Understanding APG’s Role in Advancing AML/CFT Standards in Asia Pacific Region

AML/CFT

January 6, 2026

- FATF-Style Regional Bodies (FSRBs) and their Role in AML Compliance

- What exactly is the Asia Pacific Group on Money Laundering?

- High-Risk and other Monitored Jurisdictions in the Asia-Pacific Region

- What are Mutual Evaluation Programs

- How APG’s Mutual Evaluation System Works

- What Mutual Evaluations Means for Financial Institutions

As unfortunate as it is, what still remains true is the fact that financial crime does not respect borders and neither can the systems designed to stop it.

With the globalization of finance, financial crime has also become globalized. Money laundering schemes evolved rapidly, exploitation of regulatory gaps between jurisdictions became a norm, thus, forcing regulators to recalibrate their approach towards AML compliance.

As a result of which, international cooperative bodies emerged to align standards, coordinate oversight, and strengthen cross-border defenses against illicit finances, giving a new shape to AML compliance as a globally acknowledged obligation.

The creation of the Asia Pacific Group on Money Laundering is a result of one such collaborative effort that helped countries in the region to work together in order to overcome money-laundering as a vice.

FATF-Style Regional Bodies (FSRBs) and their Role in AML Compliance

FATF-style regional bodies are regional inter-governmental organizations that are modeled on the FATF. Their primary role is to promote and facilitate the implementation of FATF’s 40 recommendations within their respective regions.

There are a total of nine FATF-style regional bodies that are established for propagating international standards for battling money laundering, financing of terrorism and proliferation.

The FSRBs conduct evaluation of the AML systems of all the member states and make relevant recommendations for improvement. FSRBs conduct mutual evaluations of member countries’ AML frameworks to assess compliance and effectiveness, identify gaps and recommend improvements. They operate as the associate members of the FATF’s global network which includes FATF and nine regional bodies that cover most of the world.

What exactly is the Asia Pacific Group on Money Laundering?

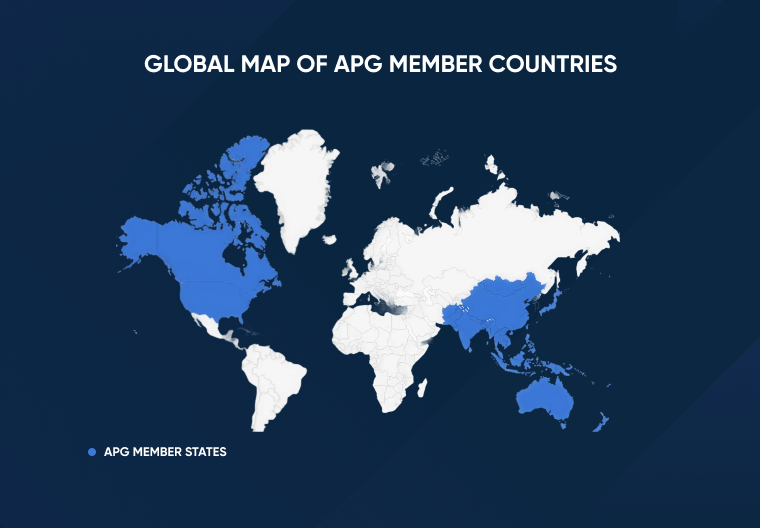

In 1993, FATF established its Asia Secretariat in the Asia Pacific, positioning it as a central hub for AML compliance in the region. Through this platform “Asia Money Laundering Symposia” held a series of meetings between 1993 to 1997 in Singapore, Malaysia, Japan and Thailand helping these countries to work united to counter money-laundering. At the last meeting the permanent foundation of APG was laid.

The current APG secretariat is in Sydney, Australia and the office is mainly funded by APG members.

High-Risk and other Monitored Jurisdictions in the Asia-Pacific Region

In the context of AML compliance high-risk countries are those flagged by global standard-setting bodies for weaknesses in their regulatory controls, enforcement mechanisms, or transparency standards.

While the Asia-Pacific Group for Money Laundering does not have its own list of “high-risk” countries, it aligns with the FATF issued lists which is the global AML standard setter. The FATF classifies jurisdictions with weak AML controls in black and grey lists. Iran, North Korea and Myanmar are in the black list because they have strategic deficiencies in their AML regimes. FATF members are urged to apply specific countermeasures against Iran and North Korea whereas enhanced due diligence in the case of Myanmar.

While the grey list consists of countries which are actively working with FATF to address weaknesses in their AML/CFT systems. Financial Institutions should assess their risk case by case basis and apply proportionate measures when dealing in those jurisdictions listed as grey list.

APG member states use FATF’s high-risk and increased monitoring lists as part of their national AML risk assessments and compliance frameworks.

What are Mutual Evaluation Programs

According to FATF a mutual evaluation report (MER) is an assessment of a country’s measure to combat money-laundering, financing of terrorism and proliferation of weapons of mass destruction. The report does not question or confirm why an entity was designated as a terrorist organization.

During a mutual evaluation the onus of responsibility is on the shoulders of the country being assessed. It must demonstrate that it has an effective framework to protect its financial system from abuse.

Mutual evaluations have two main components namely:

- Effectiveness

- Technical Compliance

The most critical element of a mutual evaluation is a country’s effectiveness rating. These ratings go beyond laws on paper and deciphers whether a country’s AML framework actually works in practice.

This is why effectiveness becomes the central focus during on-site visits where a team of experts work directly with the assessed country. Expectations are not one-size-fits-all, this is because what assessors look for varies based on the specific money-laundering, terrorist financing and other financial crime risks a country faces.

How APG’s Mutual Evaluation System Works

The Asia-Pacific Group on money-laundering (APG) plays a central role in improving AML/CFT systems across the Asia-Pacific region through its mutual evaluation program. Upon membership all APG members are bound to commit to a mutual peer review system in order to determine their levels of compliance with international AML/CFT standards.

There is a desk-based review of the member’s AML/CFT system as well as an onsite visit to the APG member by a team of experts of other APG members and the APG Secretariat, the team includes legal experts, financial and regulatory experts and law enforcement experts.

Once a mutual evaluation is completed, it identifies deficiencies and then further provides tailored recommendations on how a jurisdiction can strengthen its AML framework; these recommendations help countries prioritize reforms. Thus, continued oversight fosters sustained improvements and accountability.

What Mutual Evaluations Means for Financial Institutions

Through these evaluations and follow-up mechanisms the APG’s mutual evaluation program not only benchmarks compliance against global standards but also drives how AML/CFT works on ground, ultimately strengthening national and regional defenses.

Mutual Evaluation Reports directly have an impact on financial institutions because it enables them to prepare for any expected legislation or new regulations, as a result of identified gaps or recommendations included in the report.

FIs, banks and other AML regulated sectors should review their policies and controls in response to the gaps or risks identified in the MERs.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries