AML in Gambling & iGaming for UK Gambling Commission & MAS 2026

Others

May 5, 2026

- Why AML Gambling Risk Is Escalating Across Global Markets

- UK Gambling Commission Expectations Shaping AML Gambling Compliance

- Singapore’s Regulatory Stance On Gambling-Linked Financial Flows

- Where Global Regulatory Pressure Converges

- Screening Gaps That Put Operators At Risk

- Building A Unified AML Gambling Screening Workflow

- Compliance in 2026 Demands More Than A Screening Checkbox

- How AML Watcher Supports Gaming Compliance Teams

Recent regulatory reviews have suggested that a notable share of UK gambling operators may not be meeting expected AML standards. At the same time, the largest money laundering case in Singapore, which is valued at $3 billion, exposed how illicit funds were routed through remote gambling facilities.

These developments indicate that the gambling sector is continuing to evolve. Gambling operators continue to face challenges in understanding the complex flow of money, even though there are anti-money laundering (AML) controls in place. In 2026, pressure has increased as the UK Gambling Commission (UKGC) and the Monetary Authority of Singapore (MAS) apply stricter requirements, but without a shared framework.

Why AML Gambling Risk Is Escalating Across Global Markets

Gambling operators are classified as Designated Non-Financial Businesses and Professions (DNFBPs) according to the FATF Recommendation 22. This means they are expected to implement enhanced due diligence measures that are similar to those of financial institutions and are in practice.

The digital onboarding, along with the crypto deposits and instant payments, now move funds faster than most AML systems and human reviews can realistically keep up with. Most operators have not yet aligned their AML programs with these operational demands.

Alongside this, the gambling platforms are also highly attractive to money launderers for reasons beyond transaction volume. The deposits, gameplay, winnings, and withdrawals create movement of funds that looks similar to normal customer behavior in other cases. According to the UKGC, the Videoslots case in 2025 directly highlighted this issue: a customer managed to deposit over £75,000 in prepaid digital vouchers within just 16 days, spreading the funds across four different bank accounts. It was not until the automated risk scoring tools by the operator flagged the activity that a review was initiated.

Regulatory findings in both jurisdictions point to repeated transaction behaviors that raise suspicion of illicit fund movement. These include::

- Structured deposits below reporting cut-offs are intended to avoid triggering due diligence

- Third-party funded accounts, obscuring the source of funds and beneficial ownership

- Rapid withdrawal after minimal gameplay, indicating layering activity

- The use of wallet-based systems and prepaid instruments weakens transaction traceability

These are not isolated incidents. Regulators in the UK and Singapore are already informed by these behaviors as the basis for enforcement actions.

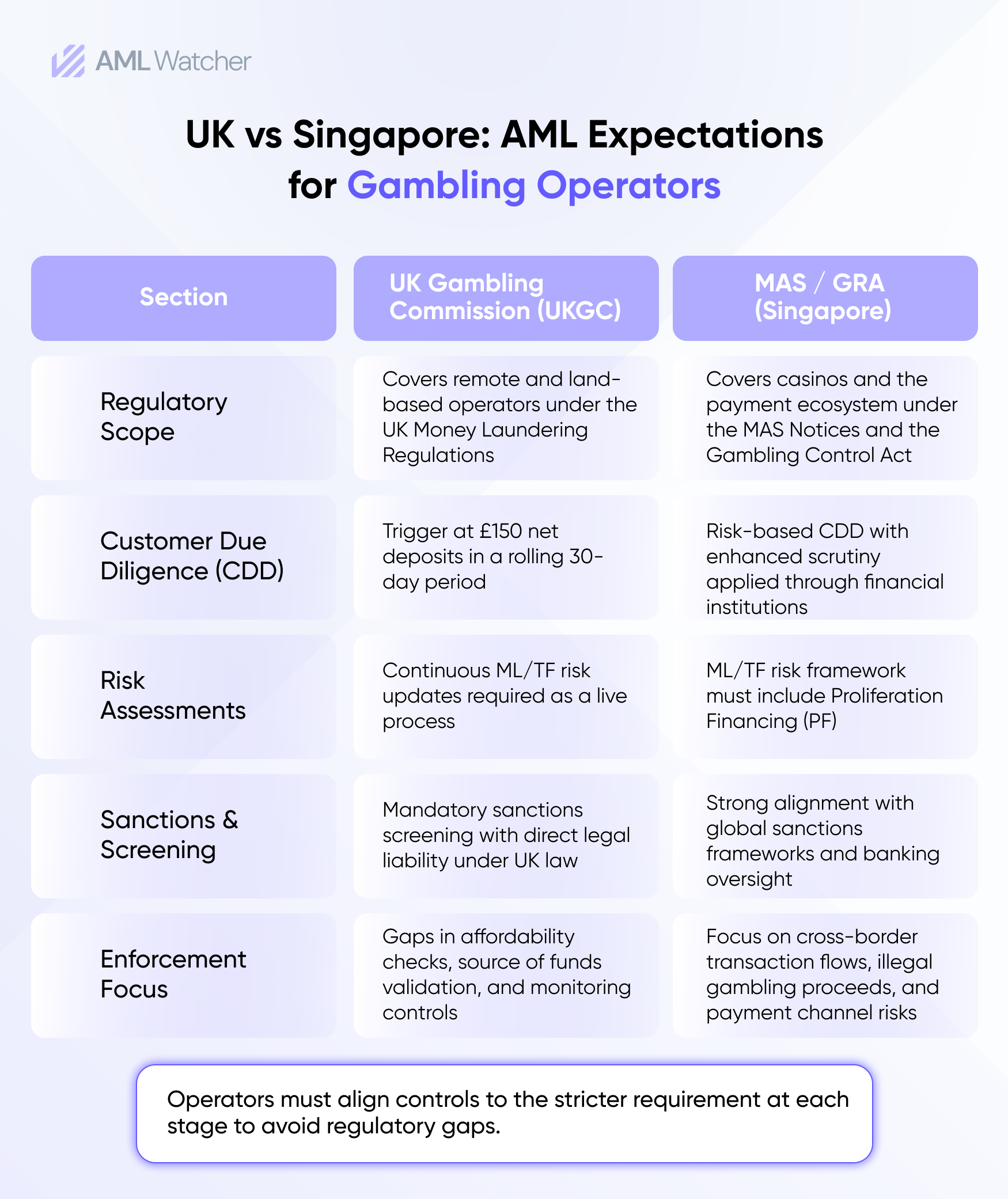

UK Gambling Commission Expectations Shaping AML Gambling Compliance

According to the Annual report and accounts 2024-2025 by the UKGC, the UKGC carried out 9,700 compliance actions in 2024/25, compared to 4,200 in the previous year. This reinforces its increased attention to AML compliance controls, as one in four operators fails to achieve satisfactory ratings.

However, recent enforcement cases provide a clear view of where AML controls remain inadequate. The Betfred penalty, for example, identified source of funds thresholds set at £15,000 in customer losses or £125,000 in stakes over 12 months as too high to be risk-based. The Videoslots case focused on automated risk scoring that overlooked the warning signs of high-value digital voucher deposits, quick fund transfers, and withdrawals to multiple destinations. These factors, when combined, formed a risk cluster that should have prompted an immediate evaluation.

Therefore, the UKGC compliance expectations now emphasize early-stage intervention alongside ongoing monitoring. Key expectations now include:

- Source of funds verification triggered at earlier different stages from onboarding to exit, not only at high-loss thresholds

- Continuous ML/TF risk assessments replacing annual static reviews

- Mandatory sanctions screening under the Money Laundering, Terrorist Financing and Transfer of Funds Regulations 2017 and enhanced PEP guidance updated in October 2025

- Specific due diligence on open-loop payment instruments, including prepaid digital vouchers and crypto deposits

- B2B relationship risk assessment, operators must now assess money laundering exposure linked to their business-to-business partners, not just their customers

In 2025, the UK Gambling Commission revised its casino guidelines to comply with the revised treatment of domestic Politically Exposed Persons under the FCA’s new PEP guidance. The changes also included modifications to the definitions of high-risk third countries and adjustments to the thresholds for POCA’s ‘consent’ requests. Operators relying on 2023-era compliance frameworks are operating outside these updated requirements.

While the UKGC has increased enforcement activity, Singapore has moved toward a different but equally strict approach following a major financial crime case.

Singapore’s Regulatory Stance On Gambling-Linked Financial Flows

Singapore’s $3 billion money laundering case led to enforcement actions against multiple institutions for failures in customer risk assessment, source of wealth authentication, along with the transaction monitoring. A total of 17 individuals were prosecuted for laundering proceeds linked to online gambling operations in the Philippines, unlicensed moneylending in China, and fraud. MAS subsequently imposed $27.45 million in composition penalties on nine financial institutions in July 2025 for failures traced to that investigation.

AML compliance in casinos is regulated by the Gambling Regulatory Authority (GRA); AML/CFT expectations are set by MAS in the financial services provider and payment service provider sectors related to gambling activity.

The Anti-Money Laundering and Other Matters Act 2024 reduced the customer due diligence threshold for casino operators by one-fourth, to SGD 4,000 per single cash transaction or deposit.

The GRA has been granted the authority to implement requirements intended to respond to proliferation financing risks. Indicative of a shift is the changing of optional consideration into mandatory, built into the framework, as per the updated AML/CFT Notices of the MAS, which will become effective in July 2025.

MAS has indicated its enforcement priorities in 2025-26 with a strong focus on taking action against institutions that have not met the expected standards on AML/CFT. This will include a particular focus on assessing customer risk, verifying sources of wealth, and closely tracking financial activity.

Payment service providers involved in gambling transactions have seen the June 2025 penalty round reinforce the notion that inadequate due diligence and poor wire transfer control can create substantial financial repercussions.

Where Global Regulatory Pressure Converges

The new FATF guidance on DNFBPs, the expectations regarding the cross-border operators imposed by the EU AML directives, and the impact of the updated guidance on the existing procedures are discussed. To summarize the key requirements, focus on the following: real-time monitoring, continuous customer risk profiling, and comprehensive transaction tracking. In both cases, the UK Gambling Commission (UKGC) and the Monetary Authority of Singapore (MAS) are actively enforcing these rules as part of their supervisory functions.

The sanctions lists keep evolving rapidly, which continues to pose challenges for organizations with an international presence. With over 215 domestic and international sanction regimes currently in effect, batch screening cycles may result in missing coverage of exposures. If a customer is sanctioned mid-month and continues to process payments without triggering a re-screen, it results in a documented regulatory failure in both jurisdictions.

Screening Gaps That Put Operators At Risk

Enforcement cases across both jurisdictions reveal recurring shortcomings in how screening systems operate in practice. Three recurring gaps appear across both UKGC and MAS enforcement findings.

PEP Screening Gaps

When PEP screening is conducted that includes senior government officials but omits middle-level government officials, mayors, provincial appointments, and local government positions, an exploitable blind spot results. FATF Recommendation 12 mandates that risk-based due diligence on domestic PEPs be performed, a category that regulators in both jurisdictions are now closely looking at.

Adverse Media Monitoring Failures

The periodic negative media tests fail to reflect the risk that may arise between the review cycles. An active exposure window is a customer exposed to negative financial crime reporting in the middle of the month and who is not flagged until the next scheduled check.

Alert Overload Reduces Investigation Quality

When most screening notifications are false positives, the capacity to analyze shifts towards actual risk analysis rather than alert discarding. The outcome is faster alert clearance at lower detection quality, which is exactly what regulators have in mind when they talk about the problem of over-reliance on algorithms.

Building A Unified AML Gambling Screening Workflow

To achieve the UKGC and MAS expectations in 2026, a single workflow must be implemented to connect onboarding, monitoring, and risk evaluation. Operators offering services to customers in the UK and Singapore are not able to employ different screening procedures in each market. This would probably lead to discrepancies that the regulators would identify once they conduct their analysis.

Transaction monitoring should be tuned to gambling-specific trends, rather than to generic financial crime principles. The detection logic built for banking does not identify structured deposits below reporting thresholds, third-party-funded accounts, or rapid cash-out sequences. The typologies that recur in both UKGC and MAS enforcement findings necessitate rules that reflect how layering actually operates in a gambling context.

The constant surveillance will address the time lag associated with the periodic screening process. Sanctions lists, PEP status change, and adverse media alerts should automatically feed into customer risk profiles. Consequently, this demonstrates how much regulatory pressure operators will now be expected to react to.

Audit readiness follows from each of the above. All 13 UKGC enforcement actions in 2025 included requirements for third-party audits. Regulators expect complete documentation of screening decisions, alert dispositions, and investigation rationale, traceable without reconstructing manual records after the fact.

Compliance in 2026 Demands More Than A Screening Checkbox

Gambling operators active in both the UK and Singapore markets face converging regulatory expectations that fragmented screening controls are not capable of meeting. The UKGC’s enforcement is speeding up, and the MAS’s response to major financial crime cases reflects sustained regulatory pressure that operators must adapt to.

Compliance officers are still running annual risk assessments while using high-threshold sources of funds triggers or depending on scheduled adverse media reviews. They are carrying visibility gaps that regulators have already started documenting in enforcement records.

How AML Watcher Supports Gaming Compliance Teams

Fragmented screening systems continue to erode transparency for gambling operators serving customers across multiple regulated environments. This leads to slower risk detection, weaker customer assessment, and higher regulatory exposure.

AML Watcher supports gaming compliance teams with unified sanctions screening, PEP identification, and adverse media monitoring designed for real-time risk detection. Its coverage across global watchlists, as well as its risk classifications, enable consistent compliance with UKGC and MAS expectations without duplicating workflows.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries