What Compliance Leaders Must Know About FATF Travel Rule

AML/CFT

January 6, 2026

Cryptocurrency transactions are designed in a way that the identities of both sender and receiver remain pseudonymous. Instead of names and account numbers, the transactions depend on wallet addresses that are long strings of characters. These addresses offer visibility into transaction flows but do not expose who is sending or receiving funds. This creates an ongoing compliance challenge for the virtual asset service providers (VASPs) and conventional financial institutions operating in the same space.

Unlike conventional banking, where the customer identities are fully verified at onboarding, cryptocurrency transactions typically involve:

- Self-hosted crypto wallets controlled directly by individuals, with no intermediaries.

- Real-time, international crypto transactions.

- Multiple wallets controlled by a single entity, or one wallet used by many entities.

- Funds routed across different blockchains, exchanges, and decentralized platforms in rapid sequences.

This nature of cryptocurrency exploits gaps in identity and ownership transparency and exposes financial institutions to regulatory sanctions, AML risks, and reputational damage. To tackle these risks, FATF has extended its travel rule that now covers virtual asset transfer conducted by VASPs in compliance with evolving regulations. This rule is not just a regulatory requirement; it’s a crucial component of operational risk management in an increasingly digital financial landscape.

This blog will break down the FATF Travel Rule and its global adoption by different jurisdictions.

Understanding the FATF Travel Rule

The FATF Travel Rule is actually a requirement for the virtual asset service providers (VASPs) and financial institutions that aim to collect and transmit information about the beneficiaries and originators in certain transactions. Originally designed for traditional wire transfers, the rule now extends to virtual assets, including cryptocurrency transactions, whenever parties exceed designated thresholds.

FATF recommends a threshold of USD/EUR 1,000 for travel rule application, however, this differs from country to country and VASPs need to carefully review the requirements of the jurisdiction in which they operate. For example, in the USA it’s $3,000 in Canada CAD 1,000 whereas in EU it’s zero, meaning Travel Rule requirements apply regardless of amount or domestic/cross-border transfers of virtual assets.

Its core objective is straightforward: ensure that transaction data “travels” with the transfer, making it possible to trace funds, detect suspicious activity, and prevent misuse for money laundering or terrorist financing. Originator and beneficiary information typically includes names, account or wallet numbers, and identifying details such as addresses or national IDs.

Why FATF Travel Rule Compliance is Necessary

FATF Travel Rule compliance is necessary to ensure compliance with requirements like asset freezing and prohibiting transactions with the designated persons. For financial institutions and VASPs, it is also essential to comply with the Travel Rule because it helps them in performing:

Effective counterparty screening with standardized transfer data makes it easier to assess the associated financial crime risk.

Enhanced money laundering detection where financial institutions gain additional identity context related to originators and beneficiaries.

Operational Alignment, where structured, automated data exchange supports faster enforcement and more accurate monitoring across global payment ecosystems.

To support effective oversight of international crypto transactions, it is important to have these measures in place during the digital asset era.

FATF Travel Rule and Its Role in Sanctions Compliance

For Institutions that implement the Travel Rule, sanctions screening becomes a mandatory operational outcome, not an optional control.

When banks and crypto companies send a client’s payment, they must also collect and share details about who is sending the money (originator) and who is receiving it (beneficiary). Regulators now expect these companies not just to pass on this information, but also to check it against the sanctions list, with whom they are restricted from performing any business dealings. Simply transmitting originator and beneficiary information is insufficient; regulators expect institutions to screen this data against applicable sanctions lists and demonstrate that effective screening controls are in place.

Practically, this means:

- To screen the beneficiaries and originators properly before they send or receive money.

- The travel data should be checked against terrorist financing, watchlists, and global sanctions lists such as the Office of Foreign Assets Control (OFAC), HM Treasury (HMT), EU, and UN Sanctions list.

- Transactions where any alert related to sanctioned entities triggered must be blocked, declined, or reviewed further according to what the law demands.

Regulators now view unscreened Travel Rule data as a serious weakness in anti-money laundering (AML) efforts, especially in international and cryptocurrency transactions. Therefore, compliance with the Travel Rule is incomplete without sanctions screening. Lack of this screening can also put institutions at risk of enforcement actions, compel them to implement the fixes, and damage their reputation.

Travel Rule Expansion to VASPs

Since 2019, the Financial Action Task Force (FATF) has formally extended the Travel Rule to VASPs, including crypto exchanges, custodial wallet providers, trading and transfer platforms.

This expansion reflects the growing volume and complexity of virtual asset transactions. However, applying a rule designed for banking to decentralized and pseudonymous systems introduces operational challenges, particularly when transactions involve wallets outside VASP control.

Who Needs to Comply with FATF Travel Rule

Many people have this misconception that the Travel Rule only applies to cryptocurrency companies. However, this rule actually started in traditional banking and still applies fully to banks and other financial institutions.

Long before virtual assets, the Travel Rule governed:

- Cross-border wire transfers

- Correspondent banking relationships

- Payment messages exchanged through traditional rails

What has changed is the asset class and transaction environment, not the regulatory expectation.

Today, banks increasingly interact with crypto exchanges, payment intermediaries, and clients moving between fiat and virtual assets. Regulators, therefore, expect banks to:

- Apply Travel Rule controls consistently across fiat and crypto-related transfers

- Screen crypto-linked counterparties using the same sanctions standards as traditional payments

- Ensure interoperability between core banking AML systems and Travel Rule data flows

For banks, the Travel Rule is no longer a peripheral crypto issue; it is a core cross-channel AML obligation.

State of Global Compliance with FATF Travel Rule in 2026

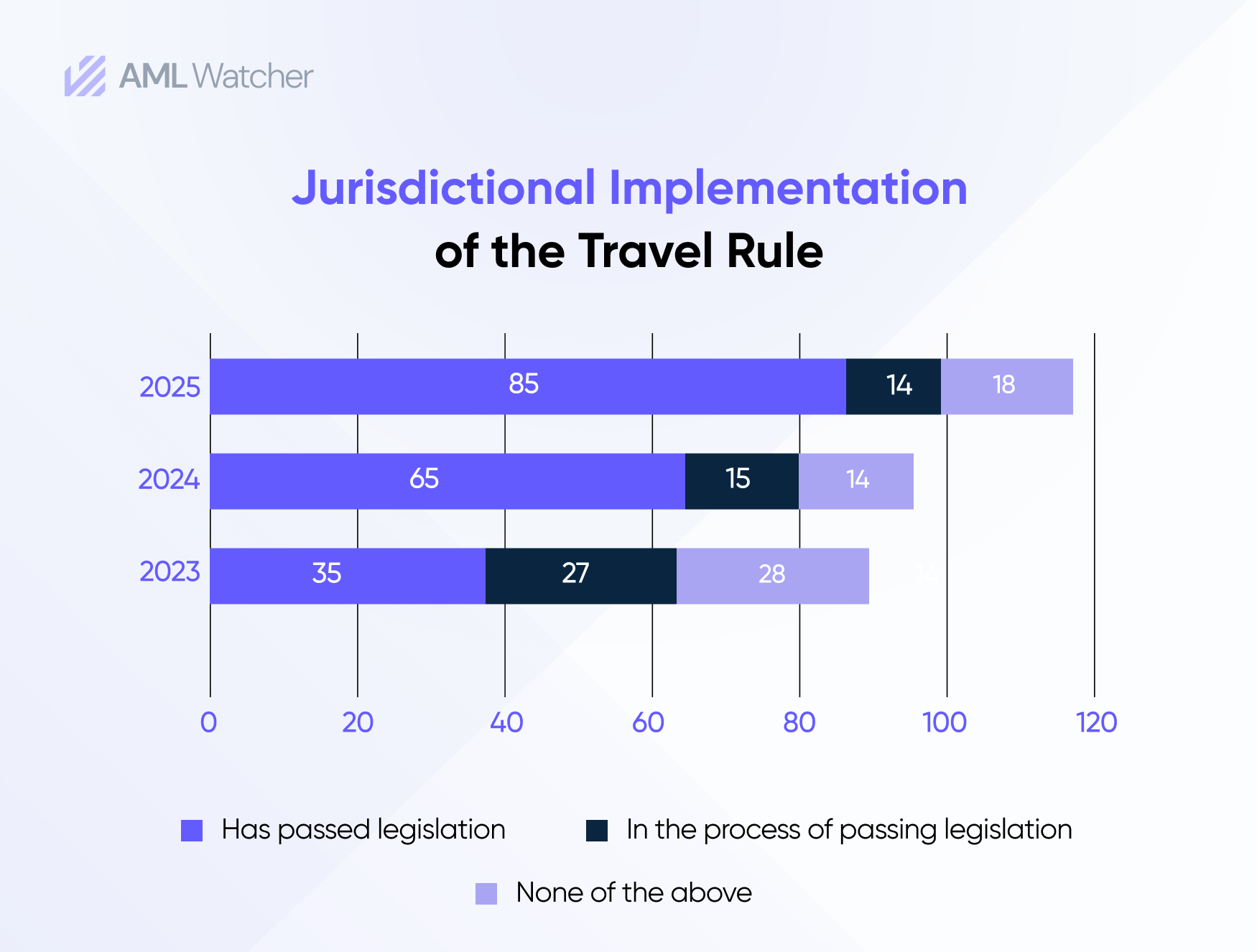

As of 2025, the adoption of the FATF Travel Rule has significantly increased since earlier years, but global implementation and enforcement remain uneven. FATF and the Global Network comprise 205 jurisdictions in total, but only 163 responded to the survey. The jurisdictions that did not participate were treated as not having implemented the requirements.

According to FATF’s Best Practices on Travel Rule Supervision report, 99 jurisdictions have either enacted or are in the process of enacting legislation to implement the Travel Rule. This marks a significant increase compared to previous years and reflects growing alignment with FATF Recommendation 16 on transparency in international payments.

Within that total number of 99 jurisdictions:

85 jurisdictions out of 163 have passed legislation or formal regulation implementing the Travel Rule against virtual assets and service providers, compared to 65 jurisdictions last year. An additional 14 jurisdictions reported that they are actively working toward rule implementation.

These figures usually refer to jurisdictions that do not completely ban Virtual Asset Service Providers (VASPs) or keep them out of regulatory frameworks. This means the whole focus is on countries that choose to regulate crypto activities instead of prohibiting them.

However, implementation in law doesn’t always translate into effective enforcement:

Many jurisdictions that have passed Travel Rule legislation have not yet established robust supervisory frameworks or taken enforcement action against non-compliant entities. According to the 2025 Targeted Update on Implementation of FATF Standards on Vasps, a majority of jurisdictions (approximately 59% of those with laws) have yet to issue supervisory findings, directives, or enforcement actions tied specifically to Travel Rule compliance.

This enforcement gap partly reflects the recency of many laws and the complexity of operationalizing Travel Rule requirements, especially given interoperability challenges and resource constraints in supervisory agencies.

Such fragmentation creates cross-border compliance challenges known as the “sunrise issue”. This usually occurs when VASPs in compliant jurisdictions must exchange Travel Rule data. They have to exchange it with counterparts in jurisdictions that are in the process of implementation or are only partially compliant, which complicates the transaction flow.

Understanding these adoption and enforcement gaps is crucial, as they directly impact how VASPs navigate cross-border transactions and comply with evolving Travel Rule obligations.

Why Compliance with Travel Rule Is Still a Challenging Task

Even in the regulated jurisdictions, the practical implementation of the FATF Travel Rule remains a challenge for the financial institutions and VASPs. They face the following complexities during the rule implementation:

- System Incompatibility: When there are different Travel Rule solutions and protocols, they do not work well together, which creates difficulty in information sharing.

- Unhosted Wallets with no Intermediaries: When the crypto is sent directly from a customer’s personal wallet, it usually has no intermediary involvement that later complicates the verification of the sender and the receiver.

- Limited Regulatory Experts: There are some regulators who lack regulatory expertise and knowledge, which complicates the monitoring and compliance enforcement.

- Cross-Border Complexity: different timelines and interpretations of the Travel Rule can result in increasing the functional risks.

These challenges mean that Travel Rule compliance is not just a legal issue; it is an operational one.

Strengthen Travel Rule Compliance with AML Watcher

Many compliance teams collect Travel Rule fields but still struggle to convert them into decisions that reduce sanctions and ML risk.

AML Watcher supports Travel Rule programmes with originators and beneficiaries against sanctions, PEPs, and adverse media in real time to strengthen transaction controls. The platform helps to minimize false positive review time and compliance costs through an adaptable screening process powered by Artificial Intelligence and proprietary database.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries