9 Steps to Build an Effective AML Policy for Businesses

AML Compliance

May 9, 2025

On 10 April 2025, the UK conducted “Operation Machiniz” targeting cash-intensive businesses like vape and barber shops suspected of money laundering. The operation led to 35 arrests and the raiding of hundreds of establishments. Ninety-seven victims of modern slavery were rescued, and £1 million in bank accounts were blocked.

It shows how legitimate businesses can be involved in financial crimes, and it requires establishing and implementing anti-money laundering (AML) policies in AML-obligated entities such as Banks, financial institutions, insurance companies, real estate agencies, and other industries.

Financial crimes are increasing daily, and criminals are utilizing different and advanced methods to integrate their illegal money into the legal and legitimate financial system; $3 trillion has been transferred through illicit activities.

The United Nations Office on Drugs and Crime (UNODC) report highlighted that 2 to 5 % of money is laundered annually.

AML policies and procedures will prevent the flow of illicit funds that are disguised as coming from a legitimate source

Let’s learn and understand the AML policy meaning, what is aml policy, and its significance in mitigating financial crimes.

Impact and Significance of AML Policies

Regulated businesses establish an anti-money laundering policy based on existing rules and regulations to mitigate AML non-compliance risks and consequent financial risks.

These institutions play a crucial role in detecting and reporting financial risks in accordance with industry and company requirements.

Robust automated AML software enables financial institutions to implement AML policies and procedures that align with their risk appetite..

International AML Enforcement Procedures

International AML standards and regulations offer essential guidance for building robust anti-money laundering policies.

The regulatory body, the Financial Action Task Force (FATF), establishes standards for countries to streamline their anti-money laundering (AML) and counter-terrorist financing (CTF) efforts.

It has 39 members, covering 37 countries and entities, including the European Commission and the Gulf Cooperation Council.

The FATF’s recommendations provide a framework for financial institutions to establish effective AML policies and procedures.

Recommendation 10: Customer due diligence

As per Recommendation 10, Financial institutions must conduct customer due diligence (CDD) under three conditions.

- Starting a business relationship or performing transactions above USD/EUR 15,000.

- Suspecting money laundering or terrorist financing.

- Customer data for verification is doubtful.

Each country may determine how it implements specific CDD obligations, either through law or enforceable means. The CDD measures to be taken are as follows:

- Verifying the identity of clients

- Identifying the beneficial owner

- Understand the purpose of business.

- Ongoing due diligence throughout the business relationship

If the CDD measure should be implemented for all new and existing clients to ensure a risk-based approach is followed, terminate the business relationship if the CDD can’t be completed and a suspicious report is filed.

Recommendation 11: Record keeping

Financial institutions must retain transaction records for at least five years, including local and international transaction data, currency details, and evidence of criminal prosecutions.

Keep CDD-related data, such as copies of identification documents and account files, even after the business relationship ends or an occasional transaction occurs.

Recommendation 18: Internal Controls and Compliance Officer

Financial institutions must implement internal AML policies and procedures for robust AML compliance.

As per the interpretive note to recommendation 18, hire an AML compliance officer to oversee and manage the implementation of AML policies, ensuring compliance with regulatory requirements, and following a risk-based approach to combat financial crimes.

Recommendation 20: Reporting Of Suspicious Transactions

Suppose a financial institution suspects that transactions are linked to illicit activity, such as terrorist financing. In that case, it is required by law to report this immediately by submitting a suspicious activity report to the financial intelligence unit (FIU).

Bank AML policy outlines the procedures that banks and relevant staff must follow to prevent financial crimes, including compliance officers, onboarding officers, and money laundering reporting officers.

FATF issues recommendations to help countries develop laws combating money laundering and terrorist financing. Banks must then establish AML policies in compliance with these laws.

Financial institutions must be well-informed about regulatory changes to ensure AML policy compliance in accordance with their jurisdiction’s laws and also with FATF standards.

AML Compliance Policy for FIs in the United States

Several countries, like the U.S., have their own AML laws and regulations that align with global standards. Banks in the U.S are mandated to follow specific AML procedures under the Bank Secrecy Act (BSA).

Bank Secrecy Act (BSA)

To establish an effective AML compliance program, procedures such as customer due diligence (CDD), screening against the Office of Foreign Assets Control (OFAC) economic and trade sanctions, transaction monitoring, and submitting suspicious activity reports (SARs) should be conducted.

As mandated by AML policies and the Bank Secrecy Act (BSA), a risk-based approach is essential for banks to identify and manage potential risks in their operations effectively.

The U.S. PATRIOT Act

The U.S. PATRIOT Act of 2001 was established after 11 terrorist attacks on September 11, 2021. It was introduced to empower the AML/CFT efforts of the U.S. government.

Section 352 requires financial institutions (FIs) to design and implement an effective anti-money laundering (AML) compliance program, which involves several key steps, including establishing Regulations such as PEP screening, internal AML policies and procedures, appointing a compliance officer, conducting staff training workshops, and conducting regular audits.

According to Section 314(b), financial institutions must notify the U.S. Department of the Treasury about suspicious activities linked to money laundering and terrorist financing.

This facilitates the distribution of information across financial institutions (FIs) and the government, aiding in detecting and reporting suspicious transactions.

Section 326 mandates that financial institutions verify the identities of clients seeking to open an account and maintain records of the client’s identity verification, including their name, address, and other relevant data.

Clients must be checked against known or suspected terrorist lists provided by the government to detect entities that have associations with terrorist financing or terrorist groups.

Section 351 provides security to institutions that report suspicious activities without fear of legal consequences.

It also requires financial institutions to refrain from disclosing to individuals that their suspicious activity has been reported to the Financial Intelligence Unit (FIU), such as FinCEN in the U.S., even if a suspicious activity report (SAR) has been filed.

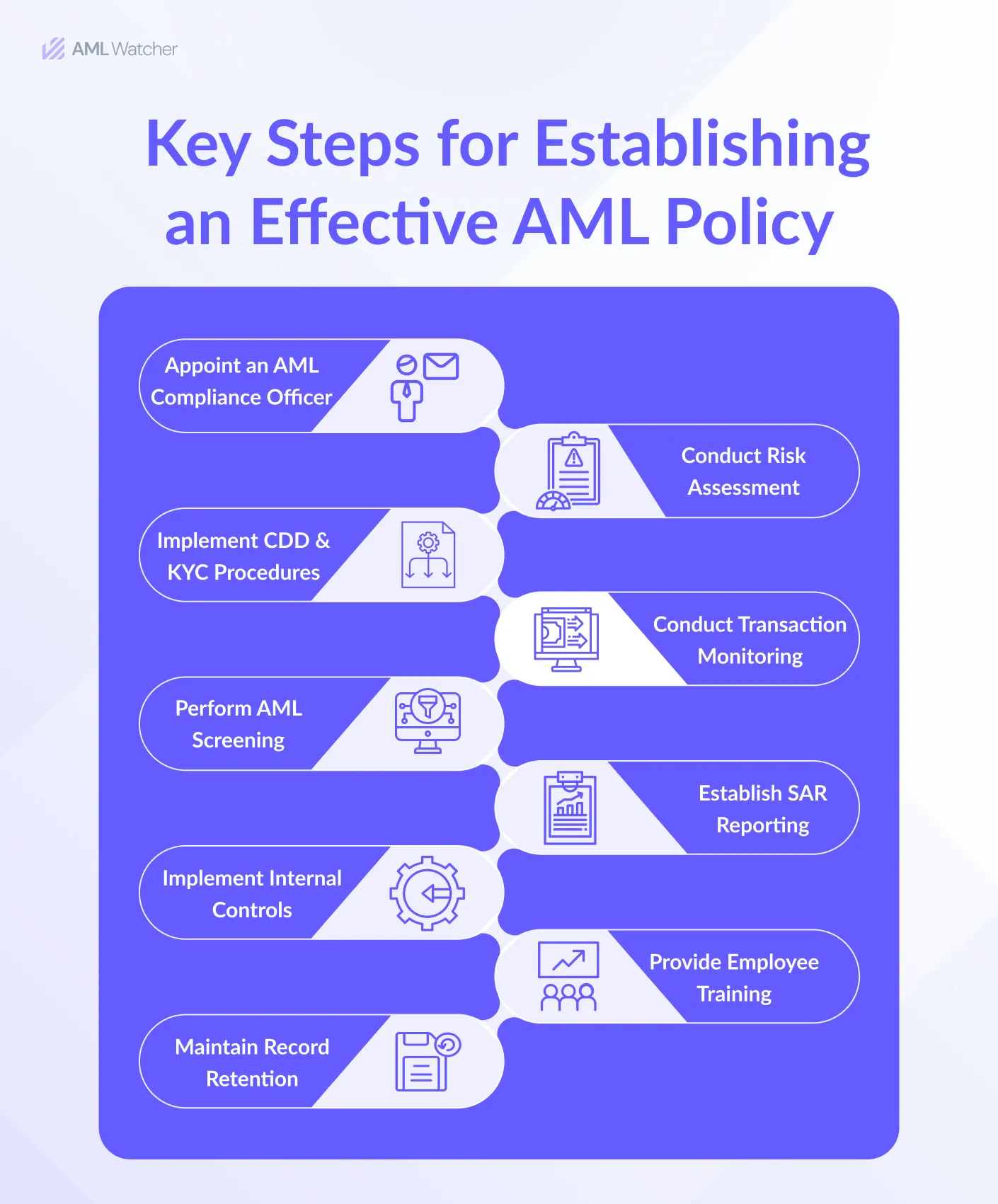

Nine-Step Guide to Establishing a Customized AML Policy

AML obligated entities must create an AML policy to ensure compliance with legal requirements and FATF standards.

The following steps will provide the complete AML policy requirements based on FATF’s recommendations, BSA, and the EU’s Fourth Anti-Money Laundering Directive (AMLD4).

Set the Objective

A company’s AML policy must clearly define its objective by providing concise content, without lengthy introductions, that includes mandatory details to help people understand what it applies to.

Hire a Compliance Officer

Designate a compliance officer who will oversee all AML compliance-related operations.

Responsibilities

- His responsibility will be to evaluate current AML policies and procedures

- Identify areas for growth and ensure all AML polices align with AML laws and global standards

- Implement policies across the jurisdiction to ensure the integrity of the financial organization is maintained.

- An expert compliance officer must be knowledgeable about your industry and company.

- He should have sufficient experience to establish and manage regulatory change.

- He should be intelligent enough to collaborate with other team members and effectively manage issues.

Verification of the Client’s Identity

AML policy must be established in your organization to clearly define the rules and regulations that must be followed for the Know Your Customer procedure.

Describe the appropriate measures that should be taken for verification of client identities and what is required.

Conducting customer due diligence (CDD)

Define the AML policy and procedure for conducting customer due diligence (CDD), and enhanced due diligence (EDD) for clients, including beneficial owners, senior management, and high-risk clients such as politically exposed persons (PEPs).

AML-obligated entities should define their risk appetite and follow a risk-based approach in evaluating clients. Adverse media is often part of ongoing monitoring.

When a client’s name is detected on a sanction or PEP list, and if a client is triggered by adverse media, then ongoing monitoring is necessary for them.

Defining Risk Appetite

Financial institutions must clearly state their risk appetite by defining the level of risk exposure they are willing to tolerate and making decisions like whether to start business relationships with high-risk jurisdictions, such as Russia, Iran, Libya, Syria, and Venezuela, countries that are high risk in the United States.

These decisions should align with the bank’s risk management approach and regulatory requirements to effectively mitigate potential financial risks.

Sanction Screening

Financial organizations must ensure that their clients are not under sanctions by screening their names against sanctions lists, such as the US Specially Designated Nationals List (SDN).

Regulated businesses must establish basic operational procedures to be followed for screening clients against updated sanctions lists, and AML software streamlines this process.

AML software utilizes advanced technologies to expedite processes and minimize false positives.

Submitting a SAR and CTR

The organization’s AML policy must include the processes for submitting suspicious activity reports (SARs) and currency transaction reports (CTRs) to the relevant authorities.

If a currency transaction exceeds $10,000, a CTR must be reported, and the firm will determine under which conditions an STR will be submitted and how it will be submitted.

Submit these reports to FinCEN directly; under certain conditions, the obligation may be transferred to a collaborating bank.

This guide outlines the procedures to be incorporated into the AML policy template. However, it is not a prescriptive rule.

Senior executives, including C-suite leaders, should determine the methods based on the firm’s specific requirements, resources, and alignment with global standards and best practices.

They must assess the risk level of customers and decide the appropriate level of due diligence or enhanced due diligence for high-risk clients.

Collaboration with Law Enforcement Agencies

All AML-related findings must be reported to the relevant authorities and law enforcement agencies in your country to facilitate the distribution of AML information.

Organizations must be aware of the relevant authorities with whom the data will be shared and the channel through which it will be shared.

Exchange of AML Data with Other Firms

Although it is not necessary to share data with financial institutions (FIs), collaborating with other entities can assist you in achieving AML compliance.

Be knowledgeable about the types of information that should be shared and the methods that will be implemented to share the data.

Common AML Compliance Challenges

Financial institutions face several challenges in achieving AML compliance, including staying up-to-date with constantly evolving AML regulations and managing limited resources like personnel and technology.

The high costs of maintaining AML programs can be difficult, especially for smaller institutions. Inaccurate or outdated customer data can lead to failure in customer due diligence and risk assessment.

AML Screening tools often generate false positives, leading to unnecessary investigations and increasing the review time. Additionally, integrating AML solutions with legacy systems can disrupt efficiency and provide poor-quality data.

Strengthen Your AML Policies and Procedures with AML Watcher

AML Watcher enables financial institutions to enhance their AML compliance by providing a robust, customizable screening solution that aligns with specific risk appetites and regulatory requirements.

It offers real-time updates, minimizes false positives, and automates screening processes to reduce manual workloads and improve efficiency.

It integrates seamlessly with existing systems, ensuring smooth implementation without disturbing ongoing operations.

Additionally, it delivers significant cost savings, up to 50% compared to traditional providers, while enabling institutions to tailor compliance strategies to their unique risk profiles and regulatory obligations.

Customer Due Diligence (CDD) and Risk Assessment are essential components of a financial institution’s AML policy.

A robust AML screening solution, such as AML Watcher, enables financial institutions to confidently expand their global operations or diversify their customer base without fearing non-compliance with AML laws.

Institutions can effectively identify and mitigate potential financial crimes by screening global customers against Politically Exposed Persons (PEP) lists, sanctions, watchlists, adverse media, warnings, and regulatory enforcement lists.

The following are features of AML software that support an effective AML policy.

- The sanctions screening process involves screening clients and business partners against sanctions lists issued by government and regulatory authorities to ensure that transactions and entities are not associated with illicit activities.

- PEP Screening screens foreign and domestic PEPs using 100,000+ data sources from any country in the world and gets alerts of updates on PEPs’ Status changes in seconds.

- Adverse Media Screening can help identify adverse media related to individuals or entities, detecting negative press that may indicate financial crimes and thereby improve the due diligence process.

- Custom Risk Scoring provides tailored solutions to help businesses expand their global operations by effectively managing risk. Different levels of risk (low, medium, and high) are evaluated, and the system can be adjusted according to the business’s requirements, regardless of its size or location.

These features can seamlessly integrate into AML policy, automating and improving due diligence processes to ensure risks are identified, alerts are generated, and threats are effectively prevented. Contact us to customize your compliance strategy with AML Watcher’s adaptable risk scoring, aligning with your institution’s unique risk profile.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries