How AML Identity Verification Sets the Basis for Accurate Risk Assessment

Anti Money Laundering

September 19, 2025

Money laundering is a global threat that disrupts financial ecosystems, fuels crime, and damages trust. In response, regulators are tightening expectations, especially around KYC measures.

Identity verification is not just a step in onboarding; it is central to the structure of modern AML compliance. But without timely, accurate, and context-rich AML screening data, even the best KYC solutions are not able to ensure accurate risk assessments.

What is the Difference Between AML and Identity Verification

Before digging into regulatory obligations, let us first understand the difference between AML and Identity Verification (IDV), and how these two tools work together in compliance.

- AML is a broad compliance function. It refers to the set of laws, regulations, policies, and procedures designed to prevent criminals from hiding proceeds of illicit activity, financing of terrorism, corruption, or other financial crime. Some critical elements of AML checks include:

- Customer Due Diligence (CDD)

- Screening

- Transaction Monitoring

- Record-keeping

- Reporting to the relevant authorities

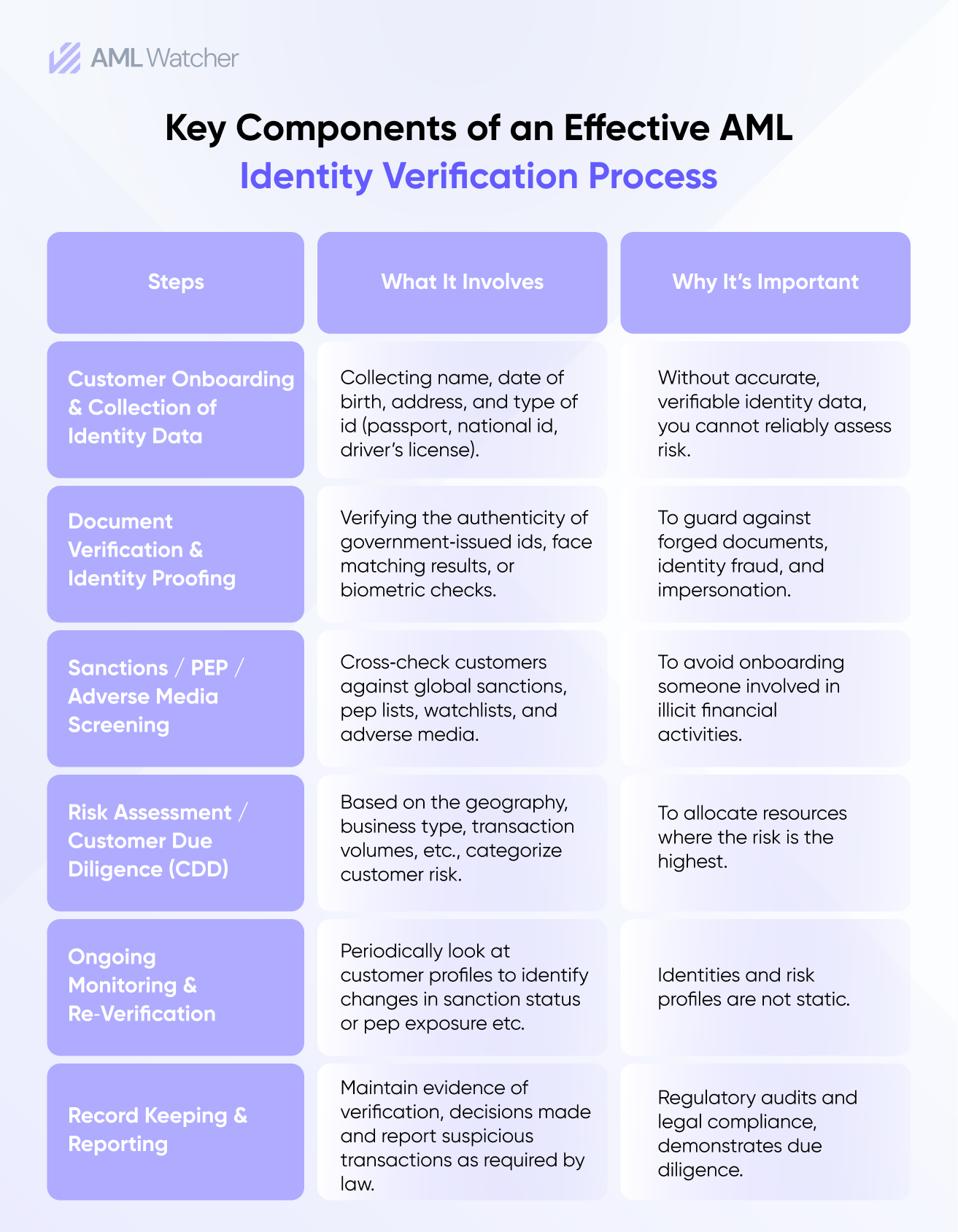

While Identity Verification (IDV) serves as the first critical step in ensuring a legitimate customer, it lays the foundation for the next phase of compliance: Know Your Customer (KYC), where in-depth risk assessments and ongoing monitoring come into play.

Without a strong IDV, AML ID verification fails at the first hurdle. Without ongoing AML intelligence, IDV lacks context. This is why KYC providers must integrate high-quality AML data into their verification workflows to deliver full-spectrum compliance.

Why Does AML Identity Verification Process Matter:

The intersection of AML and Identity Verification is where compliance and risk management converge. Without proper verification of identity, the customer’s accurate risk assessment is not possible. Here is why AML and Identity Verification are essential:

1. The Gateway to Financial Systems Must Be Secure

Identity verification is the first gatekeeper to any financial or digital service. If that gate is weak, the entire AML framework collapses. Fraudsters exploit gaps in IDV to create synthetic identities, use stolen credentials, or establish seemingly legitimate accounts to launder money later.

- A weak identity check enables the onboarding of high-risk or criminal entities into the financial system.

- Once inside, these bad actors exploit transaction systems, payment platforms, and corporate structures to layer and integrate illicit funds.

It is thus imperative for a KYC solution system to be robust in the identification of customers. Given that IDV is the gateway to financial systems, errors in the identification of customers may lead to inaccurate AML risk assessments.

2. Significance of Ongoing AML Monitoring

A customer who passed IDV today might become a politically exposed person (PEP) tomorrow, get sanctioned next week, or appear in adverse media in a different language.

That’s why ongoing AML monitoring is inseparable from identity verification in today’s regulatory climate. Without continuous screening, KYC solutions can only promise a moment-in-time view, which is insufficient for risk-based compliance models.

3. Fraud and Financial Crime Have Evolved — So Must Verification

Modern financial crime is fast, cross-border, and tech-enabled. From deepfake IDs to trade-based money laundering, criminals don’t think in silos, and so compliance systems can’t either.

An Identity document alone is not sufficient to tell if a person is in a global criminal watchlist. or if they’ve been involved in environmental crime, drug trafficking, or corruption. That insight comes from real-time, multilingual, categorized AML data, applied soon after the legal identity of a customer gets confirmed. Both the verification of identity and the associated AML risk of a customer are crucial for financial institutions to analyze the money laundering risk associated with them and then decide the course of action.

For KYC providers, this is a value-add: helping clients avoid onboarding a sanctioned shipowner, a cartel-linked shell company, or a politically exposed embezzler, other than helping them comply with the Customer-Identification Program.

What Does The FATF Recommend For Effective AML Verification

The Financial Action Task Force (FATF) establishes international standards designed to prevent money laundering and terrorist financing. Specifically:

- Recommendation 10 – Customer Due Diligence (CDD): Financial entities shall utilize a reliable, independent source of documents and data to verify the identity of a customer.

- Recommendation 12 – Politically Exposed Persons (PEPs): Enhanced due diligence must be applied to PEPs to mitigate corruption-related risks

- Recommendation 20 – Reporting of Suspicious Transactions: Firms must monitor customer activity to report any suspicious transactions to competent authorities.

The FATF recommendations mean that financial institutions require KYC solution providers that go beyond simple verification of ID. Instead, KYC solution systems require high-quality AML data that enables accurate verification, risk scoring, and continuous monitoring, aligning with FATF Recommendations. This approach not only verifies who someone claims to be but also assesses who they truly are.

Best Practices in AML ID Verification

To make the process not only compliant but also efficient and user‑friendly, these practices emerge repeatedly:

- Integrating high-quality, real-time AML data from trusted sources helps refine risk scoring and ensures accurate identification of potential threats, reducing false positives.

- Automate the process of AML Verification, but leave room for human approval for high-risk cases.

- Apply a risk‑based approach so that low-risk customers have fewer hurdles, while high-risk cases get more scrutiny.

- Ensure fast update/refresh of sanctions / PEP / adverse media data to increase effectiveness.

How AML Watcher’s AML & Identity Verification Measures Close the Gap

Identity verification isn’t just a front‑door requirement—it must be deeply integrated into AML strategy. AML Watcher is built to address the challenges above, delivering a cohesive AML solution. Here’s how:

- Data-Powered Identity Risk Insights

Enhanced AML risk detection by supplying enriched sanctions, PEP, and adverse media data that can be consumed by KYC platforms in real-time – allowing providers to assign risk scores at the time of onboarding and beyond, based on comprehensive global intelligence. - Real-Time Updates

High‑quality AML data that is updated every 15 minutes (across sanctions regimes, PEPs, adverse media, etc.) to help reduce unnecessary alarms and improve overall verification accuracy. - Biometric AML Screening that Goes Beyond Name-Matching

Identity-anchored AML risk screening by accepting facial images, IDs, and passport numbers. This biometric screening capability compares facial data against over 3,500 global watchlists across more than 235 jurisdictions using advanced facial recognition technology. Clients using this approach have reported a 44% reduction in false positives as compared to their previous AML Screening vendor, and 90% fewer manual reviews, giving you a Biometric AML Screening solution that anchors risk to verified identity. - Automated workflows, risk-based verification

Supports risk‑based verification: low-risk customers proceed quickly; higher-risk cases trigger enhanced checks. Automation of this workflow significantly reduces the need for manual input, resulting in fewer delays. - Ongoing monitoring and re‑verification

Continuous monitoring for changes (such as new sanctions, adverse media, and changes in ownership). A customer may be low-risk at the time of onboarding, and become high-risk later on. AML Watcher flags high-risk customers through continuous monitoring. - Compliance, audit trail, and documentation

Keep detailed records, including the ID checked, when it was checked, and which risk flags were triggered, making audits easier and more defensible.

By integrating comprehensive AML data, including advanced biometric screening and real-time updates, AML Watcher empowers KYC providers to enhance their identity verification processes, ensure regulatory compliance, and effectively mitigate financial crime risks.

Frequently Asked Questions

Typically required documents include government-issued IDs (passport, driver’s license), birth IDs, and utility bills. In some cases, biometric data like facial images or fingerprints may also be used to verify identity.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries