GENIUS Act Compliance for Stablecoin Issuers with AML Controls

AML Compliance

April 29, 2026

- The Compliance Gap No One Priced Into Stablecoin Regulation

- How the GENIUS Act Redefines Stablecoin Issuers as Financial Institutions

- Customer Due Diligence in Stablecoin Ecosystems

- Identity Verification And Onboarding Requirements

- Transaction Monitoring Across Primary and Secondary Markets

- Stablecoin OFAC Screening and Wallet-Level Sanctions Enforcement

- GENIUS Act FinCEN Obligations and Governance Accountability

- System Architecture Requirements for GENIUS Act Readiness

- Key Enforcement Risks For Stablecoin Issuers

- Compliance As An Operational Capability

- How AML Watcher Supports the GENIUS Act Compliance

Stablecoin regulation in the United States has entered a clearly defined enforcement phase following the enactment of the GENIUS Act. This legislation, signed into law on July 18, 2025, firmly establishes stablecoin issuers as primary participants in the financial and regulatory framework by classifying them as financial institutions under the Bank Secrecy Act.

What started as guidelines for transparent governance and control mechanisms for issuance has now become a detailed system for preventing money laundering, also complying with sanctions rules.

The Financial Crimes Enforcement Network (FinCEN) and the Office of Foreign Assets Control (OFAC) released a joint Notice of Proposed Rulemaking (NPRM) on April 8, 2026. This notice outlines how their legislative goals will translate into concrete operational requirements.

The final regulations are expected to be unveiled by July 2026, and enforcement is set to commence on January 18, 2027.

The Compliance Gap No One Priced Into Stablecoin Regulation

The gap has shifted from a theoretical concern to an operational challenge for stablecoin issuers. They are now required to execute the systems supporting customer due diligence and real-time blockchain transaction monitoring. The system must additionally deploy sanctions controls across both centralized and distributed settings while remaining compliant.

The actual challenge lies in implementing compliance at scale across fragmented blockchain environments, rather than recognizing its necessity.

How the GENIUS Act Redefines Stablecoin Issuers as Financial Institutions

The GENIUS Act addresses the regulatory uncertainty that previously distinguished compliance programs in the digital asset ecosystem from those in banks. Now, permitted payment stablecoin issuers are considered financial institutions under the Bank Secrecy Act.

This status brings a comprehensive anti-money laundering and counter-terrorist financing program. It includes:

- Risk-based AML program consistent with bank standards

- Engagement of a competent compliance officer in the United States

- Annual independent testing of the AML and sanctions program

- Regular workforce training programs correspond with risk

- Certification of the program’s adequacy by senior compliance management

An important governance measure is the prohibition on compliance officers. Those with prior convictions for financial crimes, including fraud, along with the insider trading, and cybercrime, cannot serve in the role.

The April 2026 Notice of Proposed Rulemaking (NPRM) elevates the expectations. It mandates issuers to have the underlying systems needed to freeze, cancel, or reject transactions at the protocol level. This is a major move from policy compliance to imparting technical controls.

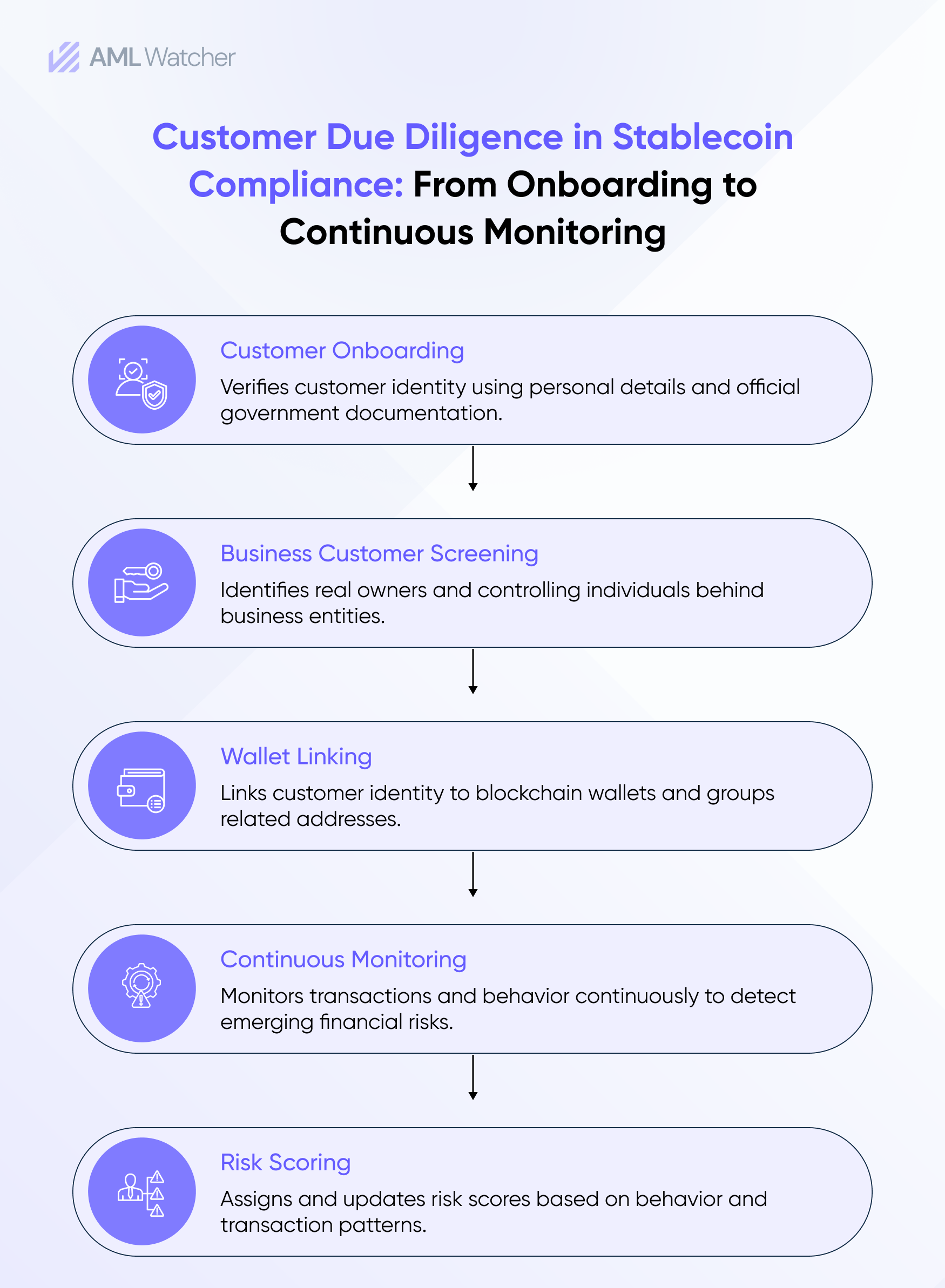

Customer Due Diligence in Stablecoin Ecosystems

Customer Due Diligence under the GENIUS Act follows BSA principles but expands in scope due to blockchain-based asset flows.

Identity Verification And Onboarding Requirements

For primary market transactions like minting and redemption, issuers need a Customer Identification Program (CIP) that requires the following from the customer:

- Legal name

- Date of birth

- Residential address

- Government ID number

For legal entities, the beneficial ownership rules require identifying individuals who hold 25% or more of the entity and the ultimate controlling persons.

An “account” is any formal relationship with an issuer for the provision of financial services. This means the onboarding requirements apply only to relationships involving an issuer, not to all wallets that hold stablecoins in circulation.

Continuous Identity Intelligence

Onboarding is just one part of the Customer Due Diligence. Stablecoin issuers must perform ongoing identity authentication to link real-world individuals and businesses on their blockchain infrastructure activities. This encompasses:

- Wallet attribution and clustering

- Behavioral correlation across addresses

- Continuous risk reassessment based on transaction behavior

A wallet that appears low-risk throughout the onboarding process may later engage with sanctioned entities, mixers, or high-risk decentralized protocols. Under the GENIUS Act within the guidance framework, it is essential to that risk classification adapts and also evolves as a reaction to these changes.

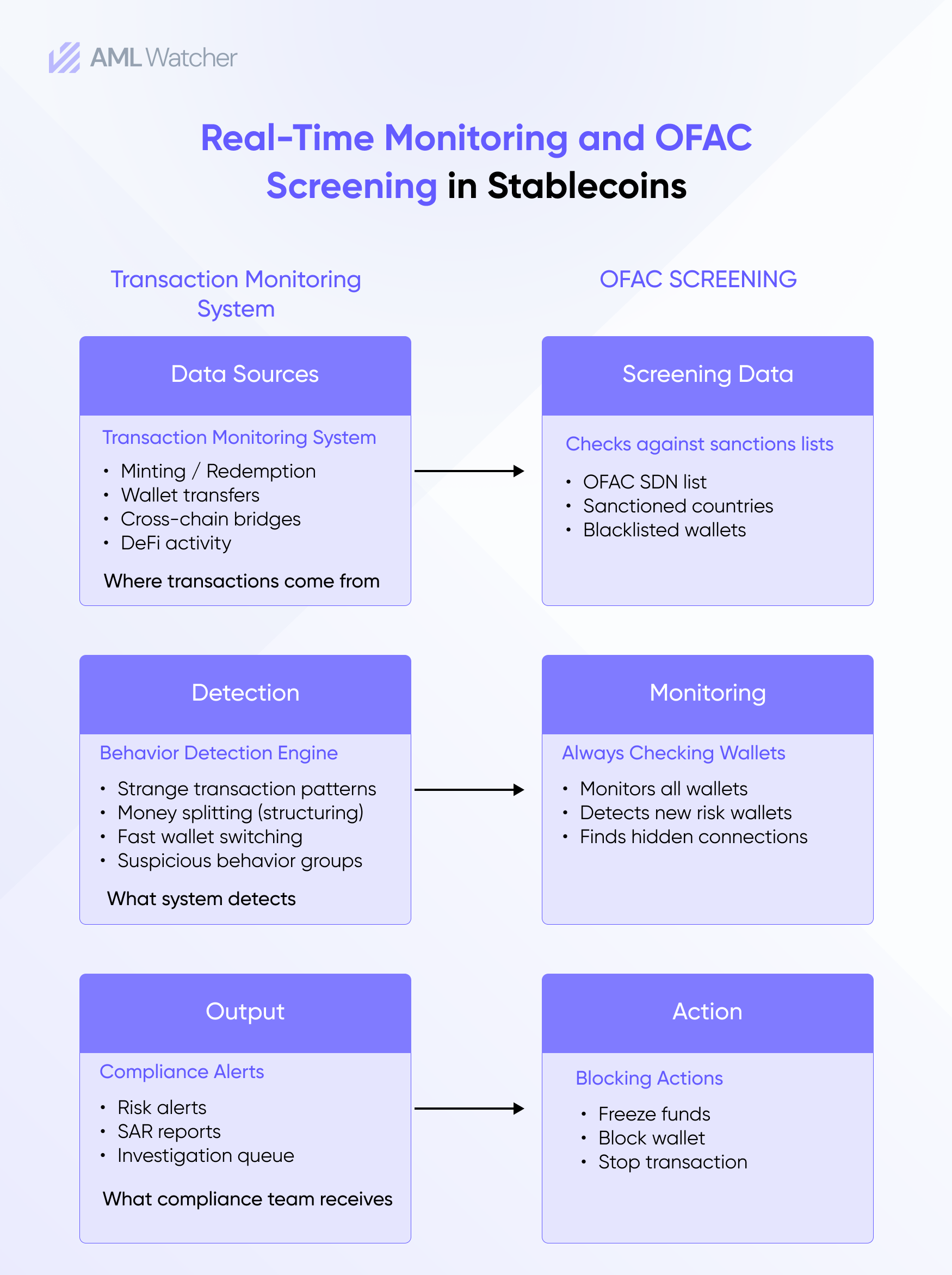

Transaction Monitoring Across Primary and Secondary Markets

Transaction monitoring is one of the most challenging aspects of the GENIUS Act, given that it spans both primary and secondary markets.

Primary Market Monitoring Obligations

For the minting and redemption transactions where the issuer is a counterparty, the obligations include:

- Suspicious Activity Report filing for relevant transactions

- Monitoring for structuring and laundering patterns

- Currency Transaction Reports for applicable thresholds

The SAR threshold is set at $5,000, a limit that is aligned with banking regulations rather than those for money services businesses. This creates a more stringent reporting environment for stablecoin issuers, thereby improving their understanding of regulatory standards.

Secondary Market Monitoring Expectations

Transactions in the secondary market do not activate the requirements for Suspicious Activity Reports (SAR). However, issuers are still expected to have a monitoring regime that is able to effectively detect:

- Exposure to sanctioned wallet addresses

- Interaction with high-risk blockchain entities

- Cross-chain movement through bridges as well as DeFi protocols

- The models for layering across various wallets

FinCEN’s approach is straightforward, since it would be counterproductive to report all secondary transactions as SARs. However, it is also unacceptable to ignore the secondary market risks.

This results in a two-tiered monitoring expectation where issuers must strike a balance between regulatory efficiency and the ability to notice peculiar behavior effectively.

Stablecoin OFAC Screening and Wallet-Level Sanctions Enforcement

The GENIUS Act’s compliance with OFAC regulations extends beyond traditional name screening.

Therefore, the Stablecoin issuers are considered U.S. persons under OFAC. As a result, sanctions considerations apply to the issuance, redemption, and secondary market exposure of these stablecoins.

Expanded Screening Scope

OFAC compliance now includes:

- Wallet-based SDN and sanctions list screening

- Ongoing screening of previously vetted wallets

- Monitoring indirect risks from DeFi protocols, as well as bridges

- Ability to block or freeze sanctioned assets in real time

One important development in the regulations is that the risk of sanctions now also applies to parties beyond the direct counterparties. If a sanctioned entity transacts in any way with a stablecoin, it is anticipated that stablecoin issuers will be able to identify and respond accordingly.

Technical Enforcement expectations

The GENIUS Act requires the Treasury to work together with issuers when sanctions are designated. This requires operational readiness to:

- Identify affected wallets immediately

- Freeze or block assets without delay

- Take sanctions actions through programmable contract or protocol-level controls

Sanctions compliance has therefore shifted from static screening to real-time enforcement.

GENIUS Act FinCEN Obligations and Governance Accountability

Beyond operational controls, the GENIUS Act introduces governance-level accountability that directly impacts compliance leadership.

Program Certification Requirements

Issuers must certify the effectiveness of their anti-money laundering and sanctions programs for the prevention of illicit monetary transactions within 180 days of authorization, and thereafter annually.

This certification establishes personal accountability for compliance leaders. Thus, transforming the effectiveness of these programs into a regulatory obligation rather than merely a policy statement.

Examination Expectations

Regulators are expected to evaluate:

- Transaction monitoring logs, along with the alert histories

- Model verification and refining documentation

- SAR escalation timelines

- Audit trails used for sanctions decisions

- Evidence of continuous risk evaluations

Explainability has now become a critical feature of compliance systems. It’s important that these systems can explain why a transaction is marked or cleared, especially when automated or AI systems are used.

System Architecture Requirements for GENIUS Act Readiness

Regulatory requirements have progressed to include system architecture in addition to control mechanisms. Simply relying on disjointed compliance solutions is no longer sufficient.

A compliant architecture generally includes three interrelated layers:

If there’s no integration among these layers, issuers encounter repeated alerts, delayed identification of issues, and inconsistent risk assessments.

Key Enforcement Risks For Stablecoin Issuers

Regulators are expected to focus their enforcement efforts on more extensive systemic concerns instead of being distracted by minor errors made by individuals. Key risk areas to keep an eye on include:

- Failure to detect indirect sanctions exposure

- Delayed identification of structuring across multiple wallets

- Inability to freeze assets after designation updates

- Lack of cross-chain visibility in monitoring systems

- Overreliance on onboarding-only KYC controls

The effectiveness of compliance will be assessed based on detection capabilities during transactions rather than on the quality of policy documentation.

Compliance As An Operational Capability

In stablecoin environments where false-positive rates can rise above 80% to 90%, thus, this makes efficiency an important requirement for regulation. The GENIUS Act indicates an underlying change in how stablecoin regulation is approached. Compliance is no longer just about keeping records; it now includes operational capabilities as well.

Customer due diligence must advance into a system of continuous identity intelligence. Transaction monitoring should function in real time across blockchain networks. Additionally, OFAC screening needs to extend to wallet-level enforcement and the detection of indirect exposure.

A key challenge for stablecoin issuers lies in achieving uninterrupted integration. For maximum effectiveness, identity verification, reviewing transaction activity, and sanctions data need to operate as a coherent unit. Therefore, this integrated collaboration facilitates real-time detection, swift escalation, and transparency that is ready for audits.

Issuers who prioritize developing scalable, integrated compliance infrastructure from the outset will be better positioned to withstand oversight from regulators as enforcement efforts ramp up in 2027.

Bank-Level Compliance Expectations in a Non-Banking Infrastructure

This regulatory shift places stablecoin issuers closer to banks in terms of compliance expectations, while still operating in a technologically distinct environment. This mismatch increases both operational cost and regulatory risk.

How AML Watcher Supports the GENIUS Act Compliance

The compliance demands introduced by the GENIUS Act require unified infrastructure across identity, transaction monitoring, and sanctions screening.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries