Ad-Hoc Vs Batch Screening in AML: Managing Sanctions and Risk

Sanctions

March 18, 2026

- Regulatory Expectations Driving Screening Programs

- What Is Ad-Hoc Screening?

- What Is Batch Screening?

- Ad-Hoc vs Batch Screening: What Sets Them Apart

- Screening Across the Customer Lifecycle

- Data Quality, Technology Challenges, and False Positives

- The Compliance Risk of Getting Screening Wrong

- How AML Watcher Supports Both Screening Models

Most sanctions breaches occur not because policies are missing, but because screening controls are applied at the wrong time or implemented incorrectly.

Sanctions, Politically Exposed Person (PEP), and adverse media screening are core security measures in any anti-money laundering (AML) program, which help institutions find high-risk or restricted individuals before they build any relationships.

The European Union (EU) is quickly expanding its sanctions rules, as it regularly includes new individuals, groups, and sector restrictions through various sanctions packages. Not keeping up with these regulations can lead to serious consequences. According to the FCA, the total fines published as of January 16, 2026, reached £124.2 million, not including court fines.

To navigate this risk, institutions usually employ two operational models: ad-hoc screening and batch screening.

Regulatory Expectations Driving Screening Programs

No regulator mandates a specific screening model, but all expect a risk-based approach that produces continuous, accurate, and auditable results.

The Financial Action Task Force (FATF) sets the global standard that requires ongoing customer monitoring and the ability to detect status changes such as new sanctions listings, PEP exposure, or adverse media.

Recommendation 12 requires Enhanced Due Diligence (EDD) for foreign Politically Exposed Persons (PEPs). Agencies, such as the Office of Foreign Assets Control (OFAC) and the Office of Financial Sanctions Implementation (OFSI), need screenings to counter sanctions lists.

FATF Recommendation 10 establishes the requirement for ongoing customer due diligence, the regulatory basis for continuous batch monitoring of existing customer portfolios.

Moreover, the EU Anti-Money Laundering Directives expand the definitions of PEPs and the documentation needed. Regulators do not prescribe a single screening model. Rather, they anticipate that institutions will adopt risk-based screening processes that integrate various methods.

The EU’s forthcoming single AML Regulation (AMLAR) removes the transposition inconsistencies that allowed uneven implementation under the Directives, directly tightening expectations around screening cadence across member states.

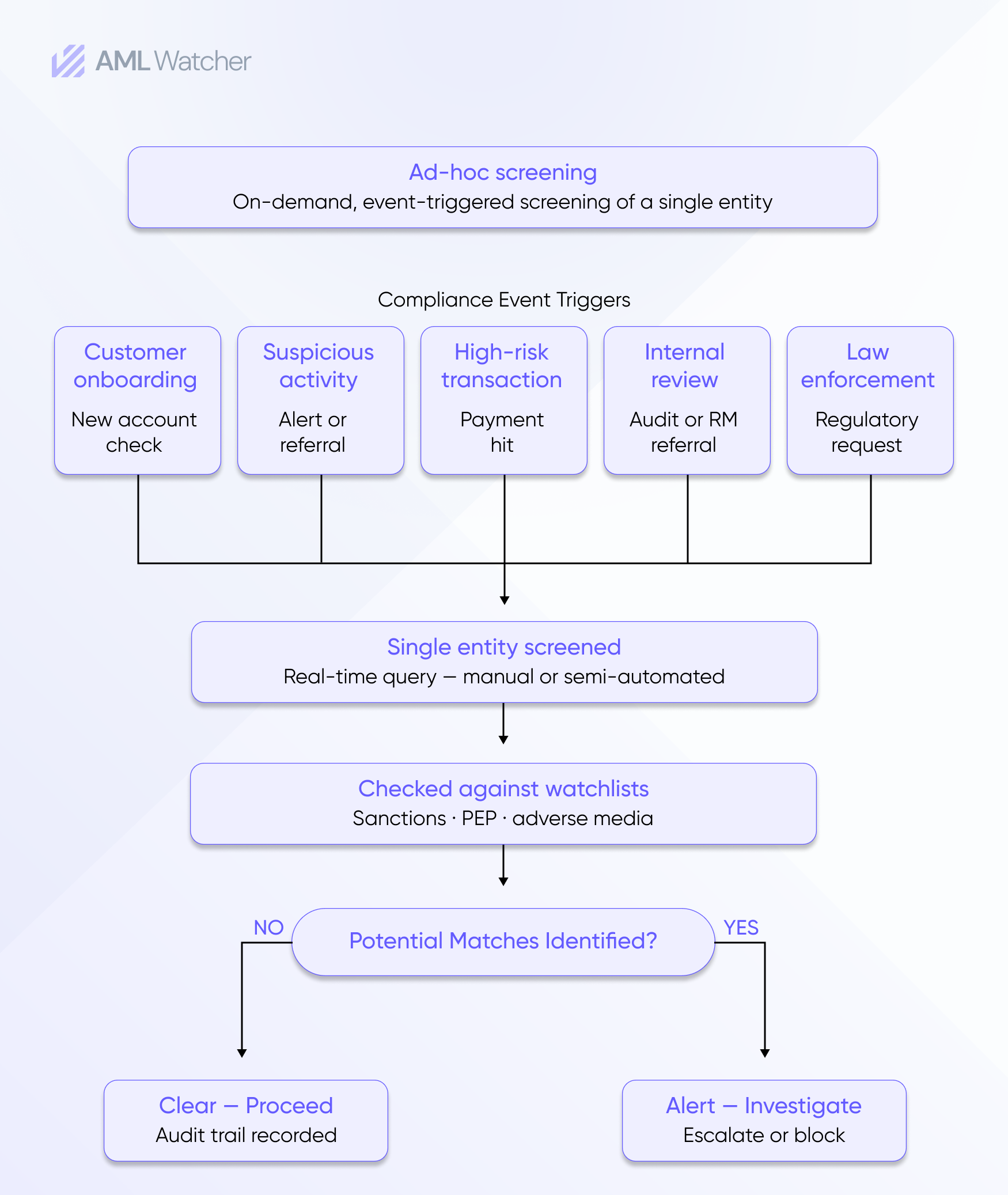

What Is Ad-Hoc Screening?

Ad-hoc screening is the on-demand screening of a single individual or entity within the sanctions lists, PEP databases, and watchlists at a definite point in time. Thus, it is triggered by a specific compliance event rather than a scheduled process.

The defining characteristics of ad hoc screening are its immediacy and specificity. It is real-time, investigation-driven, and frequently implies a human analyst directly querying a screening platform. That targeted quality makes it irreplaceable at decision points, as in onboarding, where a match can block a customer before exposure occurs.

Its limitation is equally clear. Ad-hoc screening cannot systematically monitor an existing customer population. A customer screened clean at onboarding may appear on a new sanctions designation six months later. Without automated monitoring, that change goes undetected until someone manually runs another check.

This constraint is the reason why institutions depend on batch screening to effectively monitor large-scale operations.

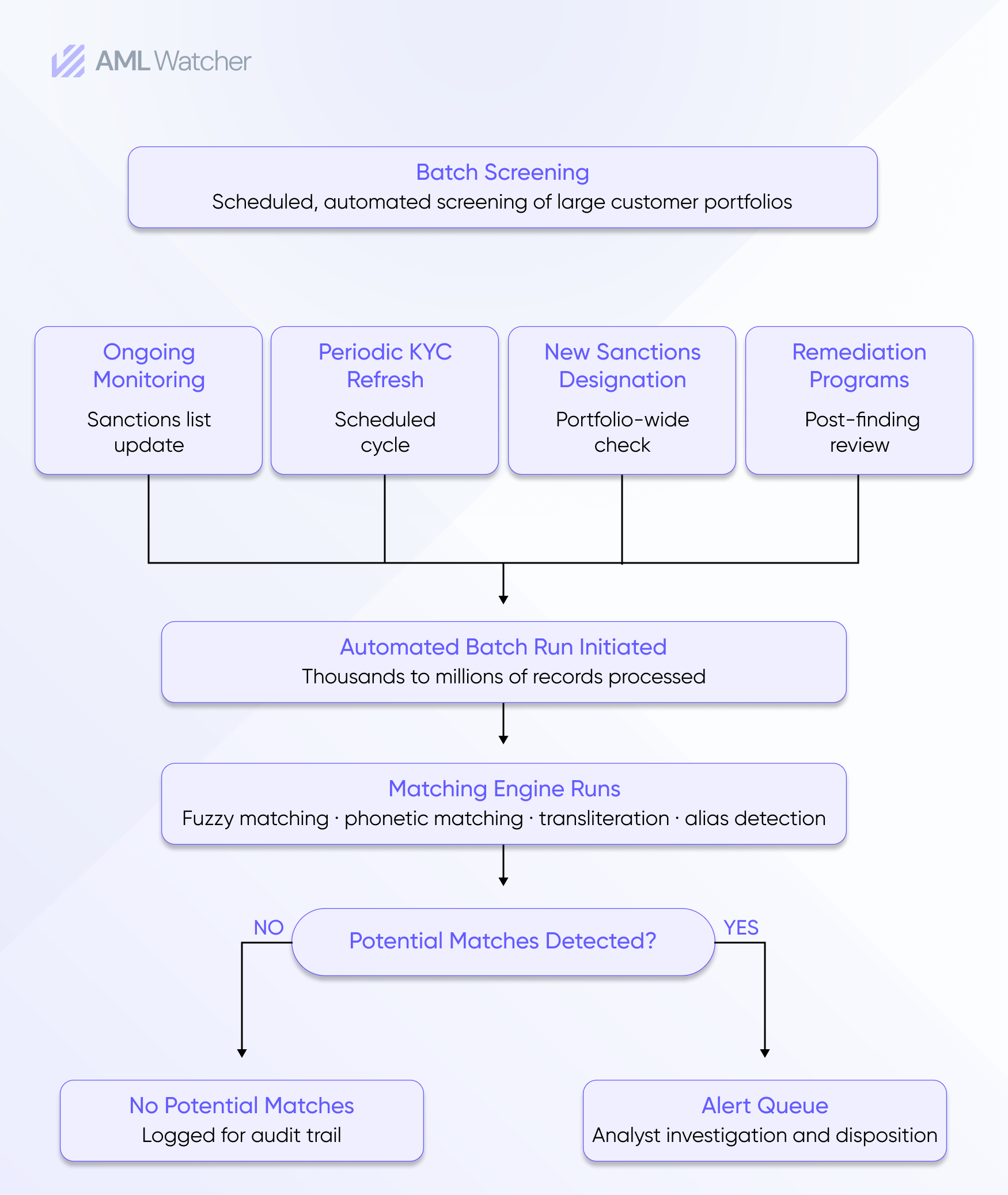

What Is Batch Screening?

Batch screening is an automated process that screens large volumes of customers against sanctions lists, PEP databases, and watchlists at scheduled intervals.

Where ad-hoc screening is triggered by an event, batch screening runs on a cadence, daily, weekly, or even monthly, regardless of whether a specific risk signal has been received. It processes customer portfolios at scale, comparing every record against updated watchlists, which generates alerts when matches occur.

Technically, batch screening systems process thousands to millions of records. They apply automated matching algorithms, such as fuzzy matching and transliteration logic, also then generate alert queues for analyst review.

Poorly tuned batch screening can generate thousands of alerts overnight, overwhelming analysts and obscuring real risks. This isn’t just an efficiency problem: real sanctions matches buried in high-volume alert queues create genuine compliance exposure.

This is the core operational challenge batch screening creates. It also makes data quality and matching accuracy more consequential than in ad hoc screening, where a single analyst reviews a single entity.

Both models serve different purposes, so it’s important to understand how they differ, as this is essential for creating an effective AML screening system.

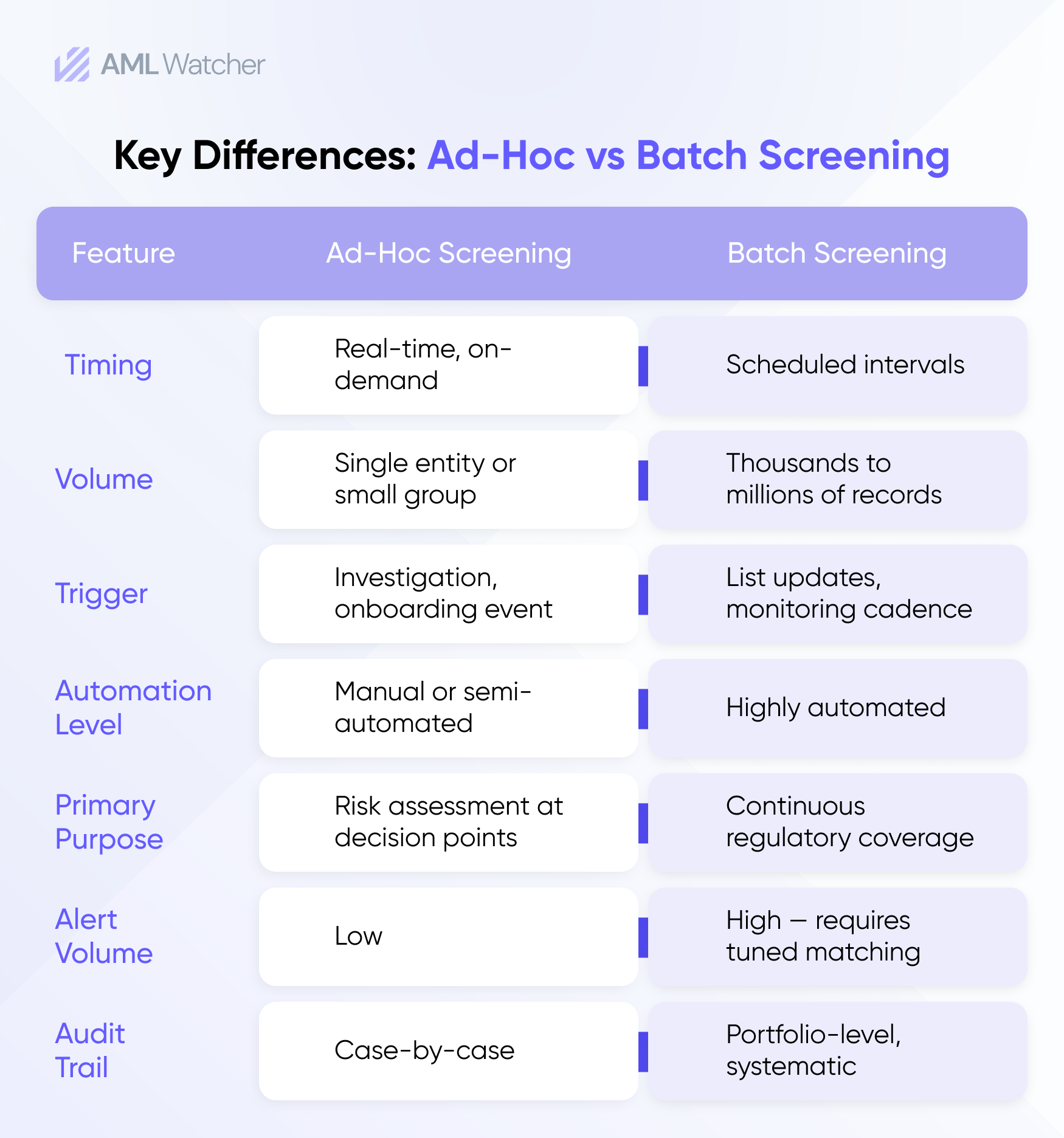

Ad-Hoc vs Batch Screening: What Sets Them Apart

Ad-hoc screening supports decision-making at critical compliance moments. Batch screening ensures regulatory coverage does not lapse between those moments. Neither model, used in isolation, satisfies current regulatory expectations.

Screening Across the Customer Lifecycle

The most effective AML programs do not treat screening as a single checkpoint. They integrate it across multiple stages of the customer lifecycle, using each approach where it is operationally most effective.

Onboarding is the primary use case for ad-hoc sanctions screening. Before bringing a new customer on board, a real-time check is conducted to ensure that the individual or entity is not listed on sanctions lists, does not fall under PEP criteria that would require enhanced due diligence, and has no negative media reports that could escalate risk. The result determines whether the relationship proceeds.

Transaction monitoring generates ad-hoc screening triggers throughout the relationship. When a transaction alert fires, an unusual payment pattern, a counterparty in a high-risk jurisdiction, an amount threshold breach, a compliance analyst may conduct an immediate screening check as part of the investigation workflow. Payment screening at the transaction level adds a real-time layer that catches sanctioned beneficiaries before funds are transferred.

Ongoing monitoring is where batch screening delivers its core value. Batch screening automatically re-screens existing customers against updated watchlists and risk signals. Without automated batch screening, institutions cannot guarantee that a customer who was clean at onboarding remains clean today.

Periodic KYC refresh combines both approaches. Batch screening identifies which customers require updated documentation or enhanced review. Ad-hoc screening is then used during the refresh process itself to confirm the current status before the relationship is re-approved.

Insight:

Effective AML programs integrate screening into multiple stages of the customer lifecycle rather than relying on a single control point.

Data Quality, Technology Challenges, and False Positives

Screening is only as accurate as the data it runs against. Compliance teams depend on third-party risk intelligence datasets, sanctions lists, PEP databases, law enforcement watchlists, and adverse media feeds, each with varying coverage, update frequency, and consistency.

Common names generate large volumes of alerts. Transliteration often results in different spellings, complicating the matching of names across scripts. Moreover, sanctions designations might include aliases, partial names, or names written in non-Latin characters that create real challenges for accurate matching, even for advanced systems. Modern watchlist screening platforms address these problems using fuzzy matching algorithms, phonetic matching, and transliteration logic, but implementation quality varies widely.

The industry consequence of poor tuning is measurable. Industry studies estimate that around 90% of AML screening alerts are false positives. For batch screening in particular, this creates a severe operational burden: compliance analysts reviewing hundreds of alerts per day to identify a handful of genuine matches is not an effective use of compliance resources. It also creates a secondary risk, genuine hits buried in a high-volume alert queue may receive insufficient attention.

The technology challenge is not simply implementing screening. It is implementing screening that generates actionable results without overwhelming the team responsible for reviewing them.

The Compliance Risk of Getting Screening Wrong

Inadequate screening carries well-documented regulatory, financial, and reputational consequences.

Breaching sanctions can lead to civil monetary penalties, criminal referrals, and public enforcement actions from authorities such as OFAC, OFSI, and various national financial regulators. In the UK, the Financial Conduct Authority (FCA) has taken action against institutions that exhibited systemic failures in their screening processes. This was not due to a lack of screening tools, but rather because the implementation of those tools was insufficient.

The pattern in major enforcement cases is consistent. Institutions had screening systems in place. The systems were poorly configured, infrequently updated, or generating alert volumes that overwhelmed the teams responsible for review. Real sanctions exposure slipped through, not because the list was unavailable, but because the operational model could not process it effectively.

Reputational damage compounds the financial penalty. Being publicly identified as the institution through which a sanctioned entity transacted creates lasting consequences with correspondent banks, regulators, and clients that no fine calculation captures.

Insight:

In many enforcement cases, the issue is not the absence of screening tools but the ineffective implementation of screening controls.

How AML Watcher Supports Both Screening Models

Ineffective screening models put institutions at risk of facing sanctions violations, regulatory penalties, and operational inefficiencies.

AML Watcher enables compliance teams to unify ad-hoc and batch screening within a single platform, ensuring real-time decision-making and continuous monitoring without operational overload.

With access to 215+ sanctions regimes and 3,500+ watchlists, combined with AI-driven risk scoring, teams can reduce false positives, accelerate investigations, and stay ahead of regulatory expectations.

Ongoing portfolio monitoring, driven by TruRisk AI, decreases false positives by 44% and minimizes manual reviews by as much as 70%-80%. This empowers compliance teams to concentrate on real risks that matter.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries