Public-Private Partnerships in AML: A Guide to Information Sharing

Others

July 9, 2026

- Financial Crime Has Outgrown the Single-Institution Playbook

- What Are Public-Private Partnerships in AML?

- How Public-Private Partnerships Work

- Different Models of AML Information Sharing Around the World

- Regulators Are Mandating Faster AML Information Sharing

- Why Traditional SAR Reporting Is No Longer Enough

- Where AML Collaboration Breaks Down in Practice

- What Makes Public-Private Partnerships Successful?

- How Financial Institutions Can Prepare for Effective AML Information Sharing?

- What Financial Institutions Should Do Next

- How AML Watcher Supports Better Information Sharing

A single bank rarely sees the whole crime. A mule account opens at Bank A, moves funds to Bank B within hours, then routes through a crypto exchange before anyone files a Suspicious Activity Report. By the time one institution’s alert reaches an investigator, the network has already moved on.

This is the operational reality driving a growing international focus on AML information sharing, and it is reshaping what regulators expect from compliance programs in 2026.

Financial Crime Has Outgrown the Single-Institution Playbook

Criminal networks operate across banks and payment service providers, as well as fintechs, and borders as a matter of design, not accident. A romance scam or pig-butchering scheme often impacts multiple institutions, with each one holding only a fragment of the overall story.

Recent enforcement actions reveal how large these networks have become. In October 2025, the US Department of Justice revealed that it had seized approximately $15 billion in Bitcoin linked to a forced-labor scam network. This action was accompanied by sanctions targeting the group’s money-laundering operations, which had funneled over $4 billion in illegal funds over a 3.5-year period. No institution flagged that on its own. It took financial intelligence sharing across banks, exchanges, and law enforcement to reconstruct the network.

This explains why AML information sharing has become a regulatory priority. A compliance team whose data, customer cohort, and SARs experience is different from the other team’s is being attacked by an enemy with whom they are only partially in touch. Financial crime information sharing fills that visibility gap by allowing institutions to share their experiences with the same typologies, entities, or behaviors, eliminating the risk of losses stacking.

What Are Public-Private Partnerships in AML?

A public-private partnership in anti-money laundering creates a way for financial intelligence units, regulators, and law enforcement to share information with banks, fintech companies, payment providers, and crypto exchanges. The collaboration operates within clearly defined legal boundaries, expanding on the traditional process in which Suspicious Activity Reports vanish into filing systems that create a more efficient and well-organized communication of essential risk information.

Public sector participants typically include the national FIU, the primary financial regulator, and law enforcement agencies with financial crime mandates. Private sector participants range from large retail banks to remittance providers, gambling operators, alongside VASPs, depending on which sectors a jurisdiction’s PPP covers.

Instead of investigating individual cases, PPPs enable their participants to create a common picture of the financial crime landscape without violating legal and regulatory obligations.

How Public-Private Partnerships Work

Most PPP schemes are implemented in a similar way, although this varies from jurisdiction to jurisdiction.

- Detection: An institution’s monitoring systems flag unusual activity.

- In an internal investigation: The institution’s analysts assess whether the activity meets the threshold for external sharing.

- Information sharing: the finding moves through an approved mechanism (a task force, a legislated platform, a secure portal) to other participating institutions or to the FIU.

- Cross-institution comparison: other participants check the shared indicators against their own customer and transaction data.

- FIU coordination: the FIU consolidates observations into actionable or tactical intelligence products.

- Law enforcement action: When appropriate, investigators take action based on the cohesive picture.

- Feedback into monitoring: participants make changes to their detection rules based on what the partnership brings up.

Three types of intelligence typically circulate within this framework.

- Strategic intelligence encompasses broad trends, such as emerging mule-account patterns and new methods for crypto off-ramps.

- Tactical intelligence is more focused, targeting identified entities, accounts, or transaction chains under suspicion.

- Operational intelligence supports real-time investigations, often involving tighter access permissions with a tightly controlled timeframe for action.

Understanding which category a piece of information belongs to is important because it dictates who may see it and under what circumstances; swiftly, processing deadlines become more urgent.

Different Models of AML Information Sharing Around the World

Jurisdictions have built PPPs around different regulatory frameworks and operating models, but they all require organizations to adopt different approaches.

Australia’s Fintel Alliance illustrates the scale this can reach. By the end of 2024, the partnership had aggregated over 50 million cash-deposit records from the nation’s four largest banks. Within just a few days, they uncovered criminal activity that one organization alone could never have detected in its own data.

Regulators Are Mandating Faster AML Information Sharing

Public-private partnerships in AML have moved from best practice to explicit regulatory expectation over the past year.

FATF approved a new Global Overview of Public-Private Partnerships at its June 2026 Plenary, framing structured PPP models as necessary for lawful data exchange between banks and jurisdictions; FATF Recommendations 13, 14, 16, 29, and 40 already require various forms of cross-institution and cross-border cooperation. FinCEN’s June 12, 2026, update to its Section 314(b) guidance confirmed that the safe harbor for voluntary information sharing between US financial institutions extends to fraud, including pig-butchering schemes, romance scams, and mule account activity, not only confirming money laundering, and it explicitly encourages sharing “in real time.” Singapore’s MAS operates COSMIC under dedicated legislation, with direct access for the country’s Suspicious Transaction Office, while the EU’s Anti-Money Laundering Authority (AMLA), established under the bloc’s 6AMLD framework, is extending coordinated supervision and cross-border data exchange requirements across member states.

Across jurisdictions, regulators are encouraging faster and broader information sharing that extends beyond traditional SAR reporting.

Why Traditional SAR Reporting Is No Longer Enough

Traditional SAR reporting follows a largely one-way process. An institution detects activity, files a Suspicious Activity Report, and the SAR disappears into an FIU’s queue for eventual investigation, often weeks or months later, with no feedback loop back to the filer.

Public-private partnerships complement this process by enabling structured collaboration between institutions, FIUs, and law enforcement. Compared with traditional reporting, they improve detection speed, provide richer investigative context, and help connect related activity across multiple institutions.

Public-private partnerships complement rather than replace SAR obligations by adding a collaborative intelligence layer to traditional reporting. Understanding the distinction between public-private sharing and private-private sharing is important in this context. The Section 314(b) framework established by FinCEN serves as a private-private mechanism that allows institutions to collaborate on investigations across various organizations under a safe harbor arrangement. This is separate from the public-private channels that involve an FIU or task force.

Where AML Collaboration Breaks Down in Practice

Institutions are still struggling with operating problems despite increasing regulatory support.

Poor-Quality SARs Reduce the Value of Shared Intelligence

Regulators have historically rewarded over-reporting to avoid liability, which floods financial intelligence units with low-value filings. Research from the Future of Financial Intelligence Sharing program found that 85-95% of private-sector financial crime leaders disagreed that the current Suspicious Activity Reporting framework leads to effective crime discovery and disruption.

Unclear Information-Sharing Rules Delay Investigations

Compliance teams often misread the scope of what they’re permitted to share, or default to caution because approval processes are slow. FinCEN’s own June 2026 guidance was issued specifically to correct a widespread misunderstanding that 314(b) covered only money laundering, not fraud.

Inconsistent Data Standards Prevent Effective Intelligence Matching

Different institutions run different case management systems, use inconsistent entity identifiers, and match names against watchlists with varying levels of accuracy. Two institutions can hold data on the same suspect entity and fail to recognize the overlap simply because their systems format names or identifiers differently.

Cross-Border Privacy and Compliance Rules Limit Information Sharing

GDPR-style data protection rules, bank secrecy provisions, and data localization requirements pull in different directions from the expectation of broader information exchange, and few institutions have clear internal protocols for what can move across borders without additional consent.

Poor Data Quality Weakens External Collaboration

An institution that can’t unify its own PEP, sanctions, watchlist, and adverse media signals internally has little useful intelligence to contribute to a partnership. Across the industry, approximately 90% of AML alerts are false, or “noise,” which can overwhelm the real signal a partnership is aiming to detect.

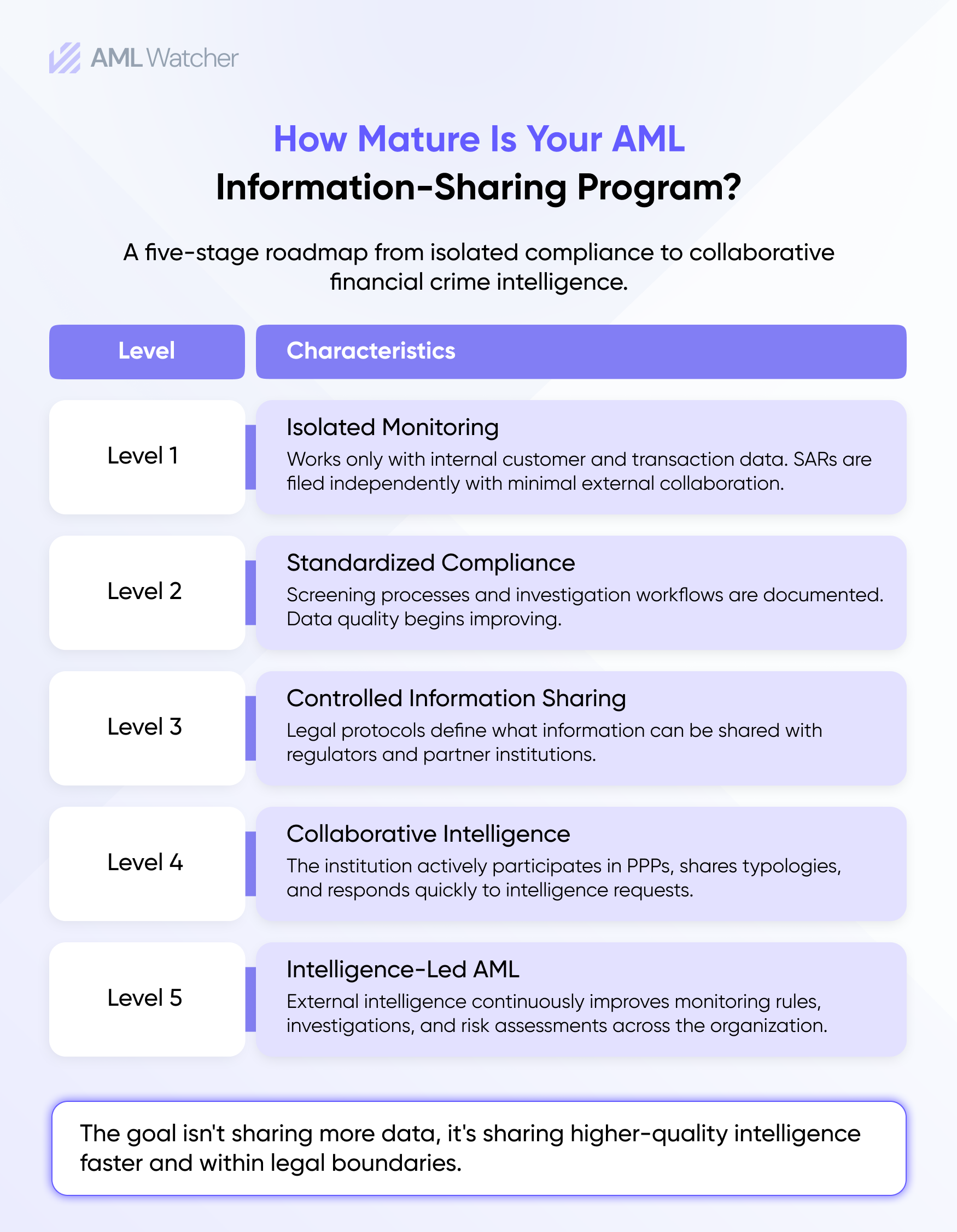

What Makes Public-Private Partnerships Successful?

There are legal reasons to exchange information, but there are also other characteristics that make public-private partnerships successful. Governance structures are mechanisms that determine who has access to shared intelligence and how long they have, whereas legal agreements are those that define how, and how not, that shared intelligence can be used. When there is trust between participants and trust that grows from a sustained series of engagements, institutions are willing to share with one another intelligence that is useful to them, not just the amount they are legally obligated to share. Common terminology helps participants interpret typologies consistently, and regular feedback from financial intelligence units ensures institutions understand how shared intelligence supports investigations and continue contributing high-quality information.

How Financial Institutions Can Prepare for Effective AML Information Sharing?

Participating effectively in a public-private partnership also requires strong internal capabilities. Financial institutions should focus on:

- High-quality screening: Accurate sanctions, PEP, watchlist, and adverse media screening prevent institutions from reporting false intelligence.

- Fast investigation turnaround: Receiving information through partnership is meaningless if there is no timely evaluation, resolution, and documentation of decisions.

- Accurate entity resolution: Institutions must be able to correctly match customers and entities in different data sets, even when names are misspelled or identifiers are incomplete.

- Consistent customer data: Shared intelligence becomes easier to search, match, and investigate because of standardized, well-structured data.

What Financial Institutions Should Do Next

Considering current regulatory expectations, compliance teams have a reasonably clear checklist:

- Review current information-sharing policies against FinCEN’s expanded 314(b) guidance or the equivalent framework in your jurisdiction

- Understand which local PPP initiatives your institution is eligible to join, JMLIT, Fintel Alliance, FEC, or a national equivalent

- Audit internal data quality before joining external partnerships.

- Train investigators on what can legally be shared, particularly the distinction between sharing the facts underlying a SAR versus revealing the SAR itself.

- Update screening systems to minimize false-positive alerts which currently swamp genuine alerts.

- Documented governance and approval processes to avoid undue delays in sharing information.

How AML Watcher Supports Better Information Sharing

Effective AML information sharing depends on accurate screening and reliable customer intelligence. Poor data quality and excessive false positives reduce the value of every partnership.

AML Watcher helps financial institutions improve the quality of the intelligence they contribute to collaborative AML efforts. By utilizing comprehensive sanctions, enhanced PEP and watchlist monitoring, along with adverse media screening, compliance teams can quickly pinpoint genuine risks. This approach not only streamlines the process by minimizing unnecessary manual reviews but also supports investigation decisions with trustworthy, auditable data.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries