A 2026 Guide on AML Compliance

AML Compliance

December 26, 2025

As we step into 2026, financial crime is rapidly evolving. Fraud schemes are getting entangled with money laundering activities, requiring financial institutions to go beyond compliance audits to effectively tackle emerging threats. Regulators have been very specific in their expectations that businesses must demonstrate involvement in preventing financial crime throughout the entire customer lifecycle.

This blog will outline the major modifications to AML compliance by 2026, and give financial institutions the tools and strategies necessary to comply with regulations and combat the increasing risks of money laundering and terrorist financing.

What is AML Compliance?

Anti-money laundering (AML) compliance is a regulatory system that is adopted by an institution to deter, identify, and report any suspicious financial activity. It includes practices, such as customer identity checks (KYC), continuous monitoring of transactions for illegal activity, and countering the financing of terrorism (CFT) to prevent terrorist group financing.

By 2026, the scope of AML compliance has expanded beyond the conventional banking sector to encompass digital assets, fintech platforms, and even decentralized finance (DeFi). The methods used by businesses to counter financial crime should keep up with the advancement in the tactics of financial crimes.

Current compliance with AML requires constant supervision of customer activities and timely reporting of suspicious behavior to regulators, which is a sign of the sophistication of financial offenders and the technological progress that promotes the work of criminals.

The Evolution of AML Compliance in 2026

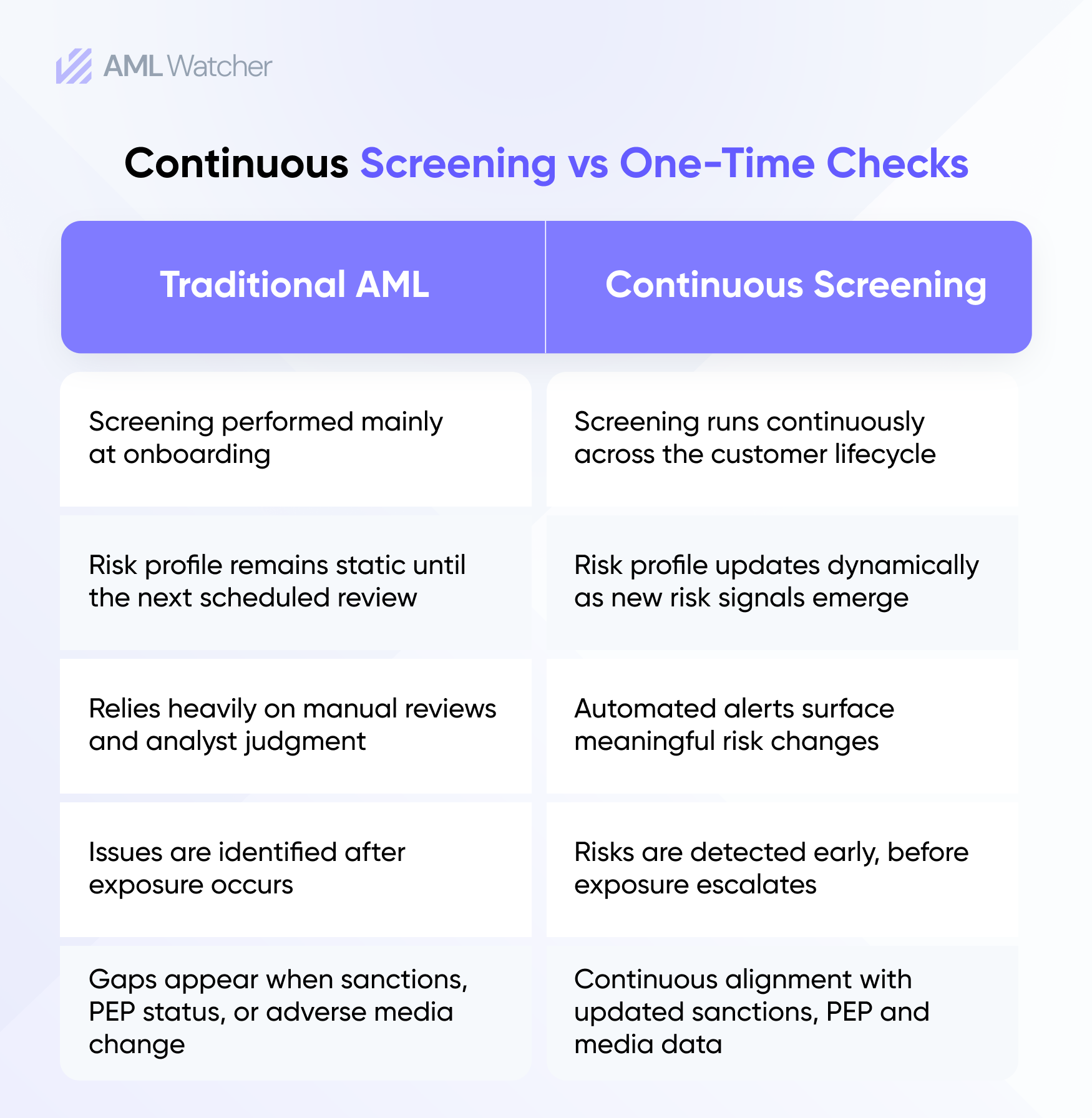

The financial crime landscape is shifting very quickly. The reaction to these changes is that the Financial Action Task Force (FATF), the international body setting anti-money laundering standards, has revised its recommendations to keep pace with the changing risk landscape.

In 2025, FATF updated parts of its Standards and issued updates relevant to risk-based controls, payment transparency, and virtual assets. These changes reinforce expectations that AML programs remain risk-based and responsive as products, channels, and typologies evolve. It implies that in the face of a changing risk environment, institutions are supposed to develop their compliance programs in accordance with the emerging risk environment, as opposed to a one-size-fits-all approach.

The emergence of real-time payment systems and digital assets, including cryptocurrencies and tokenized assets, has offered new ways in which illicit actors can launder money, bypassing traditional financial systems. This change in technology demands that companies implement new screening mechanisms, more effective screening tools, and updated risk assessment frameworks.

In 2026, compliance for financial institutions will involve more than just meeting basic requirements. It will be about building a responsive and scalable compliance ecosystem.

Key Building Blocks of a Successful AML Program in 2026

In order to remain in line with changing regulations, companies need to come up with AML programs that align with their risk appetite while ensuring they meet regulatory requirements. The main pillars of an effective AML program in 2026 are as follows:

-

Risk-Based Approach (RBA)

A risk-based approach is foundational to modern AML compliance. Businesses must evaluate risks on customer and transactional levels, allocating resources to higher-risk areas. By 2026, an efficient RBA must consider:

- Client Risk: This involves assessing the risk posed by various customers, e.g., Politically Exposed Persons (PEPs), customers from high-risk jurisdictions, or clients with complicated financial structures.

- Product and Service Risk: Certain products, such as high-value wire transfers or digital assets, may be more prone to money laundering and require more stringent checks.

- Geographic Risk: There are some areas where financial crime is believed to be high, due to lax regulations and weak enforcement. The businesses need to consider risks according to the geographical distribution of their clients and business processes.

Businesses focusing on higher-risk areas, businesses can ensure that resources are allocated efficiently, reducing the risk of financial crime and compliance violations.

-

Customer Due Diligence (CDD) and Enhanced Due Diligence (EDD)

Customer Due Diligence (CDD) is the core of AML compliance, as it is a process aimed at collecting the necessary information about clients to determine their risk level. In their case, more risky clients, including PEPs or citizens of high-risk jurisdictions, require Enhanced Due Diligence (EDD) measures. This can entail the collection of more data about the monetary history, wealth, and origin of money of the client.

CDD and EDD are important in determining the risks that may happen in advance, and this gives businesses the knowledge to reduce risks of exposure to illegal activities.

-

Ongoing Monitoring and Transactions Audit

Continuous monitoring will be one of the key components of AML compliance in 2026. As digital transactions and real-time payments become a significant trend, companies should regularly monitor their transaction patterns and customer activity. Monitoring systems should be capable of identifying unusual or suspicious behavior, including:

- Large or unusual transactions that are not in accordance with the customer’s normal activity.

- Deals with high-risk jurisdictions or with persons listed in the sanctions or PEP databases.

- Irregularities in the transaction’s destination or origin may indicate efforts to mask illegal activity.

However, effective systems that offer real-time updates and automated alerts can help compliance teams stay ahead of emerging risks.

-

Sanctions and Adverse Media Screening

Sanctions screening plays a critical role in ensuring that businesses do not get involved with companies and individuals who might be under financial sanctions. By 2026, screening should not be confined to a single check during onboarding but should continue throughout the relationship.

Together with the sanctions lists, the businesses will also be required to screen the customers against global watchlists, PEP databases, and adverse media reports to identify any potential risks linked to a specific customer.

-

Suspicious Activity Reporting (SAR) and Internal Governance

Whenever there is suspicious activity, the concerned authorities should be notified of it. This requires organizations to have explicit, well-articulated procedures of identification, reporting, and investigating suspicious transactions.

Moreover, companies are expected to have robust internal controls, such as audit trails, senior management oversight, and periodical review of the compliance framework. This makes the organization responsible and prepared for regulatory scrutiny.

How AML Watcher Supports 2026 AML Compliance

Many institutions expose themselves to enforcement action, if ongoing monitoring has gaps or screening workflows are outdated that can’t capture risk changes during customer lifecycle after onboarding.

AML Watcher supports continuous screening across sanctions, PEP, watchlists, and adverse media, helping teams keep risk decisions current as new signals emerge.

Frequently Asked Questions

AML/CFT regulations refer to laws that aim at deterring and identifying money laundering and terrorist financing activities. They demand that the financial institutions implement preventive measures, including transaction monitoring and customer identity verification.

Risk-based approach enables businesses to channel resources to higher-risk customers and transactions to enhance the effectiveness and efficiency of their AML programs while reducing the cost of business operations.

Continuous monitoring is the act of tracking and analyzing customer transactions to detect suspicious activity. This helps immediately identify the changing patterns of financial crime.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries