Top FCA Fines in 2025 and Key Enforcement Findings

Others

November 28, 2025

Financial institutions in the UK are on high alert after record-breaking fines imposed by the Financial Conduct Authority (FCA). Tens of millions in penalties have been imposed on both global banks and challenger firms, after the regulator identified shortcomings in their compliance systems.

These enforcement actions raise critical questions for financial institutions: where did these firms go wrong, and which ones could be next under regulatory scrutiny? This blog breaks down the year’s biggest FCA fines, summarises the regulator’s key findings, and outlines the lessons compliance teams should consider to strengthen oversight.

Top 10 FCA Penalties in 2025

The FCA’s enforcement blitz in 2025 has already produced staggering penalties. Following is a list of the top 10 FCA fines imposed in 2025 so far:

-

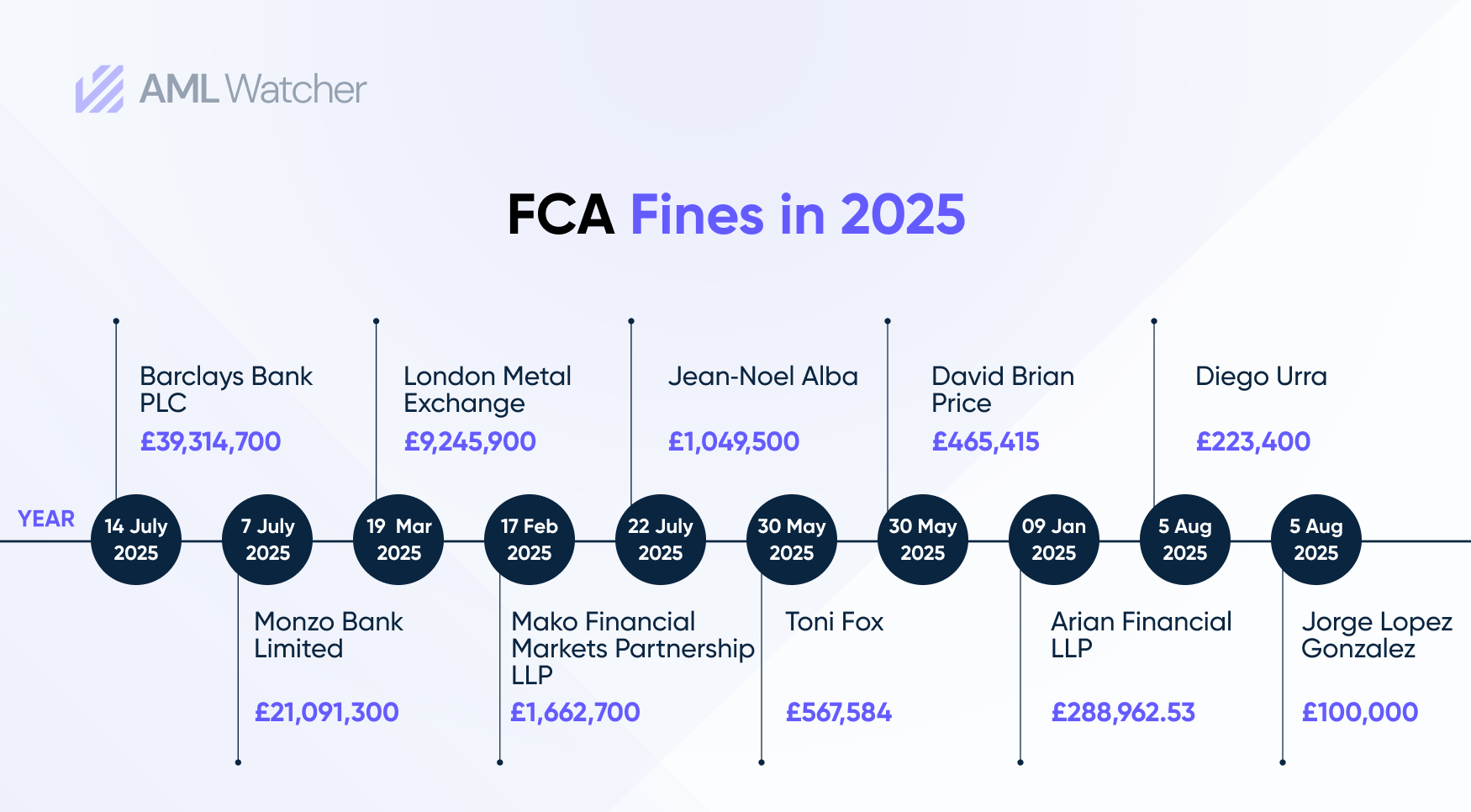

Barclays Bank PLC

According to the FCA, Barclays showed weakness in monitoring its high-risk corporate clients, despite the multiple red flags, including law enforcement activity. By doing so, they permitted £46.8 million in funds from a criminal operation to pass through. FCA fined Barclays a huge amount of £39.3 million for its negligence in risk assessment and monitoring.

-

Monzo Bank

Monzo didn’t check its clients and track transactions properly, As FCA cited in its report, “Its customer base has grown rapidly, increasing almost tenfold from around 600,000 in 2018 to over 5.8 million in 2022. However, Monzo’s financial crime controls failed to keep pace with its customer and product growth”.

For poor customer checks and ineffective transaction monitoring, they were fined £21.1 million.

-

London Metal Exchange (LME)

FCA fined LME for governance lapses and inadequate systems during the 2022 nickel market crisis. The weak systems and lack of senior oversight led to a penalty of £9.24 million.

-

Mako Financial Markets

FCA claim that Mako shows negligence in identifying red flags in anomalous trading worth £90 billion. For this, Mako had to pay £1.66 million for deficiencies in AML controls related to complex trading strategies.

-

Jean Noel Alba

The former H2O deputy CEO, Jean Noel Alba, misled the Financial Conduct Authority, as the FCA said, “During the FCA’s investigation into H2O, Mr Alba provided false and misleading statements and documentation to the regulator. Mr Alba was the principal point of contact with the FCA during its investigation”. For this FCA fined £1 million and banned him for severe integrity breaches.

-

Toni Fox

As per the FCA report, Toni Fox pushed people to shift their pension from a guaranteed benefit to a riskier system where the customers can even get more profit than their actual pension or nothing at all. That’s how she violated the standards of FCA. In response to this, FCA fined her with a penalty of £567K.

-

David Brian Price

David Brian was fined by the FCA because the Financial Conduct Authority found him supporting Toni Fox in running her riskier pension system without checking if it was right for the customers or not. He got a fine of £465K.

-

Arian Financial

FCA stated that Arian Financial was a UK-based financial firm that failed to spot red flags in risky cum-ex trades. The firm actually managed £52 billion in circular trades, allowing several clients to claim improper taxes. Because they missed major warning signs, FCA fined them £288K.

-

Diego Urra

Diego Urra used a large number of fake orders to trick the market and profit from smaller real trades. Because they violated the standards of FCA, as “the Act for engaging in behaviour that amounted to market manipulation which was prohibited by Article 15 of the Market Abuse Regulation 1 and before that was prohibited by section 118(5) of the Act” they got a fine of £223K from the Financial Conduct Authority.

-

Jorge Lopez Gonzalez

According to the FCA, Jorge Lopez Gonzalez was involved in market manipulation through spoofing at Mizuho (a Japanese financial group). Gonzalez, along with his colleagues, placed fake orders to gain smaller profits. FCA fined him £100K.

FCA Enforcement Trends 2025

In 2025, FCA enforcement highlighted a shift towards more effective and real-time investigations. Open investigations decreased from 188 to 130, while case closures increased compared with the previous year. Total fines rose from approximately £38 million to between £179 million and £186 million. Penalties imposed on individuals more than tripled during this period. The FCA also made greater use of interventions, authorisation revocations, and other supervisory powers.

The majority of cases concerned financial crime, deficiencies in AML controls, and governance failures. These trends are documented in the FCA’s 2024/25 Annual Report and enforcement data.

How FCA Penalties Are Triggered

Picture a bank observing a new company on its client list, when they skim through the FCA register, they found out that it’s quite risky; however, the bank ignored it. This small negligence will later become a headache for the banks because in the future, when they will get associated with them, they will have to face penalties by the FCA. This penalty would be in response to negligence that the bank did intentionally.

Another scenario can be if a bank notices weird money trails but did not submit a SAR or did not finish their work with that specific company, and waits for the regulators to tell them about the issue. They will get a fine from the FCA for not acting promptly.

How Financial Institutions Can Avoid Costly Penalties

The above-mentioned high-profile FCA fine cases highlight that the significance of ongoing compliance is not a one-time task; it is an ongoing process. FIs must be vigilant in this case; they should follow the following practices:

The key defences for penalties that have become industry standard now are:

- Comprehensive transaction monitoring: FIs need to install automated transaction monitoring systems to spot unusual transfers and frequent new accounts. This will help them report suspicious behaviour proactively.

- Robust customer screening: Perform frequent customer checks against sanctions, PEP lists, and adverse media. Such practices will reduce the risk of being in a business relationship with criminals and money launderers.

- Regular risk reviews and audits: Firms should frequently stress-test their AML controls (as one AML Watcher audit guide notes) to find gaps. This includes revisiting risk assessments and ensuring AML policies keep pace with new products or regions.

- Clear accountability and records: The FCA stresses detailed audit trails. Senior managers must be able to demonstrate oversight and decision rationale. Case management tools that log every review and escalation make this much easier and are increasingly expected by supervisors.

By following the best practices mentioned above, financial institutions can address the money laundering challenges effectively instead of just reacting to them. The contemporary systems offer compliance systems that are a combination of screening, monitoring, and case management, enabling them to keep up in the highly competitive environment.

Strengthen Compliance and Minimize Costs with AML Watcher

Many financial institutions face a common challenge where the majority of compliance workforce time is consumed in reviewing false positives.

AML Watcher’s solutions are built to be adaptable to the unique needs of every business, eliminating the majority of the noise in screening upfront that comes with rigid solutions.

Its advanced AI compliance feature, combined with proprietary data, separates false positives from true matches with a clearly explained decision process, solving the alert fatigue problem for compliance teams.

This frees valuable analyst time for high-priority tasks and an informed decision-making process, turning compliance from a vulnerability into a business advantage.

With regulators moving to stricter supervision, notice how FCA fines and strategies emphasize forward-looking controls with AML Watcher. With us, the top firms can now adopt the following solutions:

- Real-time screening of names and transactions.

- Automated alerts for policy breaches and clear audit dashboards.

- 15-minute data refresh for PEP, adverse media, and watch lists.

The FCA’s 2025 enforcement shows the cost of inaction. Investing in AML Watcher’s advanced technology turns compliance into a strategic asset: it helps detect issues early and demonstrates to auditors that you meet FCA expectations.

Move Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries