evidence that reduce the rate of manual errors and weak reporting.

Jurisdictional Guidance

Automated systems embed thresholds, red flags, and filing rules for multiple countries, simplifying global compliance.

Reduced Alert Fatigue

Dynamic risk-based thresholds filter out low-risk transactions while prioritizing high-risk ones.

Faster Investigations

Automated aggregation of media reports, sanctions, and ownership data accelerates the review process.

These capabilities ensure fewer, higher-quality filings, which improve efficiency for compliance teams, reduce unnecessary hassle for clients, and provide regulators with more actionable intelligence.

How Compliance Units Can Calibrate CTR and SAR Filing?

Compliance troops can integrate smarter workflows by:

- Linking transaction alerts to adverse media, PEP/ownership networks, and merchant risk scores.

- Using customized risk scoring to highlight the cases that genuinely need attention.

- Auto-populating SARs with supporting evidence, leaving analysts to review rather than write from scratch.

- Tracking changing reputations, shareholding frameworks, and transaction behaviour to spot potential issues.

The above mentioned practices help FIs file fewer reports, but with higher investigatory value, which increases productivity and helps in complying with changing regulations.

Make Every CTR and SAR Count with AML Watcher

In order to line up with the regulatory standards it is necessary to have precise CTR and SAR filings. And when volumes surge, alerts pile up, and investigative context is scattered across systems, even the strongest compliance teams feel the strain. AML Watcher is built for that reality. It turns fragmented data into organized information, helping teams stop reacting to filings and start owning the risk behind them.

The everyday problems of compliance professionals, including limited visibility, rising regulatory pressure, and the recurring tension of ignoring an actual alert, AML Watcher tackles it all. Here’s what it offers:

- Continuous monitoring of sanctions, adverse media, and ownership networks that offer analysts the context they rarely have time to gather themselves.

- One-page intelligence briefs that distill complicated transactions and associations into an immediate, decision-ready snapshot.

- Customized risk scoring that highlights genuinely mattered alerts and personalized due diligence according to the entity.

- Jurisdiction-specific advice and systematic SAR templates that remove uncertainty in multi-country reporting.

At AML Watcher, every feature is designed with a single purpose that is to reduce noise, strengthen decisions, and help your team produce filings that resist scrutiny and actually add value to your risk program.

Take the next step toward smarter reporting

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries