Everything You Need to Know About Single Customer View (SCV)

AML Compliance

February 12, 2026

Many financial institutions hold customer data into onboarding tools, core banking systems, payment rails, CRM platforms, and case management queues. When customer profiles remain in disconnect systems, risk signals also stay fragmented. That gap slows investigations, weakens ongoing monitoring, and creates inconsistent customer risk decisions.

A Single Customer View (SCV) addresses this by unifying identities and interactions into one customer profile that teams can trust for AML controls and risk management.

What is Single Customer View (SCV)?

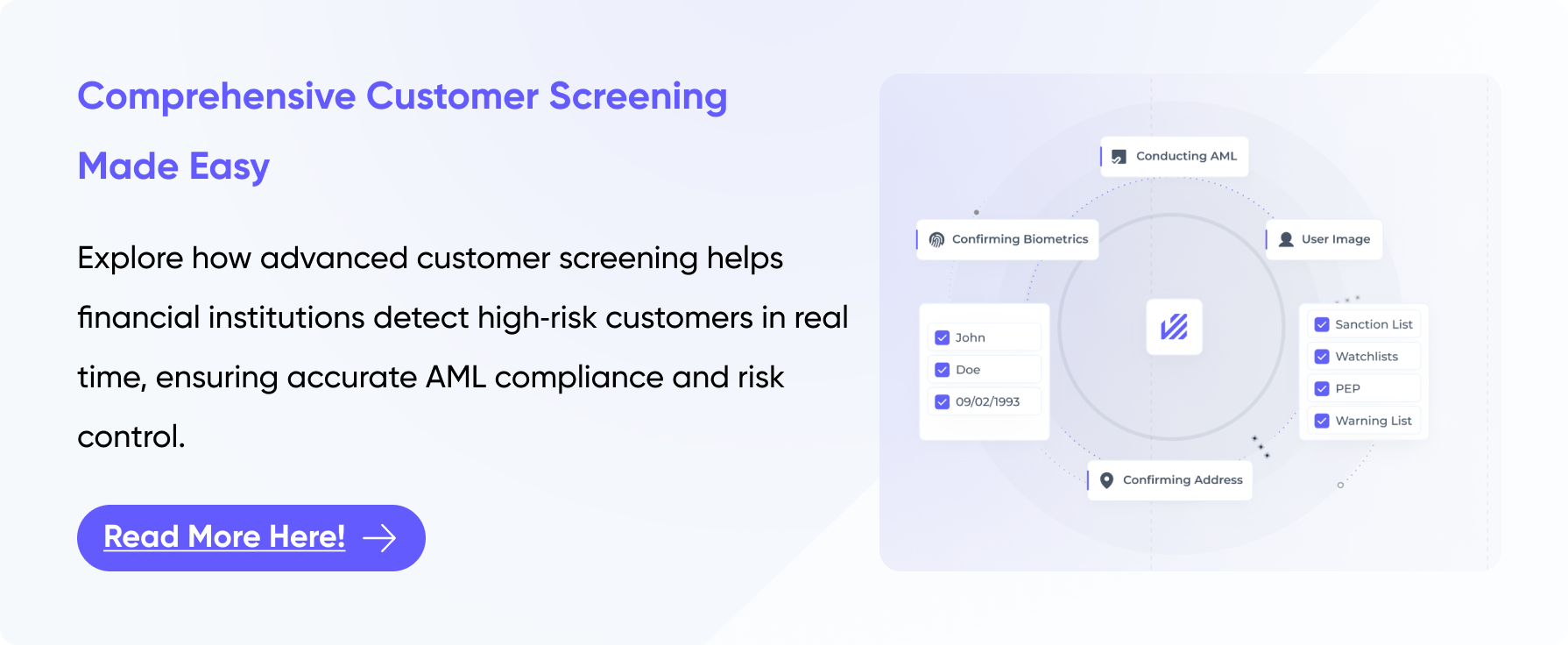

The Single Customer View (SCV) is a unified customer profile created by combining data from multiple internal and external sources. It connects customer identity details, products, accounts, transactions, and interactions into a single profile. This ensures that decisions made during onboarding, monitoring, investigations, and reporting are consistent. Clients interact with businesses across multiple channels online, in-store, via customer service, and mobile apps.

SCV consolidates the fragmented client data into a single, comprehensive profile that reveals past behaviors, preferences, and interactions. This consolidation helps in managing customer data, offering accurate insights that improve decision-making and compliance with AML regulations.

Significance of SCV in Anti-Money Laundering (AML)

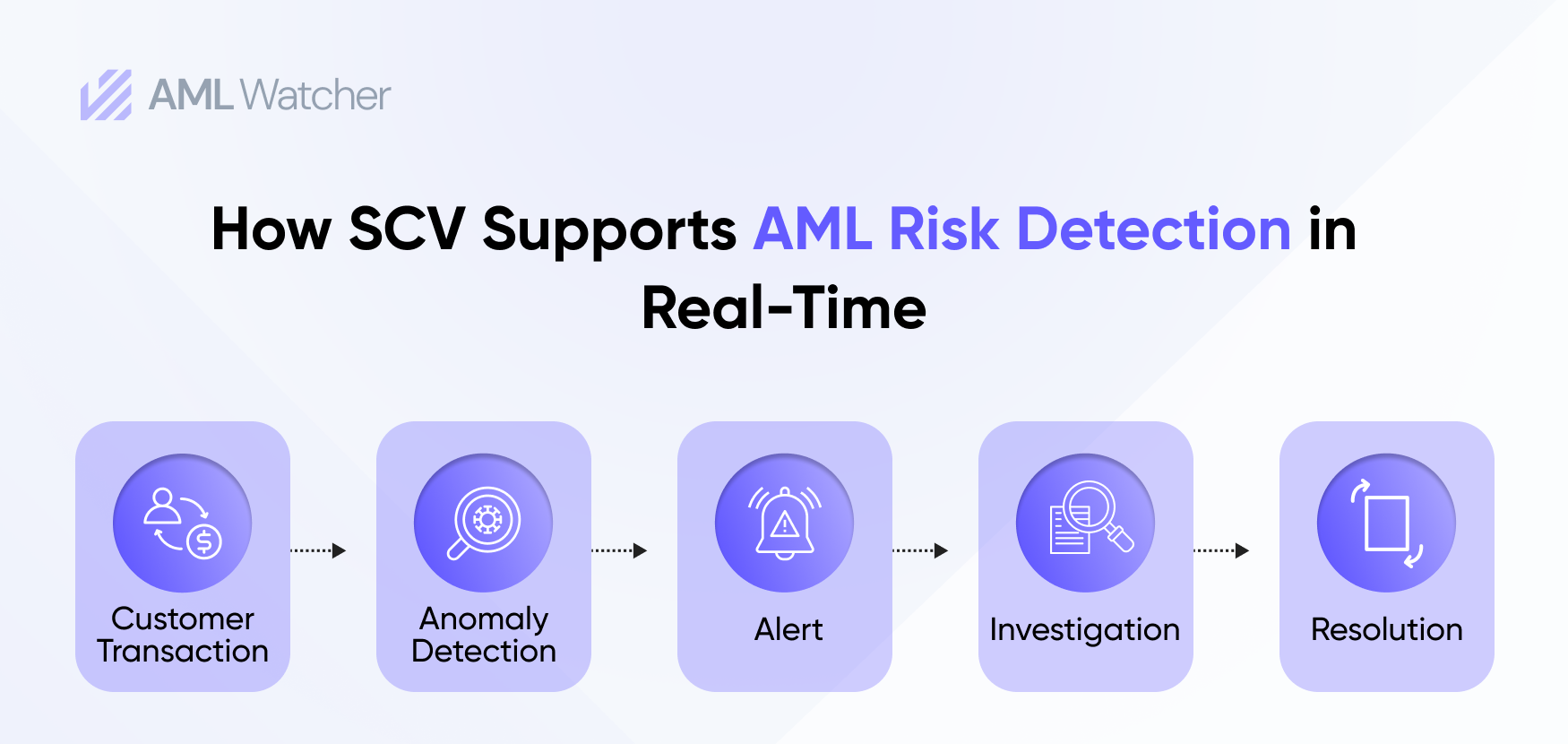

To companies, especially in the financial industry, a single customer view is important in compliance with AML regulations. Banks and other financial institutions need to check on their customers for suspicious activity to avoid money laundering and terrorist financing. SCV helps an MLRO justify why a customer’s risk rating changed because the history of alerts, screenings, and case outcomes is visible in one place.

Key Benefits of SCV in AML

- Holistic Monitoring: SCV enables financial institutions to detect suspicious activities more effectively due to fewer missed links between related accounts/entities.

- Enhanced Risk Management: With the full customer profile across products, financial institutions are able to effectively evaluate and address the risks.

- Efficient Compliance: Consolidated customer data helps in faster evidence gathering for audits and SAR/STR narratives.

How SCV Works

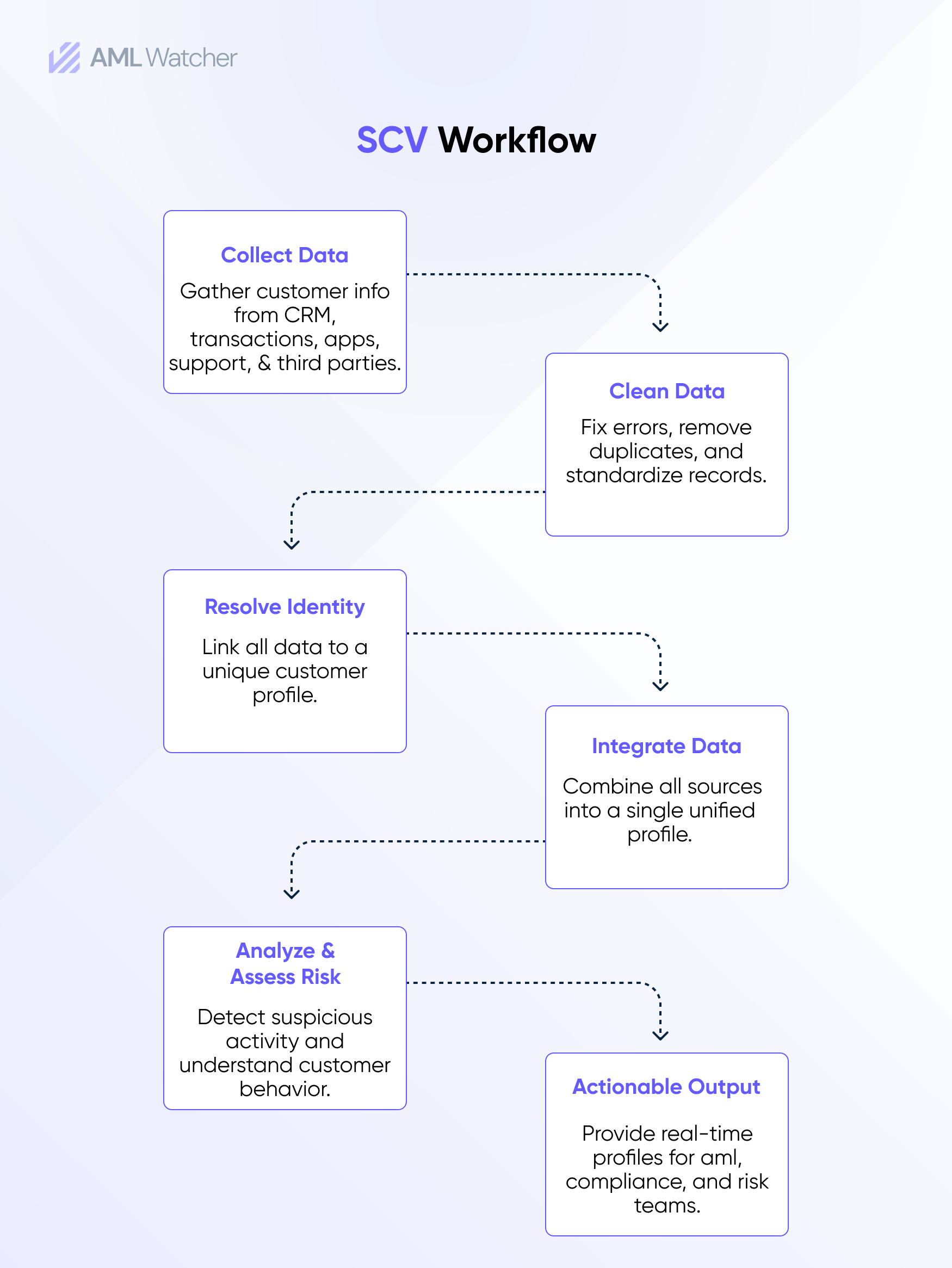

Single customer view is achieved by integrating customer data from multiple sources, such as Customer Relationship Management (CRM) systems, transaction records, and support logs. SCV integrates customer interactions, transaction history, behavioral data, and demographics into one comprehensive profile.

There are a number of drivers that contribute towards the formation of one perspective of customer information:

- Data Integration: Data from various sources (CRM systems, transaction records, customer support logs, advertising data, etc.) has to be integrated.

- Data Cleansing: It is necessary to get rid of duplicate data and ensure that all the data is right and consistent.

- Data Enrichment: Adding external third-party data to customer profiles to increase insights.

- Real-Time Data: It is important that the customer’s view is updated at all times.

Challenges in Implementing a Single Customer View

Although the advantages of SCV are obvious, the process of its realization is frequently characterized by difficulties. Some of the major hurdles include the complexity of integrating different sources of data, data quality, and privacy issues. Additionally, SCV needs a solid data governance system that will guarantee that data is used in an ethical and legal manner, as per such regulations such as GDPR or CCPA.

-

Data Silos

Data stored across various systems creates fragmented information. It becomes challenging to consolidate this data into a single view. This fragmentation limits insights and hinders informed business decisions.

-

Data Quality

There is always a challenge of ensuring that data is correct, consistent, and complete. Duplicate records, outdated information, and inconsistent data formats can undermine the reliability of the SCV. Poor data quality not only affects analytics and personalization efforts but also reduces trust in business intelligence outputs.

-

Privacy and Security Concerns

Data consolidation across the different touchpoints implies that sensitive information about customers must be secured. Breach of information or misuse of data might be very detrimental. This increases the risk of data breaches, unauthorized access, or misuse of information. Therefore, it requires companies to implement robust security controls and privacy safeguards to protect customer data and maintain regulatory compliance.

-

Scalability

As data volume grows, a single customer view might become more difficult to sustain. Maintaining an accurate and real-time single customer view at scale becomes increasingly difficult without flexible architectures and advanced data management capabilities.

Future of SCV in Customer Risk Management and AML

As customer data grows, financial services recognize SCV’s role in AML compliance, with AI and machine learning enabling real-time data management.

In addition, with the changes in regulations, an accurate and single customer profile will be even more significant in ensuring compliance and the prevention of enforcement action.

To sum it up, the use of a Single Customer View is non-negotiable; it needs to be implemented among businesses, particularly those related to the financial sphere. The advantages of a centralized customer profile, be it better risk management or less compliance, are unquestionable. Nevertheless, in achieving the potential of SCV, companies have to overcome the issues surrounding the integration, quality, and privacy of data.

With the ongoing change in the field of technology, SCV solutions are going to be more advanced, with greater insights given to the businesses in areas of customer behavior and upcoming risks. To financial institutions, the adoption of SCV is an important move towards the development of a stronger, compliant, and customer-focused business establishment.

How AML Watcher’s Solution Smoothly Integrates with Existing Systems

Fragmented customer data makes it harder to explain why a customer was rated high risk, why an alert was closed, or why a periodic review was delayed. When an SCV program is paired with reliable screening and ongoing monitoring, risk changes become easier to spot and document.

AML Watcher supports screening across sanctions, PEP, watchlists, and adverse media, with configurable risk scoring and monitoring workflows that help compliance teams act on changing risk signals.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries