A Guide to Offshore Banking and Money Laundering

Money Laundering

November 13, 2025

em

As per the World Metrics 2025 report, in more than 85% of money laundering cases, the funds actually moved through at least three jurisdictions before appearing legitimate.

This cross-border web of transactions, therefore, makes offshore banking a major vulnerability in the global financial system. These structures make it challenging to learn what’s actually happening by letting the criminals take advantage of different laws in every jurisdiction and hindering regulators from working together effectively. In offshore banking, transactions often move through multiple countries and shell companies, creating layers that hide the actual source of funds. As a result, for compliance leaders, this raises pressing questions: how do they monitor what is barely visible? And is offshore banking illegal? To comprehend these questions, the first thing is to trace how offshore banking evolves.

Offshore banking structures started as tax-planning tools; today, they’ve become a blind spot that sophisticated launderers exploit with growing precision.

This article will assist the readers in letting them know about how offshore banks and money laundering are associated, what risks they pose, and how the teams should respond to these threats.

What is Offshore Banking?

Offshore banking meaning in simpler terms, is obtaining financial services from banks that are not located in their home country. This kind of banking assists the money launderers and criminals in hiding the source of funds and their ultimate beneficial owner.

How Criminals Exploit Offshore Banking for Money Laundering

Through offshore banks, criminals hide their money using jurisdictions with high secrecy and low transparency. Due to limited transparency, strong privacy laws, and weak customer due diligence, it has become easier for criminals to disguise their funds.

Why Does Offshore Banking Remain an Attractive Vehicle for Financial Crime?

There are several reasons why offshore banking attracts financial crime. First, it offers offshore financial services in jurisdictions with favorable tax or secrecy regimes, which criminals and legitimate businesses alike can use for concealing beneficial owners and layering funds.

When oversight is weak, the risk escalates. For instance, the IMF’s 2023 analysis highlights that national AML efforts usually have their emphasis on domestic risk, which leaves loopholes in cross-border oversight and collaboration among regulators. Similarly, the U.S. Treasury’s 2024 NRA also highlights this point by saying that offshore-linked entities and jurisdictions where transparency is limited create vulnerabilities for illicit flows and thereby pose risks to financial system stability.

For offshore banks, the outcome is quite obvious: the illicit funds may enter through complex offshore structures, then re-enter the regulated system, exposing the institution to regulatory, compliance, and reputational harm.

Core Roadblocks for Banks, Fintechs, and Other Regulated Entities

When an offshore bank maps the banking scenario onto its compliance program, the following issues emerge:

a) Opaque Ownership and Shell Structures

Funds may move through AML and offshore banking systems behind shell companies, trusts, or nominee directors, making it difficult to trace the beneficial owner. A transparency gap means the institution’s customer‑risk model is weaker.

b) Cross‑Border Complexity and Jurisdictional Gaps

Transactions slice through multiple countries, time zones, and legal frameworks. One bank’s “ordinary transfer” may correspond to another jurisdiction’s “questionable layering” event. The regulatory burden increases accordingly. For instance, more than one‑third of EMEA institutions ranked “regulatory pressure” as their top AML challenge in a 2024 survey.

c) False Positives and Wasted Resources

Because offshore flows often look “high risk” by default, compliance teams receive elevated alerts, many of which are benign. That uses valuable investigator hours and can degrade overall effectiveness.

d) Limited Monitoring of Adverse Media and Reputational Risk

Traditional screening may capture sanction lists or PEPs, but not always the hidden reputational chatter tied to a customer’s involvement in adverse media. Offshore banking is legal, but whether it is being exploited by someone associated with high-risk activity is known by additional signals from media monitoring.

e) Emerging Channels and Transaction Typologies

Offshore banking risks in AML are further enhanced or augmented if the transaction of the customer in question is additionally associated with digital assets, crypto‑corridors, remote account openings, and trade‑based laundering. Those unfamiliar terrains amplify vulnerability.

For a CRO or Head of Financial Crime, juggling these complexity layers while also needing to ensure the business stays operational, cost‑efficient, and well‑positioned for regulatory evolution demands, a comprehensive monitoring framework that improves visibility without delaying operations is needed.

How Advanced Screening and Monitoring Address Offshore Banking Risks?

In the face of the above pain‑points, the right solution medium does three things well: visibility, precision, and resilience.

-

Visibility Across Global Counterparties and Jurisdictions

To assess the risk of customer accessing offshore banking services, respective financial institutions may have to screen against wide‑ranging data: sanctions and PEP lists across multiple countries, adverse‑media feeds in many languages, entity‑relationship graphs that surface hidden beneficial‑owners and network links. Without this breadth, overseas banks can have blind spots.

-

Precision in Linking High‑Risk Profiles and Reducing Noise

Offshore banks must move beyond simplistic “volume‑based” alerts to intelligent matching, alias resolution, phonetic and transliteration checks, entity clustering, and continuous monitoring. Research has shifted this toward intelligence-driven detection. A report on “Enhancing Anti-money laundering efforts with Network-Based Algorithms”, showed how network‑based algorithms can detect hidden cycles beneath regulatory thresholds, signaling layered laundering efforts. This leads to minimizing the false alerts and prioritizing the actual problems.

-

Flexibility to Adapt the Evolving Regulations and Criminal Typologies

Regulators and criminal typologies evolve swiftly. The solution should handle emerging channels (crypto wallets, digital‑asset entities), adapt to new sanctions regimes, and monitor adverse media and reputational signals in real time. As the European Banking Authority(EBA) noted in its opinion on money laundering and terrorist financing risks affecting the EU’s financial sector, the ML/TF landscape is “dynamic and increasingly complex”.

What Things are Obligated to Do for an Effective Monitoring Lifecycle

Here is a list of steps that help the offshore bank in implementing an effective monitoring lifecycle that ensures transparency across its international customer base. These steps are:

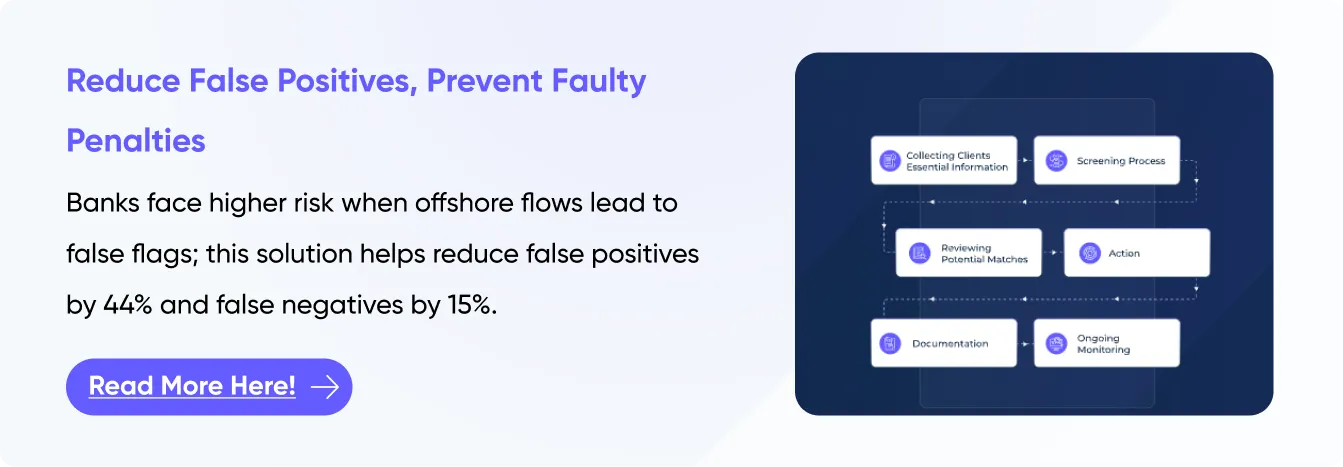

- Onboarding: When a new corporate customer opens their account, it is the responsibility of the offshore banks to check the entity’s jurisdiction, source of funds, and beneficial ownership.. At this moment, overseas banks are obliged to map beneficial ownership and apply enhanced due diligence (EDD).

- Continuous Tracking: Risk assessment during customer onboarding is not enough. Continuous monitoring is needed to detect suspicious transactions. The second step is to review whether transactions involve any suspicious activity or not. Offshore banks must watch for rapid layering, frequent cross‑border transfers, unusual patterns suggesting layering, and involving shell companies.

- Adverse Media and Reputational Overlay: Offshore banks should screen the individual, entity, and their network against adverse media mentions and regulatory actions. Such detection saves overseas banks from reputational damage that formal databases might ignore.

- Alert prioritization: For high‑risk offshore flows, risk-based alert prioritization plays a crucial role in targeting the genuine alerts. For instance, if a customer X uses an offshore bank in jurisdiction Y, then they probably need the recent adverse media link and the current large split transfers for that client. This will help them catch the actual issue with the client rather than wasting time on thousands of generic flags.

When this process is performed effectively, an offshore bank can smoothly shift from reactive ( flagged once, but the funds had already moved) to proactive (surfaced the pattern early, stopped the funds, notified relevant parties), which is exactly what modern investigators demand.

How to Choose the Right AML Screening Platforms?

For offshore banks that are serving clients from different jurisdictions or who simply want to future‑proof their screening, monitoring, and alert workflows, there must be platforms that:

- Covers all relevant jurisdictions and data types.

- Can detect hidden‑ownership links, alias networks, and layering behavior.

- Monitors adverse media, reputation, and emerging typologies (crypto wallets, remote accounts, small‑scale layering).

- Supports custom risk scoring, automated alerts, and continuous monitoring so offshore investigators focus on the right issues, not noise.

- Keeps pace with regulation, typology shifts, and jurisdictional changes so the offshore banks’ defenses remain resilient and forward‑looking.

Assesses Customers Risk Associated with Offshore Banks

Struggling to get ahead of offshore-bank‑related money‑laundering risk? Let AML Watcher assist you with this:

- Global coverage of sanctions, PEPs, and adverse media across 235+ jurisdictions, by which entities and customers can be verified even if they are in hard-to-track offshore or secrecy jurisdictions.

- Advanced name‑matching, alias resolution, entity‑linkage, and network‑detection to provide the bigger picture of the customers or related entities.

- Customizable risk‑scoring, continuous real‑time monitoring, and emerging typology support to tailor the due diligence depending upon the entity’s risk score.

Reach out today to engage our expert team and see how AML Watcher can help you move from reactive monitoring to proactive defense.

Move Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries