Decoding the Strategic Value of the 5 Pillars of AML Compliance

AML Compliance

January 14, 2025

- What are the Pillars of an AML Program?

- Fairbrother and Darlow’s Compliance Failure – Lesson Learned

- Regulatory Guidelines Stressing the Importance of Five Pillars of AML

- What are the Regulatory Tips for Establishing AML Compliant Programs?

- How AML Watcher Assists Organizations in Creating Successful AML Compliance Programs?

“The anti-money laundering laws are critical for maintaining trust in financial systems and ensuring that the proceeds of crime do not disrupt legitimate economies.”

-International Monetary Fund (IMF)

With the ever-growing instances of unauthorized financial practices, institutions are severely affected by the imposter’s money laundering trails.

As a result of these threats, approximately 3-5% of the global Gross Domestic Product is laundered annually. Therefore, formulating effective AML guidelines based on several regulatory pillars is highly important.

At the backend of every resilient financial operation lies an effective and credible anti-money laundering framework that is established based on its core pillars.

The foundation of credible AML compliance programs revolves around several regulatory pillars. The 5 pillars of AML programs are more than just the regulatory mandates; they form the foundation of transparent and trustworthy financial measures.

As per Title 31 of the Code of Federal Regulations, there are five regulatory requirements that all financial institutions must employ. Under this act, the designation of a compliance officer, establishment of a risk assessment approach, development of internal controls, establishment of AML programs, and CDD checks are required for secure business operations.

To understand the significance of each of the 5 pillars of AML compliance program, read the information given below:

What are the Pillars of an AML Program?

The 5 pillars of anti-money laundering compliance programs assist financial institutions in detecting, preventing, and reporting malicious activities like money laundering and terror financing. Businesses must build their anti-money laundering practices based on these 5 pillars of compliance.

The Bank Secrecy Act enacted in 1970 forms the foundation of the AML pillars. Under this act, all the AML policies must align with these crucial pillars. The filing and reporting of suspicious financial operations and illicit transactions are emphasized to prevent money laundering.

Let’s understand the significance of each of the 5 pillars of AML and their role in regulating the business structures.

The First Pillar: Nomination of a Compliance Officer

The first pillar of the AML compliance program is to appoint a compliance officer who oversees the functioning of the entire program.

One of the crucial duties of a designated AML compliance officer is to ensure that the company complies with the regulatory laws while regularly updating the company’s guidelines.

Article 8 and Chapter 6 of EU directive 2015/849 emphasize the compliance officers to comply with the global AML/CFT guidelines.

The key skills that must be ensured by the compliance officers include:

- The compliance officer must be informed about the legal obligations that are developed by the global regulatory bodies.

- It is essential for the AML compliance officer to regularly inspect the company’s financial departments while identifying the training requirements to boost financial integrity.

- The compliance officer is responsible for overseeing and monitoring the company’s internal governance to ensure compliance with the global AML guidelines in order to counter money laundering.

The Second Pillar: Risk-Assessment Approach

To ensure the effectiveness of the five pillars of AML program, the compliance measures must be centralized across a risk-based approach.

This calls for the development of a tailored screening program in which customer assessment is conducted based on the risk level they possess.

Customer’s risk levels are not static; therefore, continuous monitoring and updation of their risk profiles is crucial. Institutions are required to assess the customer’s risks through the following processes:

- The compliance officers must specify the company-specific risks to understand the probability of money laundering operations.

- Customer search profiling is an important aspect of the pillars of AML, as it focuses on categorizing the customers according to their risks. The risk levels are identified by their exposure and recognition in several PEP, sanction, and watchlists.

Customers who actively conduct business operations in high-risk jurisdictions are deemed speculative. This requires the implementation of intensive regulatory scrutiny during the real-time transaction monitoring checks.

The Third Pillar: Internal Policy Development

This pillar emphasizes that businesses draft internal policies to ensure a seamless detection of money laundering practices.

The policies that are formed to specifically tackle the organizational risks significantly prevent money laundering operations.

During the development of internal controls, every employee must be trained on the applications and tools used to assess customers’ risk profiles.

The internal AML compliance controls involve the following elements:

- Suspicious activity reporting

- Preservation of the company’s records

- Tailored transaction screening rules

The Fourth Pillar: AML Program Auditing

The regular auditing of the AML compliance programs by accredited third parties is essential to identify the loopholes that may create discrepancies during customer risk assessment operations.

The auditor must be able to effectively tackle the weak points that could affect the credibility of an institution’s AML regulatory practices.

According to the FATF’s AML requirements, the high-risk sectors are required to undergo frequent regulatory audits to reduce the intensity of financial crimes.

Businesses are required to incorporate data-driven modules to adapt to the evolving money laundering risks in different sectors.

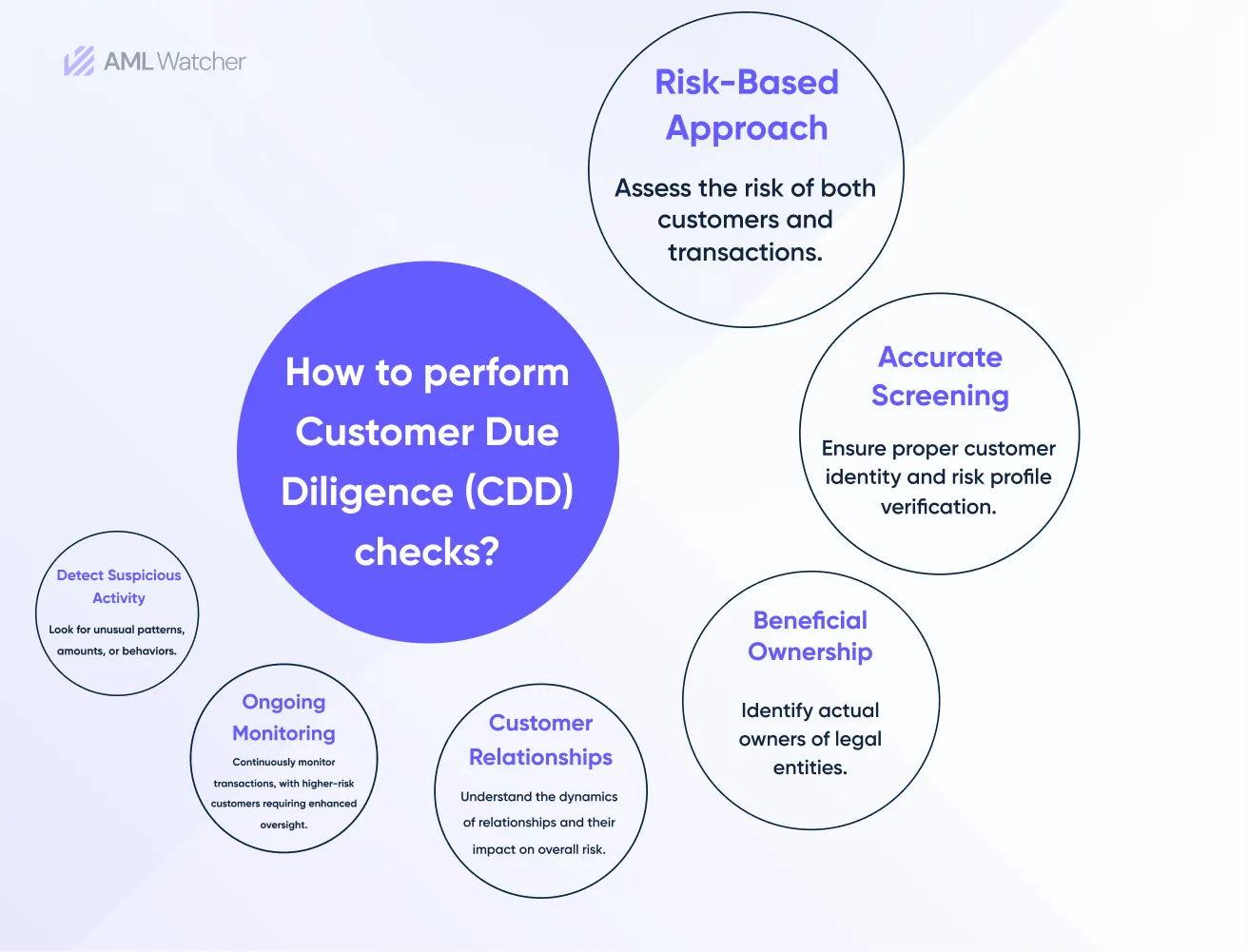

The Fifth Pillar: Customer Due Diligence Programs

Recently, customer due diligence has been identified as an important pillar of the AML compliance programs by FinCEN.

This pillar stresses continuous monitoring of the customer’s identity and risk profiles. Due to the growth of money laundering concerns, CDD checks serve an important purpose.

Background checks during the CDD process guide the compliance officers in understanding the customer’s involvement in various financial activities.

Moreover, the identification of the legal entity’s true owners and UBOs is also highlighted through the CDD process.

This intensive client risk assessment process enables businesses to take precautionary measures during the money laundering assessment.

Fairbrother and Darlow’s Compliance Failure – Lesson Learned

In 2024, Fairbrother and Darlow, a Berkshire law firm, was charged with a fine of £16,000 for their insufficient regulatory controls for over six years.

Due to the lack of structured risk assessment and internal policy controls, the Solicitors Regulation Authority (SRA) initiated the fine.

The firm failed to comply with the SRA’s regulations, which was regarded as a serious threat to the public interest. This pattern of non-compliant business operations led the firm to pay a hefty amount to avoid future disparities.

Implications of Case

This case highlighted the significance of adhering to the five pillars of AML program in order to avoid financial penalties in the long run.

Adherence to the components of the AML compliance programs is crucial to avoid the repercussions of financial penalties.

Additionally, an emphasis on enhanced regulatory oversight and accountability is crucial to protecting the firm’s integrity.

Regulatory Guidelines Stressing the Importance of Five Pillars of AML

The formulation of effective AML programs is guided by several regulations that determine the basic guidelines for countering financial crimes.

These regulations generally vary by the jurisdictions under which the institutional activities are conducted. Some of the renowned AML compliance regulations that comply with the crucial five pillars are:

FATF Recommendation 18

The 18th recommendation proposed by the Financial Action Task Force stresses that FIs establish streamlined internal controls during the formulation of AML regulations.

Adequate customer record-keeping, risk profiling, and transaction monitoring are promoted under this recommendation. The ultimate aim of this regulation is to minimize criminal money laundering practices.

USA Patriot Act (Section 352)

Section 352 of the USA’s patriot act puts a strong emphasis on establishing AML programs in which adequate employee training is promoted.

All the major US insurance companies, non-traditional financial service providers, and precious metal dealers are mandated to comply with the pillars of AML.

Code of Federal Regulations (CFR)

As determined by FinCEN’s CFR guidelines, title 31 addresses the significance of the 5 AML pillars.

Under this law, the provision for filing transactional reports, maintaining the customer’s financial records, and designation of trained compliance officers is highlighted.

What are the Regulatory Tips for Establishing AML Compliant Programs?

The effectiveness of any AML regulations depends on several development strategies that must be addressed and recognized. Some of these critical tips include:

- A sound AML policy must be clearly understood by employees at all levels. Additionally, periodic reviews and updations must be considered to avoid non-compliance issues.

- The regulation’s KPIs must be identified to understand the importance of these specified regulations. This is because the KPIs differ according to the risk levels of various jurisdictions.

How AML Watcher Assists Organizations in Creating Successful AML Compliance Programs?

Financial institutions may handle important AML compliance issues with the help of AML Watcher’s complete AML screening solutions.

AML Watcher may not directly offer each of the five pillars of AML compliance, its screening tools greatly enhance key areas of compliance.

While AML Watcher does not appoint a compliance officer but assists them with its screening tools to accelerate procedures, strengthen internal controls, and minimize human error to ensure successful AML compliance.

How?

Through its:

1. Real-Time Risk Assessment

AML Watcher conducts real-time risk evaluations on transactions and customers by checking against PEP databases, international sanctions lists, and negative news outlets.

Offers proactive insight into possible risks, facilitating prompt action and minimizing the need for manual assessment for high-risk operations.

2. Global Sanctions and PEP Screening

Screens transactions and clients against more than 230 international sanctions lists, such as those maintained by the UN, EU, OFAC, and other PEP databases.

Reduces vulnerability to organized crime, terrorism, and corruption by automatically detecting high-risk persons or companies, ensuring that institutions remain sanctions-compliant.

3. Detailed Due Diligence

Customer Due Diligence (CDD) and Enhanced Due Diligence (EDD) guarantee comprehensive background checks for clients, particularly for high-risk people or organizations, including transaction history and the source of money.

Assists financial institutions in adjusting due diligence to each customer’s risk profile, preventing possible financial crimes, and guaranteeing adherence to international AML laws.

4. Adverse Media Screening

Natural Language Processing (NLP) technology scans news articles and media publications to look for connections to illegal activities or unfavorable connotations.

Adverse Media screening improves the due diligence procedure, by spotting possible dangers in media stories and facilitating more educated choices about high-risk clients.

5. Quick Transaction Monitoring

Transactions are continuously monitored to identify any suspicious trends, such as huge wire transfers, quick fund movements, or cross-border transactions that could point to illegal conduct.

The ability to automatically identify and halt questionable transactions reduces risk and guarantees prompt regulatory compliance for institutions.

6. Customized Risk Scoring

AML Watcher offers adaptable risk-scoring models that are based on a variety of variables, including industry, geography, and transaction history.

Enhances risk management and boosts operational effectiveness by enabling companies to prioritize and concentrate efforts on the most vulnerable customers.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries