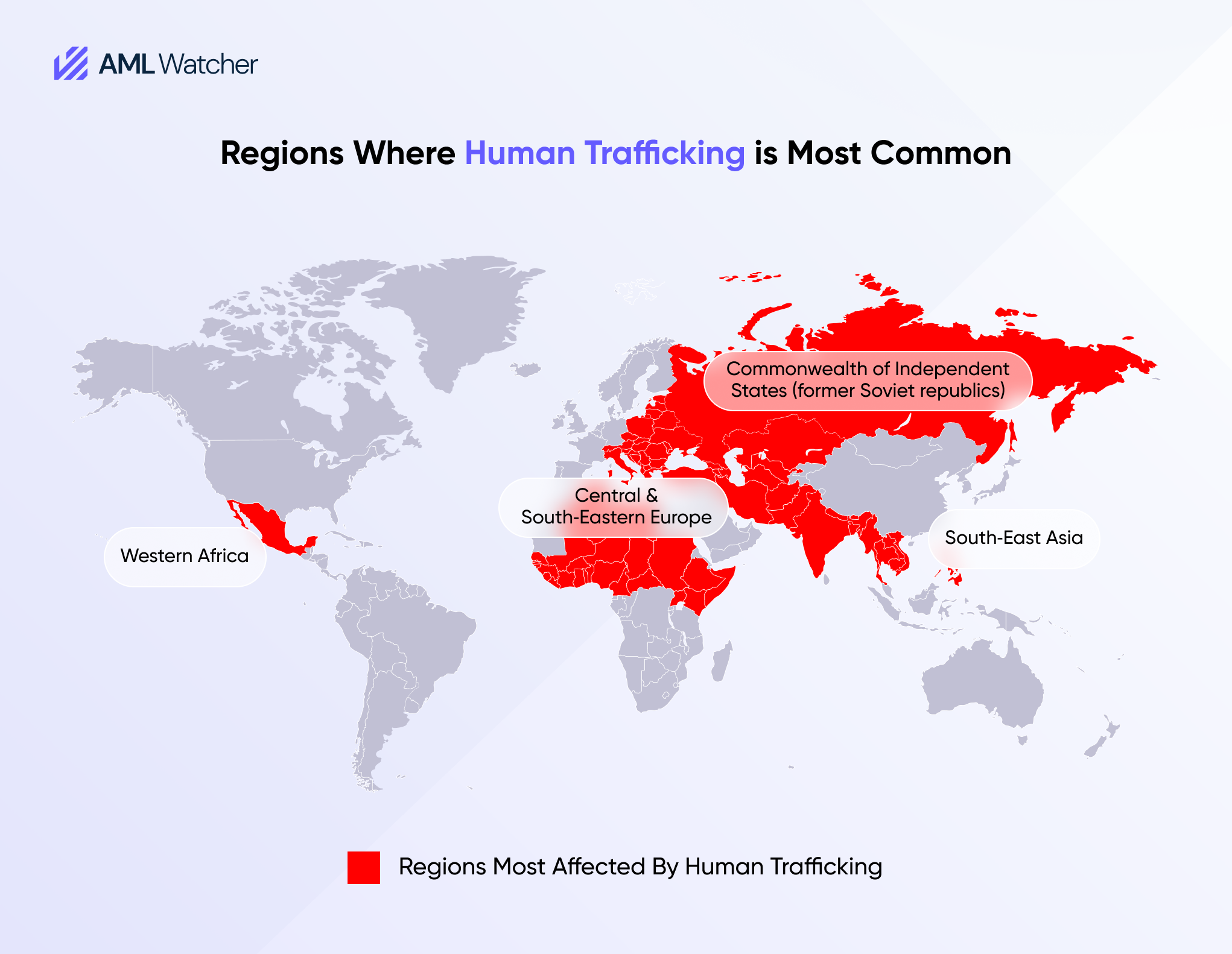

Why Banks Keep Missing Trafficking Proceeds in Their Data

Financial institutions often treat human trafficking as a distant criminal issue rather than a measurable financial risk. Yet regulators increasingly make clear that trafficking proceeds are already visible within everyday banking activity. The gap is not data availability, but how transaction behaviour is interpreted, connected, and escalated into meaningful SARs. Supervisors now expect banks to turn these data patterns into coherent SARs, not just flag individual transactions.

According to the Financial Action Task Force (FATF), 2011 report Trafficking in Human Beings and Smuggling of Migrants, found that Human trafficking and modern slavery are among the most profitable forms of organised crime, generating illicit profits that must be disguised before entering the legitimate economy. Under various anti-money laundering laws, these crimes are considered predicate offences for money laundering, as they generate proceeds that may subsequently be laundered through the financial system.

The same FATF report revealed that money made from human trafficking often ends up moving through normal banks and financial systems, which is why banks are expected to watch for and report it. FATF identified human trafficking proceeds as a major risk for banks and financial institutions when handled through their systems. Banks and financial institutions must take AML measures to address these proceeds of crime.

Trafficking of humans and slavery are considered serious criminal offenses under the UK’s Modern Slavery Act 2015, where the most severe cases lead to imprisonment. Anti-money laundering authorities make the action illegal regardless of the result or the individual’s purpose. The Proceeds of Crime Act focuses on how authorities can track this money, seize it, and take legal action against anyone trying to hide or launder it.

These laws define the offence, but compliance effectiveness depends on how institutions interpret transaction behaviour in practice, not on legal definitions alone. Even with robust legal frameworks, detection gaps persist because institutions often fail to correlate transactional data across accounts, networks, and geographies, resulting in failures to detect transactions associated with predicate offences, including human trafficking.

How to Exactly Monitor and Identify Proceeds of Crime Related to Human Trafficking

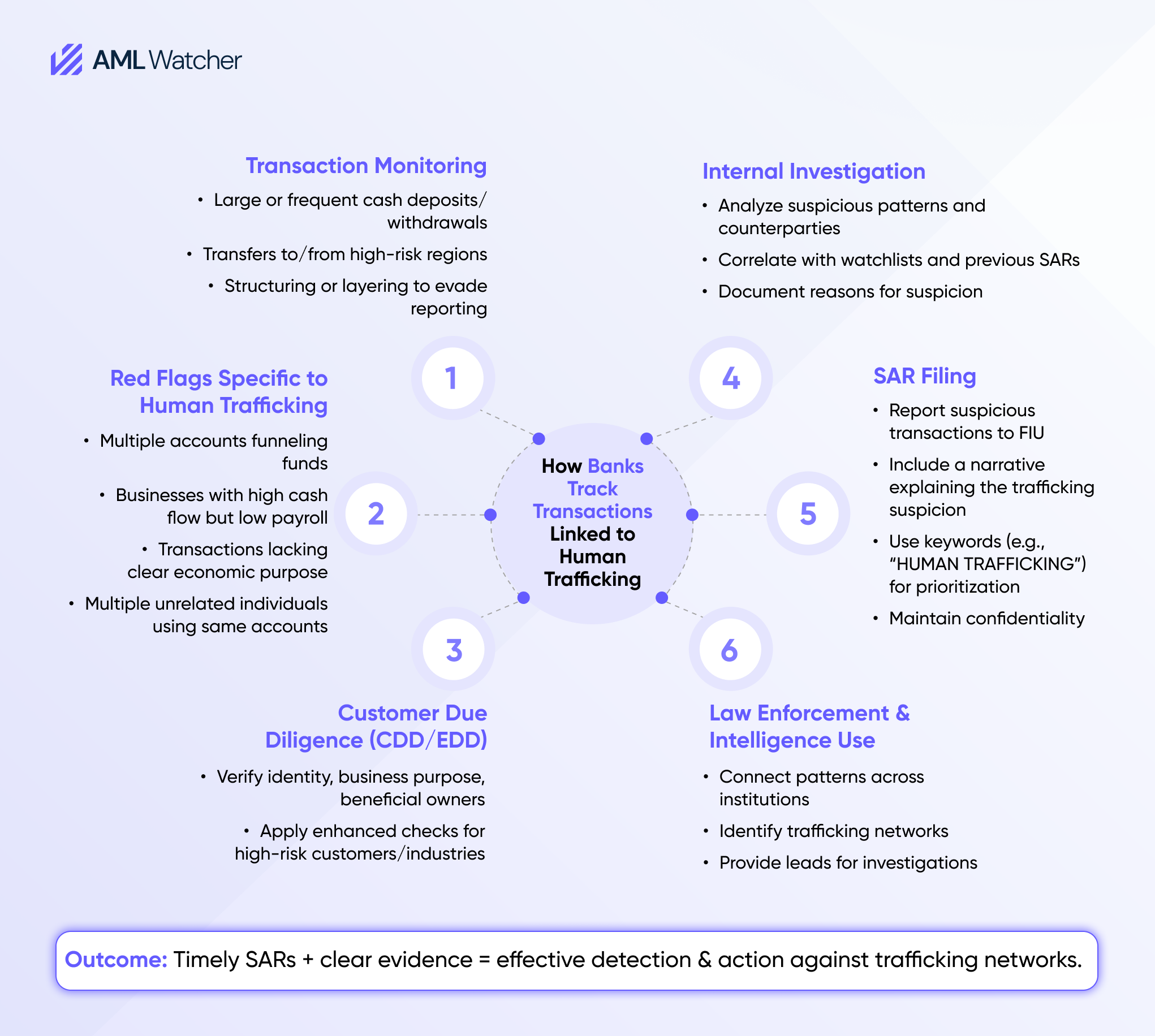

Identifying trafficking-related proceeds through SARs is complex, as the underlying transactions are often fragmented, obscured, and embedded within ordinary banking activity. In practice, trafficking proceeds rarely appear in a single suspicious transaction. Instead, patterns emerge over time, and financial institutions must connect multiple data points across customers, products, and geographies.

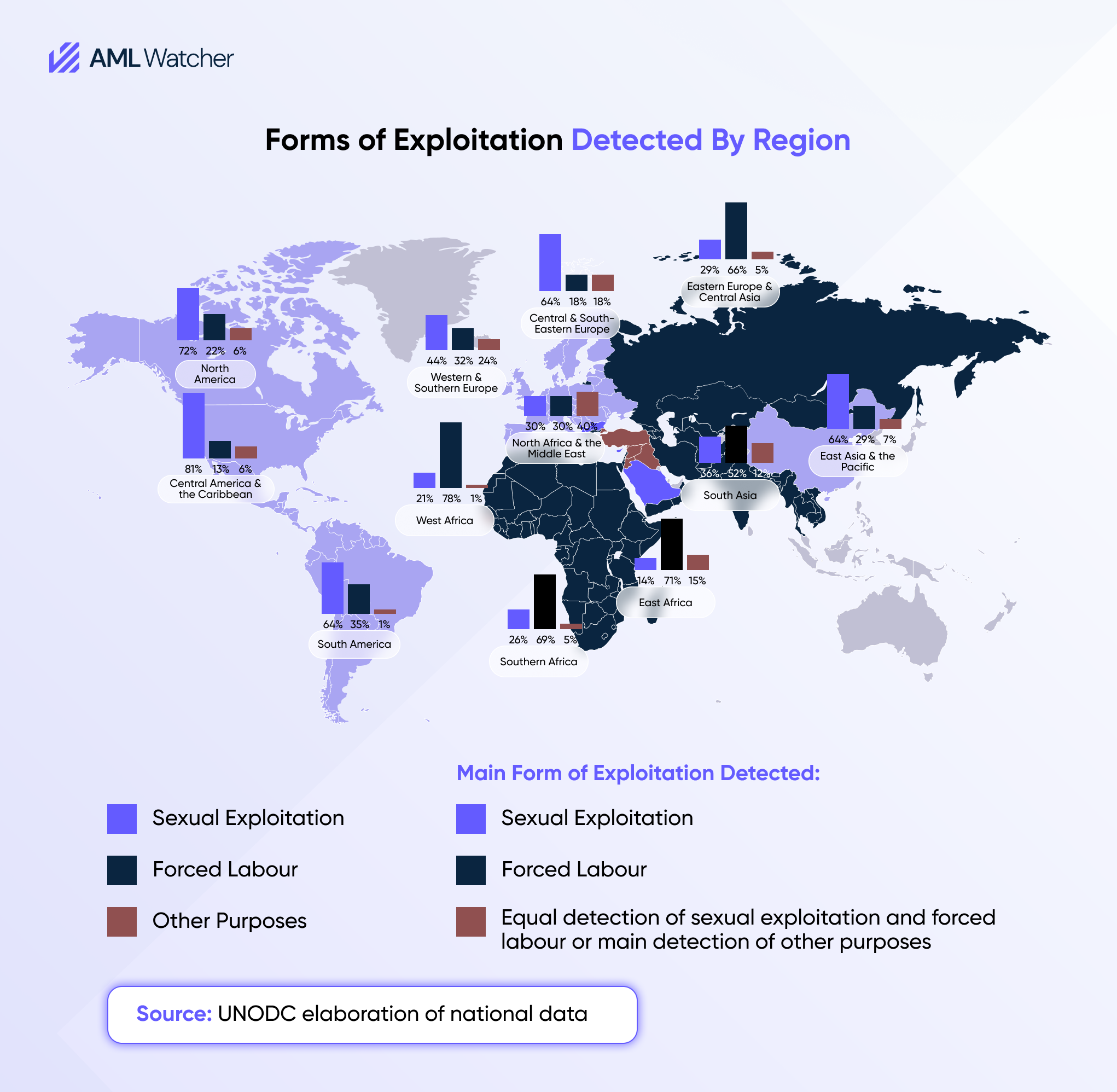

Financial Intelligence Units from the jurisdictions with a high risk of crimes like Human Trafficking often issue tailored guidance to analyze the proceeds of crime. In May 2024, the Financial Intelligence Unit of Malta published a typology report that provides detailed indicators that can help financial institutions detect potential human trafficking (HT) and modern slavery (MS) financial activity. These indicators cover customer behaviour, geographical patterns, and product or transaction types:

1. Labour Exploitation Indicators

Customer HT/MS Risk

- Properties housing more inhabitants than expected.

- Customers with poor personal hygiene or signs of physical abuse.

- Accounts showing minimal everyday expenses relative to expected behaviour.

- Absence of legitimate employment or contracts below minimum wage.

- Employers reported for cheap labour or unfair practices.

Product/Service & Transaction Risk

- ATM usage suggests third-party control of cards.

- Third-party payment of visas or employment contracts.

- Recurrent transfers indicative of debt bondage.

- Payroll inconsistencies and suspicious wage payments.

2. Sexual Exploitation Indicators

Customer HT/MS Risk

- Links to escort, model, or entertainment agencies.

- Multiple joint account holders or authorised users who are unrelated.

- Third-party involvement in transactions, including handling ID.

- Use of aliases, false documents, or shared contact information across accounts.

Geographical Risk

- Transactions to jurisdictions with high sexual exploitation risk.

- Activity linked to nightclub districts or known adult industry hubs.

Product/Service & Transaction Risk

- Third-party cash deposits and withdrawals in different locations.

- Prepaid card usage, hotel bookings covering multiple rooms, and frequent small-value transfers.

- Payments for massage parlours, beauty salons, or adult services outside normal hours.

3. Human Trafficking Indicators (All Forms)

Customer HT/MS Risk

- Multiple accounts using shared contact or employment information.

- Frequent logistics, transportation, or travel expenses inconsistent with the customer profile.

- Avoidance of face-to-face contact, frequent changes of contact info, or signs of distress.

- Third-party account control, use of forged documents, or accounts in children’s names.

Geographical Risk

- Transfers along known trafficking routes or to high-risk jurisdictions.

- Frequent activity from different locations.

Product/Service & Transaction Risk

- High transaction volume at transport hubs or for essentials, inconsistent with declared activity.

- Recurrent lump-sum withdrawals, salary withdrawals in cash, or funnelling via third-party accounts.

- Use of money remittance services, prepaid cards, and alternative payment methods to obscure funds.

4. Human Smuggling Indicators

While human smuggling is distinct from human trafficking, these activities can overlap, and similar financial red flags may indicate HT/MS risks.

Customer HT/MS Risk

- Lifestyle inconsistent with declared employment or business activity; profits or deposits significantly higher than peers.

- Accounts closed due to suspicious activity.

- New customers replicating transactional patterns of previously closed accounts, including frequent cash-intensive transactions involving the same counterparties.

- Frequent exchanges of small-denomination bills for larger ones by customers not operating cash-intensive businesses.

Geographical HT/MS Risk

- Accounts operating as funnel accounts, with cash deposits below reporting thresholds in locations unrelated to the customer’s residence or business.

Product, Service & Transaction HT/MS Risk

- Wire transfers received from countries with high migrant populations where recipients are not nationals.

- Cash payments or receipts disproportionate to the customer’s line of business, including cash used to purchase assets.

- Cheques deposited from potential funnel accounts appear pre-signed with different handwriting.

- Multiple unrelated customers sending wire transfers to the same recipient.

- Other similarities in transactions, such as common addresses, contact numbers, or amounts, indicate potential coordination.

How to Use These Indicators

No single indicator is conclusive. Banks should look for clusters of red flags across customer behaviour, geographical risk, and transaction types. Automated transaction monitoring, combined with standardised customer due diligence, can help institutions detect these patterns and generate higher-quality SARs that support law enforcement investigations.

By implementing these typology-based monitoring practices, financial institutions can transform fragmented transactional data into actionable insights, detecting the proceeds of human trafficking, modern slavery, and human smuggling more effectively.

How AML Laws Across the Globe Address the Proceeds of Human Trafficking

Across jurisdictions, AML regimes have been deployed to investigate trafficking-related financial crime:

- The Financial Crimes Enforcement Network (FinCEN) in the United States issues targeted advisories to financial institutions, highlighting patterns of transactions that may indicate human trafficking. Under these advisories, banks are expected to file Suspicious Activity Reports (SARs) using the recommended narrative term “ADVISORY HUMAN TRAFFICKING”, ensuring consistency and clarity for law enforcement. Financial institutions must monitor for indicators such as structuring of transactions, unusual fund flows, and activity inconsistent with customer profiles. SARs should be filed promptly and include sufficient detail to enable authorities to investigate potential trafficking-linked proceeds effectively. Compliance with these reporting requirements helps institutions demonstrate due diligence and supports law enforcement in disrupting trafficking networks.

- In Pakistan, the Federal Investigation Agency (FIA) and Anti-Human Trafficking and Smuggling Wing are increasingly leveraging AML law to seize assets and pursue trafficking suspects as part of broader financial crimes investigations. Under Pakistan’s Anti‑Money Laundering Act, 2010 (as amended), proceeds of predicate offences, including trafficking‑linked funds, can be investigated, frozen, and forfeited, and authorities such as the Federal Investigation Agency and Anti‑Human Trafficking and Smuggling Wing increasingly leverage these provisions in broader financial crime investigations.

- Bahamas Regulatory Authorities (FIU Bahamas) require robust AML/CFT frameworks and are part of the global Egmont Group network, which mandates effective transaction monitoring and AML reporting from regulated entities.

- AUSTRAC (Australia): Publishes guidance for detecting suspicious transactions linked to human trafficking and modern slavery, including cross-border flows and structuring activity.

- FIU Netherlands: Emphasizes correlating transactional behaviour across accounts and networks to identify laundering linked to trafficking.

Reporting Gaps in Trafficking‑Linked Suspicious Activity Reports

Financial institutions face serious consequences when they fail to detect and report suspicious transactions tied to trafficking or slavery proceeds. Enforcement actions increasingly demonstrate that regulators assess not only whether SARs were filed, but whether they meaningfully explained the suspected predicate offence behind the transactions.

One prominent example is TD Bank in the United States: regulators found extensive failures by the institution to timely file SARs on substantial criminal activity, including transactions clearly linked to organised crime and trafficking proceeds. The bank was required to review historical transaction data, overhaul controls, and implement comprehensive AML program enhancements under regulatory supervision.

While not trafficking-specific in the headline, this type of enforcement illustrates that failure to report suspicious activity, including trafficking-related patterns, leads to regulatory action. Financial institutions are under increasing scrutiny to accurately detect, escalate, and report signs of predicate offence proceeds under AML regimes.

How Transaction Monitoring Tools Detect Trafficking-Linked Activity

Modern transaction monitoring systems are a frontline defence for identifying flows consistent with trafficking proceeds. Effective solutions:

- Profile expected behavior and flag deviations (e.g., sudden high-volume movements, unusual business patterns)

- Use network analysis to uncover links between accounts with shared identifiers or behavioural similarities

- Integrate geographic risk scoring to prioritise transactions involving high-risk corridors or known exploitation hubs

- Correlate with external intelligence such as adverse media, law enforcement alerts, and FATF typologies

- Provide alerts that feed into escalating thresholds for SAR review and filing

In practice, modern AML transaction monitoring systems go far beyond simple rule‑based flags. Leading solutions use machine learning, behavioral analytics, and customer risk profiling to detect complex patterns and hidden relationships that traditional monitoring might miss.

These systems establish a baseline of normal activity for each customer and then use real‑time analysis to flag deviations from expected behavior, such as unusual transaction volume, velocity, or cross‑border flows that deviate from customer profiles. They also incorporate entity relationship mapping to uncover linked accounts and intermediaries, providing compliance teams with visual network insights and prioritized alerts for deeper investigation. This capability significantly improves accuracy, reduces false positives, and strengthens SAR reporting workflows.

Practical Takeaways for Financial Institutions

Red Flags to Incorporate into Monitoring:

- Patterns of structuring and funneling that deviate from normal economic activity

- High volume remittances involving accounts with linked identifiers

- Frequent cross-border flows with no apparent economic purpose

- Transactions tied to shell companies or obscure merchant services

Consequences of Inadequate Transaction Monitoring

Institutions that lack transaction monitoring solutions capable of detecting alerts linked to predicate offences face both operational and regulatory risks. Ineffective monitoring often results in higher false positives, increasing investigation costs, and diverting resources to low-risk alerts. More critically, it can cause delays or gaps in SAR filings, leaving institutions exposed to enforcement actions, reputational damage, and financial penalties. Ensuring monitoring systems can detect complex trafficking-related patterns is therefore essential to maintain compliance effectiveness and support law enforcement efforts.

Compliance Imperatives:

- Build transaction monitoring rules tailored to predicate offences like trafficking

- Leverage external data sources (FATF, FinCEN, national FIUs) for red flag intel

- Document and escalate suspicious findings promptly to reduce enforcement risk

Cut Manual Reviews and Detect Crime with AML Watcher

As regulatory expectations rise, financial institutions face growing challenges: detecting complex crime typologies, including human trafficking, often requires intensive manual reviews. Without tools that incorporate logic for typology detection and contextual insight, compliance teams can struggle to identify the most relevant suspicious transactions, wasting time and increasing operational risk.

AML Watcher directly addresses these pain points:

- Reduce Manual Review Burden: Our in-house research teams continuously identify human trafficking–related signals and calibrate rules enriched with diverse data, helping compliance teams spend significantly less time reviewing low-value alerts.

- Improve Detection Accuracy: Tailored rules and contextual analytics help identify proceeds of crime aligned with regulatory typologies, supporting more precise and defensible SAR filing.

- Gain Contextual Insight: Cross-referencing global risk signals and adverse media provides a fuller picture of potentially suspicious activity, enabling informed decision-making.

- Stay Aligned with Regulatory Expectations: Rules and monitoring scenarios are designed to meet regulator-mandated requirements, helping institutions demonstrate compliance while proactively addressing high-risk flows.

By combining logic-driven monitoring with enriched contextual intelligence, AML Watcher empowers institutions to detect illicit activity more effectively, reduce unnecessary review effort, and improve the quality of suspicious activity reporting.