Hedge Fund & PE AML Compliance Guide for RIAs and ERAs

AML Compliance

April 29, 2026

- Which Investment Advisers Does the FinCEN AML Rule Cover?

- What Are the LP Onboarding Challenges in Private Equity AML?

- Where Do Hedge Fund KYC Screening Programs Typically Fail?

- How Are KYC Requirements for Investment Advisers Changing?

- Why Should RIAs Build an AML Program Before the 2028 Deadline?

- How to Structure a Defensible Investor Screening Process?

- How AML Watcher Supports Alternative Asset Compliance Teams

Industry scrutiny around private market investments has intensified as concerns grow over how complex fund structures can obscure beneficial ownership and enable illicit financial flows. Investigative reporting, including analysis of leaked law enforcement intelligence, has revealed issues in the structures of private equity and hedge funds that are hard to see through.

These revelations have highlighted regulators’ longstanding concerns about the lack of oversight of anti-money laundering in the investment adviser industry. Regulatory focus on investment advisers has intensified heading into 2026 as authorities move to close long-standing gaps in AML oversight.

In August 2024, the Financial Crimes Enforcement Network (FinCEN) finalized the Investment Adviser AML Rule, bringing Registered Investment Advisers (RIAs) and Exempt Reporting Advisers (ERAs) under the scope of the Bank Secrecy Act for the first time. In January 2026, FinCEN delayed implementation to January 1, 2028. However, expectations from custodians, prime brokers, and institutional investors have advanced faster than the regulatory timeline. The rule ensures these entities are subject to formalized AML/CFT compliance programs, including suspicious activity reporting (SAR) and recordkeeping.

In January 2026, FinCEN deferred the rule’s implementation until January 1, 2028. The delay recognizes the importance of harmonizing regulatory standards with the many business models in the investment adviser sector.

For CCOs and compliance managers in alternative assets firms, this delay is an opportunity to plan and prepare. Custodians and prime brokers are now demanding to see the firm’s AML program, and institutional allocators are becoming more interested in seeing investor screening programs. Meanwhile, sanctions exposure linked to opaque investor structures is still present as an active enforcement risk. Custodians now expect to review AML programs before opening accounts, and institutional investors request screening frameworks during onboarding. The 2028 date is regulatory, but operational expectations already apply.

Which Investment Advisers Does the FinCEN AML Rule Cover?

The 2024 rule expands the definition of “financial institution” under the BSA to include certain Registered Investment Advisers and Exempt Reporting Advisers, a total of about 14,000 RIAs and 6,000 ERAs managing over $100 trillion in combined assets, according to FinCEN’s adopting release. Covered firms are required to implement AML/CFT programs, file SARs, and maintain recordkeeping obligations, which shows a clear move toward direct regulatory control.

As a result, it excludes state-registered advisers, foreign private advisers without a US place of business, or less than 15 US-person clients, or less than $25 million in AUM attributable to US investors. A related FinCEN/SEC money laundering opportunity for illicit actors on Customer Identification Programs will soon follow, and FinCEN has indicated that the rules will be harmonized. The practical guidance most legal advisers are giving covered firms: progress on the components least likely to change, and build toward the rule’s core structure now.

What Are the LP Onboarding Challenges in Private Equity AML?

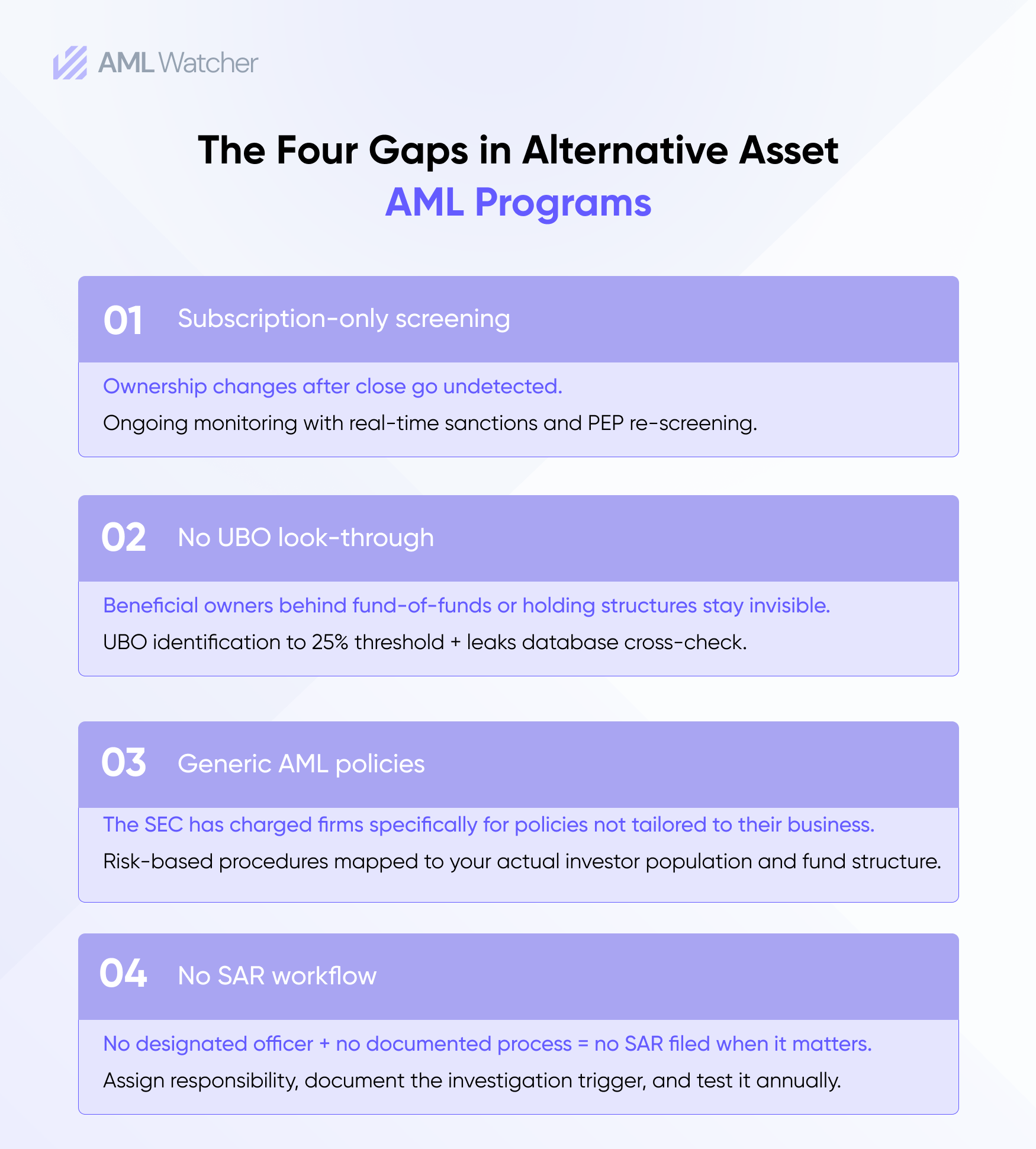

Private equity structures create investor screening complexity that standard financial institution KYC frameworks were not designed for. Limited partners frequently include fund-of-funds vehicles that obscure underlying investors, family offices with multi-layer beneficial ownership chains, and non-US entities from jurisdictions with limited ownership disclosure standards. The IA AML Rule requires risk-based due diligence on these relationships, a program approach based on the actual exposure each investor presents, rather than depending on generic onboarding checks.

A regulatory body like the Financial Action Task Force has repeatedly highlighted beneficial ownership transparency as a known gap in private investment structures.

A compliant private equity AML program needs four components: written policies and controls reasonably designed to prevent the firm from being used for money laundering or terrorist financing; independent testing by internal audit or a qualified external party; a designated AML compliance officer (which can be the existing CCO); and risk-based Customer Due Diligence with ongoing monitoring.

During LP onboarding, this means verifying the identity of legal entity investors, UBO identification for those controlling 25% or more, source of funds documentation, and sanctions screening, along with the PEP screening at subscription, plus re-screening when ownership structures change. FinCEN highlighted that historically lighter compliance in the sector created opportunities for illicit actors, indicating where regulatory focus will increase.

Where Do Hedge Fund KYC Screening Programs Typically Fail?

Hedge fund investor bases include high-net-worth individuals, sovereign wealth funds, pension plans, and family offices. Each presents a different risk profile that cannot be adequately addressed through a single-tier KYC process. A domestic US high-net-worth investor with clean adverse media warrants standard CDD. A foreign national from a FATF grey-listed jurisdiction requires enhanced due diligence. A family office whose beneficial owner holds a Level 2 PEP designation, a member of parliament, a senior executive of a state-owned enterprise requires enhanced scrutiny under FATF Recommendation 12, regardless of whether the family office entity itself appears on any list.

Hedge fund KYC screening failures are structural rather than individual. The typical gap is not a name missed on OFAC’s SDN list; it is the failure to assess investor-level PEP exposure and adverse media risk when ownership sits behind a holding company, or a failure to re-screen during a secondary LP transfer. SEC enforcement actions have specifically targeted firms for deploying generic AML policies not tailored to their business and for inadequately reviewing transactions. The enforcement risk is documented, and the bar is rising.

How Are KYC Requirements for Investment Advisers Changing?

Before the 2024 rule, investment adviser KYC requirements existed mainly through the demands of banks, custodians, and prime brokers. Those counterparties are fully BSA-covered and require their investment adviser counterparts to provide beneficial ownership data and investor screening evidence as a condition of the account relationship. Investment advisers have been operating under informal KYC expectations driven by counterparties for years, without direct regulatory accountability that follows direct FinCEN examination authority.

The 2024 rule changes that by bringing RIAs and ERAs under BSA obligations and adding SAR filing requirements currently applicable only to banks and broker-dealers. For CCOs at RIAs today, building toward these requirements is simultaneously regulatory preparation and a competitive necessity. A documented investor AML compliance program, covering initial screening, risk tiering, ongoing monitoring, and a full audit trail, is increasingly a threshold requirement for institutional capital.

The 2028 deadline provides time for proper implementation, yet AML expectations are already being applied across investor onboarding and capital allocation. Firms that postpone action face immediate operational and compliance risks.

Why Should RIAs Build an AML Program Before the 2028 Deadline?

The regulatory timeline extension does not delay market expectations. Custodians, prime brokers, and institutional investors require demonstrable AML controls before being able to provide capital to new firms or open accounts. Firms that delay implementation risk operational friction, delayed fundraising, and increased scrutiny from counterparties. Therefore, meeting FinCEN expectations is not just about regulatory compliance but also about commercial necessity.

How to Structure a Defensible Investor Screening Process?

Initial onboarding screening lays the groundwork for investor AML compliance and includes identity verification for legal entities and natural persons, UBO identification, source of funds documentation, and screening against OFAC sanctions, FinCEN watchlists, global PEP databases, and adverse media. Non-US investors from higher-risk jurisdictions require EDD, additional documentation of wealth origin, and a deeper review of the investor’s network for PEP and sanctions linkages.

Risk tiering translates screening results into defined investor risk categories that guide monitoring intensity. Higher-risk investors, those with PEP exposure, non-US jurisdictional profiles, or with complex ownership structures, require more frequent re-screening and closer scrutiny.

Ongoing monitoring is where most current programs are weakest. A lack of re-screening against updated lists, in addition to initial screening, is a significant compliance gap. The EU introduced 695 financial sanctions in 2024 alone; thus, a beneficial owner who was clean at fund close can appear on a sanctions list within weeks.

SAR readiness requires a documented investigation workflow, along with a designated responsible officer, and the ability to file for transactions involving $5,000 or more in suspicious funds. This remains one of the least developed areas across many private market AML programs.

How AML Watcher Supports Alternative Asset Compliance Teams

Many investment firms often find it difficult to set up investor AML programs that keep up with changing regulatory expectations while dealing with complicated ownership structures, along with continuous monitoring requirements.

AML Watcher supports firms with advanced screening capabilities, risk-based monitoring, and detailed tracking logs designed for modern AML compliance.

Frequently Asked Questions

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries