How AML Verification Ensures Regulatory Compliance

AML Compliance

December 4, 2025

With the expansion of digital finance in recent years, global regulators have intensified their oversight, which increases the pressure on FinTech, payments and crypto firms. As stated by the EU authorities, 70% of AML regulators observe increased money laundering risks in FinTech, and during the time period of 2020 to 2024, the number of compliance violations has more than doubled.

A parallel trend is seen worldwide, especially in the rapidly growing sector of Crypto. The Financial Action Task Force (FATF) in one of its report titled “Targeted Update on Implementation of the FATF Standards on Virtual Assets/VASPs”, warns that only 40 out of 138 jurisdictions are fully in line with the crypto-asset AML standards, whereas criminals in crypto may have gathered more than $51 billion in 2024. This regulatory burden highlights the need for effective AML verification to ensure compliance and build trust in the financial system.

What Exactly is AML Verification?

After the identity verification process, AML verification is the first line of defense against financial crime risks. AML verification involves screening customers against sanctions lists, watchlists, PEP databases, and adverse media to identify potential risks. It is a combination of Know Your Customer (KYC) checks and the risk assessment process. The aim of KYC is to verify whether a customer is genuine, whereas AML checks assess the risk level of clients based on the case.

AML checks cover processes from simple identity verification (KYC) to continuous real-time transaction Monitoring. This helps businesses identify each customer and evaluate the money laundering risk they may pose.

These are mandatory checks for AML-regulated entities worldwide. Failing to conduct them can be highly costly for financial institutions, potentially leading to severe fines and reputational damage. Furthermore, corporate officers face personal liability, which can result in prison time. For instance, in recent cases, executives from major financial institutions have faced prosecution due to lapses in AML compliance. This highlights the critical importance of adhering to AML requirements to safeguard both the organization and its leaders.

In a nutshell, AML verification is not a choice; it’s a legal requirement for regulated businesses. Doing it well not only helps avoid penalties but also prevents the firm from unintentionally facilitating crime.

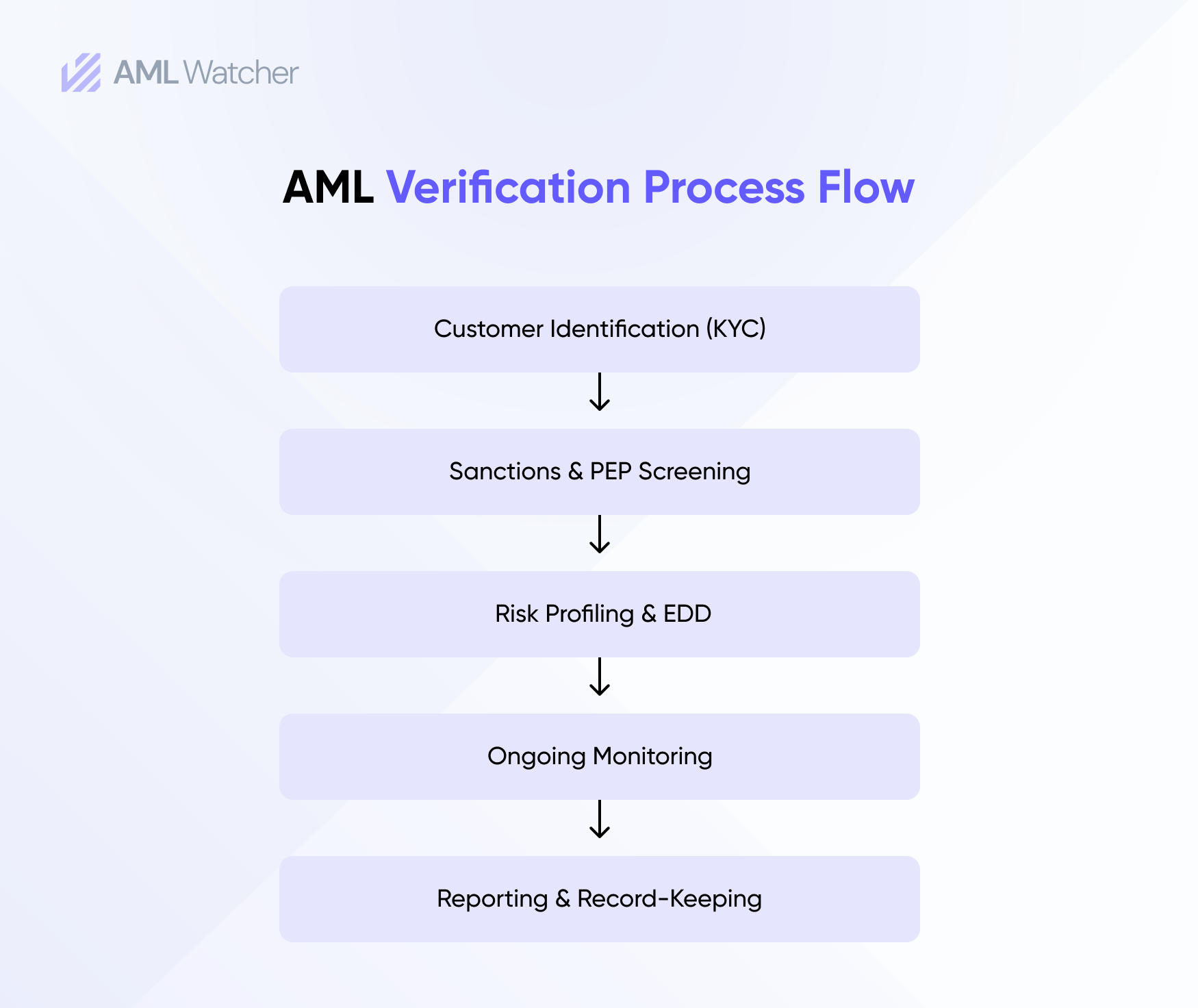

AML Verification Process

A structured AML verification process involves the following stages:

Step 1. Basic Customer Identification: The process starts by verifying the customer’s identity. For this, institutions are required to collect basic data, including the client’s legal name, date of birth, address, and ID documents (e.g. passport, driver’s license). Modern tools can even match a customer’s selfie to their ID in seconds to perform a precise investigation. This step ensures businesses are dealing with legitimate clients who they claim to be.

Step 2. Sanctions and PEP Screening. When the system is done with ID check, the customer is screened against global sanctions lists (countries and individuals under embargo), Politically Exposed Persons (PEPs) lists, and adverse media databases. The goal is to flag any customer linked to corruption, terrorism, or crime. For example, if John Smith’s name matches someone on an international sanctions list, this step triggers a red flag. Specialized software cross-references customer details with thousands of sanctions and PEP sources. This ensures that “high-risk individuals” are caught before opening accounts.

Step 3. Risk Assessment & Enhanced Due Diligence (EDD). After initial screening, each customer is given a risk rating (low, medium, high). Factors include occupation, transaction volume, and geography. High-risk customers (e.g. money service businesses or clients in tax havens) get Enhanced Due Diligence, more documentation, and scrutiny. For instance, if a client suddenly deposits a large sum from a high-risk country, the bank may require proof of the source of funds. This risk-based approach means compliance effort focuses where it matters most.

Step 4. Ongoing Transaction Monitoring. AML compliance doesn’t end after onboarding. Customer transactions are continuously monitored in real time. Automated systems use rules and machine learning to flag unusual patterns – for example, rapid transfers just below reporting thresholds or payments to sanctioned regions. Any anomaly triggers alerts for human review. Advanced AI engines can “detect complex patterns” and significantly reduce false positives, freeing analysts to focus on genuine threats.

Step 5. Reporting and Record-Keeping. If monitoring uncovers suspicious activity, the institution must file a Suspicious Activity Report (SAR) with authorities. Regulators also require detailed record-keeping, often for 5 years, so institutions can prove compliance. These records and reports are crucial in demonstrating that “proper AML checks” were executed.

With the continuous practice of the above-mentioned steps, firms can easily follow the changing regulations and they can safeguard the integrity of their financial system.

Regulatory AML Verification Requirements and Best Practices

AML verification is not a choice; it has become a legal requirement. The Financial Action Task Force (FATF) sets globally accepted recommendations that countries accept in their laws. These standards, along with regulations at jurisdiction-level such as the EU’s AML Directives or the U.S. Bank Secrecy Act, explicitly require Customer Due Diligence (CDD) and monitoring. For example, FATF Recommendation 10 encourages using reliable documents and data to verify customer identity, and Recommendation 12 calls for enhanced scrutiny of PEPs. Effective compliance goes beyond single checks; it demands continuous due diligence for clients and perpetual KYC.

Standards usually change with the passage of time, for which companies are expected to customize their AML processes according to every region’s specific regulations. In the EU, successive AML Directives (4AMLD, 5AMLD, etc.) keep expanding scope and tightening standards. Globally, FATF’s 40 Recommendations serve as the benchmark, prompting regulators in 190+ countries to update their laws. This “risk-based approach” requires firms to stay agile, updating watchlists and policies continuously.

Neglecting AML verification comes up with many adverse consequences. Regulators impose huge fines, ban liscences, and even allegations of a criminal offense. For instance, in April 2025, Lithuania’s central bank fined Revolut €3.5 million, its largest penalty ever. The reason behind the fine is the company’s failure to properly identify the suspicious monetary operations during everyday checks. This penalty illustrates why thorough AML checks are essential. Not only does compliance avoid penalties, but it also shields a firm’s reputation and customers.

Best practices dictate integrating AML verification tightly into a firm’s operations. This means automating checks where possible, applying a clear risk-based framework, and refreshing data in real time. For example, high-quality AML data feeds reduce false alarms, and fast API screening accelerates onboarding. Ultimately, strong AML verification builds trust, reassuring regulators and customers alike that your business is secure.

What are the Challenges Faced by Firms While Performing AML Verification?

Performing AML verification isn’t easy. Firms face diverse complexities:

- False Alerts: Traditional screening often flags innocent customers. A common name like “Ahmed Khan” might match a sanctioned individual, leading to tedious manual review. An increased number of false alerts exhausts staff members and makes onboarding a time-consuming process.

- Compliance Hurdles: AML standards change continuously with time depending on different jurisdictions that causes serious tension for the firms in keeping themselves updated to evolving regulations. It’s an ongoing pressure for financial institutions.

- Language or Transliteration Complexities: Names are usually spelled differently across languages which means one name can have three or four pronunciations depending upon the language. This causes a serious tension for the teams and confuses the screening systems, which can ultimately result in more false positive alerts and missed risks.

- Governance Gaps: Compliance standards change continuously across different jurisdictions, causing serious tension for firms to keep themselves updated on evolving regulations. It’s an ongoing pressure for financial institutions.

- Incomplete or Stale Data: Screenings rely on data quality. Outdated watchlists or missing adverse media in regional languages can slip through the cracks. Gaps in data sources undermine the process.

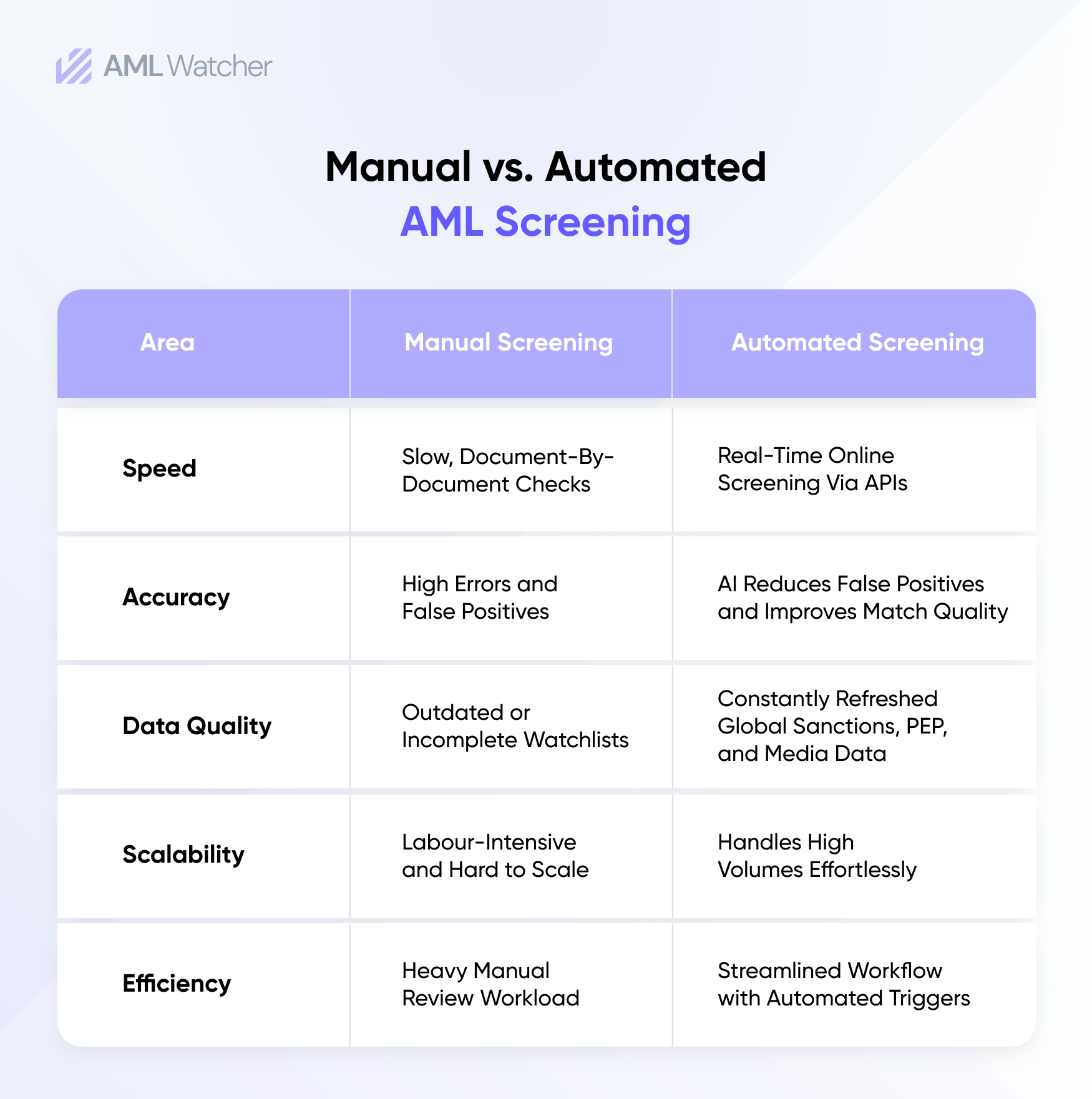

- Arduous Processes: Many compliance teams still depend on manual audits and spreadsheets. These traditional methods are error-prone and time-intensive. Manual reviews clear ten names an hour, while automated tools clear 10,000, offering a stark contrast that justifies technological investment. In fact, experts warn that relying solely on conventional verification methods is “nearly impossible to manage at scale” and advanced tools are now needed.

- Complex Entity Structures: Verifying companies and finding Ultimate Beneficial Owners (UBOs) demands corporate ownership checks. Layered shell companies can hide true ownership, complicating verification.

These complexities fail compliance teams in their tasks, waste their efforts on false alerts and leave risk at their doorstep. To overcome this, firms turn to technology and data integration.

How Advanced Solutions Make AML Verification More Effective?

Fortunately, modern technology makes AML verification more productive. These advanced solutions offer:

- Real-Time Online Screening: Advanced solutions allow online AML verification in real-time. Using APIs, firms can screen customers against thousands of global watchlists in seconds. This includes sanctions, PEP lists, adverse media, and leaked information, all updated constantly.

- Biometric Identity Verification: facial recognition adds security when verifying identities. These tools take a real selfie of the potential client and find the accurate matches.

- AI and Machine Learning: AI engines sift through huge transaction datasets in real time. They identify complex patterns that conventional systems might ignore, minimizing false alerts and spotting emerging risks. These advanced systems work on machine learning that improves with time by understanding the patterns.

- Customized Risk Scoring: Advanced screening tools offer tailored risk scoring depending upon the client’s risk profile.

- Integration and Automation: Advanced AML tools plug into a business’s onboarding and payment systems. They automatically trigger checks at critical points (new account opening, large transactions, periodic reviews). This “verification online” approach means compliance moves at business speed.

In short, digital AML solutions transform a tedious manual process into a streamlined, data-driven workflow. They allow companies to conduct AML checks at scale without sacrificing accuracy or speed.

Advance AML Compliance Process With AML Watcher

In the war against financial crime, every organization must stay vigilant. By combining sound processes with advanced tools, companies can deter criminals without disrupting genuine customers. Is your AML verification process up to the challenge of zero-backlog compliance day?

Here’s how AML Watcher empowers an AML verification process:

- With global AML verification that screens customers instantly against updated sanctions, PEPs, watchlists, and adverse media. AML Watcher delivers fast, API-powered AML ID verification that supports high-volume, cross-border onboarding.

- By customizing the risk scoring and pattern detection for teams, the system detects hidden relationships, behaviour anomalies, and evolving typologies. This reduces false positives and strengthens AML verification accuracy.

- With smooth KYC that has AML Integration, the system automatically combines identity verification with AML checks, ensuring full KYC AML verification in one workflow. No switching tools, no gaps, and no compliance blind spots.

These capabilities ensure an effective AML verification process that helps businesses stay compliant, scalable, and resilient against modern financial crime threats.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries