FinCEN’s Role in Combating Money Laundering

Anti Money Laundering

March 5, 2025

- What is FinCEN?

- Compliance vs Profits: The Central Clash

- The Case for FinCEN Regulations: A Necessary Shield Against Money Laundering

- The Other Side of FinCEN: A Bureaucratic Burden on Businesses

- FinCEN’s Strict Rules: Weighing Down Businesses Financially

- FinCEN’s Expectations from Businesses- Can Businesses Keep Up?

- Finding the Balance: What Should Businesses Do?

- How AML Watcher Assists Organizations in Maintaining FinCEN Compliance

FinCEN has imposed a fine of $900,000 on Lake Elsinore Hotel and Casino in California, for failure to comply with the Bank Secrecy Act for more than four and a half years.

Over these years, the bank failed to implement an effective AML program and neglected to file the required suspicious activity reports. This not only exposed both its patrons but also the US financial system to significant risks.

This case highlights FinCEN’s role in combating money laundering and safeguarding financial integrity.

FinCEN holds institutions accountable, not only to enforce AML compliance but also to deter potential misconduct across the financial sector.

Here are the three primary missions of FinCEN:

- It receives and maintains financial transaction data and receives reports like SARs and CTRs from financial institutions.

- It analyzes and disseminates that data for financial crime law enforcement purposes

- Collaborates with domestic and international partners and works with agencies worldwide to strengthen AML/CFT enforcement.

FinCEN enforces AML regulations to ensure financial institutions identify and prevent financial crimes. However, compliance may be complicated, requiring organizations to handle enormous volumes of data and provide thorough reports.

Many organizations have operating difficulties due to legacy or ineffective compliance systems. Institutions can more successfully comply with FinCEN’s standards by updating their AML technology.

In this blog, we discuss FinCEN’s role in combating money laundering and how businesses can use sophisticated AML software to comply with advanced and changing FinCEN regulations.

What is FinCEN?

FinCEN stands for Financial Crimes Enforcement Network (FinCEN). It is a bureau of the U.S. Department of the Treasury responsible for combating money laundering and terrorist financing and ensuring financial crime intelligence.

It collects and analyzes financial data to detect illicit activities and enforces AML regulations.

FinCEN also collaborates with financial institutions, law enforcement agencies, and international bodies to strengthen financial security and transparency.

Compliance vs Profits: The Central Clash

For many financial institutions, FinCEN’s regulations present a challenging paradox. They are indispensable for combating illicit activity, but they can also lead to cumbersome bureaucratic hurdles.

Take the example of a mid-sized bank that was recently flagged for failing to meet FinCEN’s strict filing deadlines for Suspicious Activity Reports (SARs).

The penalties imposed were severe, but what went unnoticed was the bank’s struggle to process thousands of flagged transactions. Many of these turned out to be false positives.

In this case, the bank had a small compliance team that was overwhelmed by the sheer volume of data and reports generated by its monitoring software. As a result, it faced

- Multiple delays in onboarding new clients

- Compliance gaps that led to fines and penalties

- Reputational damage and loss of customer trust

This highlights the need for businesses to take a proactive approach. While FinCEN’s oversight can seem like a bureaucratic maze, businesses that adapt smartly can navigate it effectively.

They can easily turn compliance into a competitive advantage rather than a burden.

The Case for FinCEN Regulations: A Necessary Shield Against Money Laundering

FinCEN regulations are the cornerstone of the US Financial system, but why is it needed?

The US, with its strong laws and ethical business practices, still struggles with non-compliance. So what’s FinCEN doing exactly?

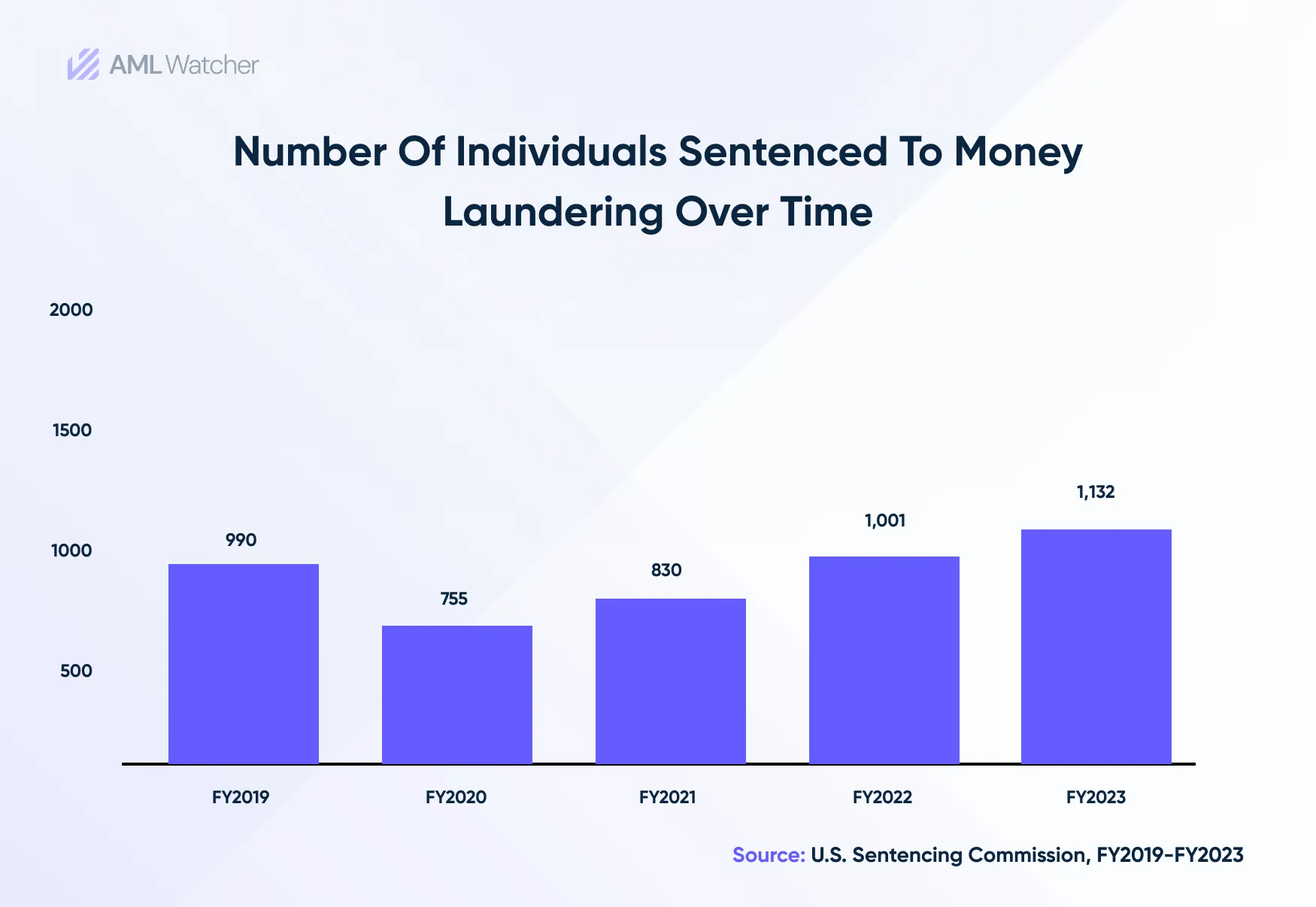

Within the US, drug trafficking makes up around 35% of crimes, followed by financial fraud, which makes up 25% of all crimes.

Additionally, of the 64124 cases that were reported to the United States Sentencing Commission, around 1132 were involved in money laundering. This paints a scary picture of financial crime within the US.

FinCEN enforces the Bank Secrecy Act to combat financial crimes. Think of FinCEN as the lifeguard at a massive financial beach. Now, think of the Bank Secrecy Act as the watchdog and binoculars.

The BSA helps spot dangerous rip currents, suspicious transactions, and money laundering. FinCEN dives in to investigate and pull bad actors out of the water before they drag the economy under.

What is BSA exactly?

The BSA requires financial institutions to maintain records, report suspicious activities, and implement Anti Money Laundering (AML) programs.

FinCEN analyzes these reports to detect illicit financial activities, helping law enforcement track and prevent fraud.

Additionally, businesses are required to file beneficial ownership information with FinCEN to highlight all the individuals who ultimately control the assets and profits of the company.

However, according to the Notice Regarding National Small Business United v. Yellen, No. 5:22-cv-01448 (N.D. Ala.) updated January 2, 2025, companies are no longer required to file BOI, yet many companies are choosing to do so voluntarily.

The Other Side of FinCEN: A Bureaucratic Burden on Businesses

According to the Financial Crime Academy, large banks spend around $1 billion dollars per year to ensure AML compliance with regulatory standards.

Additionally, globally, financial institutions spend more than $100 billion on compliance. However, this causes smaller firms to be affected disproportionately.

Whether a company is small or large, AML compliance is necessary. With FinCEN’s tough regulations, businesses often find it hard to mitigate financial crime.

Think of a Florida-based community bank that only has 8 billion dollars in assets. The company faces significant regulatory burdens because of its reliance on manual compliance processes.

Unlike bigger banks, this Florida bank is unable to keep up with all the requirements of FinCEN.

Additionally, it is worth noting that because FinCEN regulations are quite tough and expect a lot from businesses, many times businesses find it hard to comply.

This results in legitimate businesses and entities getting de-risked, leading to a loss of significant revenue.

FinCEN’s Strict Rules: Weighing Down Businesses Financially

Strict FinCEN rules can push banks to exit high-risk markets, thereby limiting their financial access to developing economies—but how does that work? And why don’t companies simply opt for a risk-based approach?

In recent years, FinCEN regulations have led many financial institutions to engage in de-risking processes which are essentially terminating relationships with clients or markets because they are perceived as high-risk.

The practice, more common in smaller financial institutes, has impacted Money Service Businesses, notably entities like

- Remittance companies

- Currency exchanges

In 2022, FinCEN and other federal regulators issued a joint statement emphasizing a risk-based approach to customer due diligence. Despite this guidance, the lack of clear parameters led many banks to adopt conservative measures, including de-risking.

The consequence: banks who want to mitigate compliance risks will often make the difficult trade-off of severing all ties with MSBs rather than adopting a proper risk-based approach.

This leads to legitimate MSBs losing access to essential banking services, thereby limiting financial access in developing economies that rely on these services for remittances and other financial activities.

So what’s the solution- how can financial and designated financial institutes comply with tough and often changing FinCEN regulations while also streamlining their processes and reducing manual workload? Are AML automation tools the solution to the FinCEN issue-

let’s analyze.

FinCEN’s Expectations from Businesses- Can Businesses Keep Up?

FinCEN enforces the Bank Secrecy Act (BSA), sets AML regulations, provides guidance, collects financial intelligence, and collaborates with law enforcement to combat financial crime.

Here is what it expects from businesses:

1. A Written and Proper AML Program

Businesses need to design a program with internal controls, procedures, and employee training mechanisms to detect and report SARS.

2. Appointment of a Compliance Officer

The officer will adhere to regulations, update policies, and ensure the training of employees.

3. Conduct Thorough Customer Due Diligence

Implement KYC processes to conduct customer and enhance due diligence.

4. Monitor Transactions and Detect Suspicious Activity

Identify red flags such as structuring, rapid movement of funds, or transactions involving high-risk jurisdictions.

5. File SARS and Currency Transaction Reports

Businesses need to report any transactions that exceed a specific threshold of $10,000.

6. Maintaining Records and Conducting independent audits

This ensures their program is not only effective but also sustainable.

Finding the Balance: What Should Businesses Do?

FinCEN’s regulations alone do not directly create hurdles for businesses and entities. However, the institution could improve efficiency by streamlining reporting processes to reduce unnecessary compliance obstacles.

Additionally, strengthening public-private partnerships for intelligence sharing and adopting best practices from other countries could enhance its effectiveness.

However, given the regulatory landscape, significant changes to FinCEN’s approach are unlikely to happen in the near future.

Businesses can prevent overreliance on manual screening and instead go for automated AML software. Compared to a manual system, a good automated AML tool has the capacity to screen individuals and entities against thousands of watchlists.

The future of AML compliance is complex. Where regulatory bodies are revamping regulations, businesses are finding smarter ways to comply with international and national regulations.

But what is most important- investing in data-driven screening solutions like AML Watcher.

How?

How AML Watcher Assists Organizations in Maintaining FinCEN Compliance

AML Watcher provides a comprehensive suite of tools to improve Anti-Money Laundering (AML) compliance, helping financial institutions comply with FinCEN laws.

It offers:

Adherence to the Bank Secrecy Act (BSA) Requirements

Ensures companies follow FinCEN’s directives & BSA rules by screening customers against sanctions lists, watchlists, and adverse media to find money laundering and terror financing threats.

Improves CDD (Customer Due Diligence)

Supports risk-based compliance by continuously monitoring high-risk individuals and entities, aligning with FinCEN’s focus to stop illegal financial activity.

Reduces False Positives

AML Watcher reduces false positives by using name-matching screening algorithms that analyze risk factors with precision.

It applies advanced entity matching, contextual analysis, and dynamic risk scoring to distinguish legitimate matches from irrelevant alerts, ensuring compliance teams focus only on truly high-risk entities.

Supports Real-Time Compliance Monitoring

It helps institutions track evolving risks in real time by continuously screening against updated watchlists, sanctions, adverse media, and PEP databases, ensuring alignment with FinCEN’s ongoing AML enforcement actions and regulatory updates.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries