KYC and AML: Understanding the Key Differences and Best Practices

AML/CFT

March 29, 2025

- How Does Know Your Customer (KYC) Work?

- Limitations of Manual AML Risk Assessment

- Role of Initial KYC and AML in Ascertaining Level of Customer Due Diligence

- Challenges in Implementing AML & KYC Regulations

- What Kind of AML Compliance RegTech compliments a KYC Software?

- How AML Watcher Can Help In AML Compliance

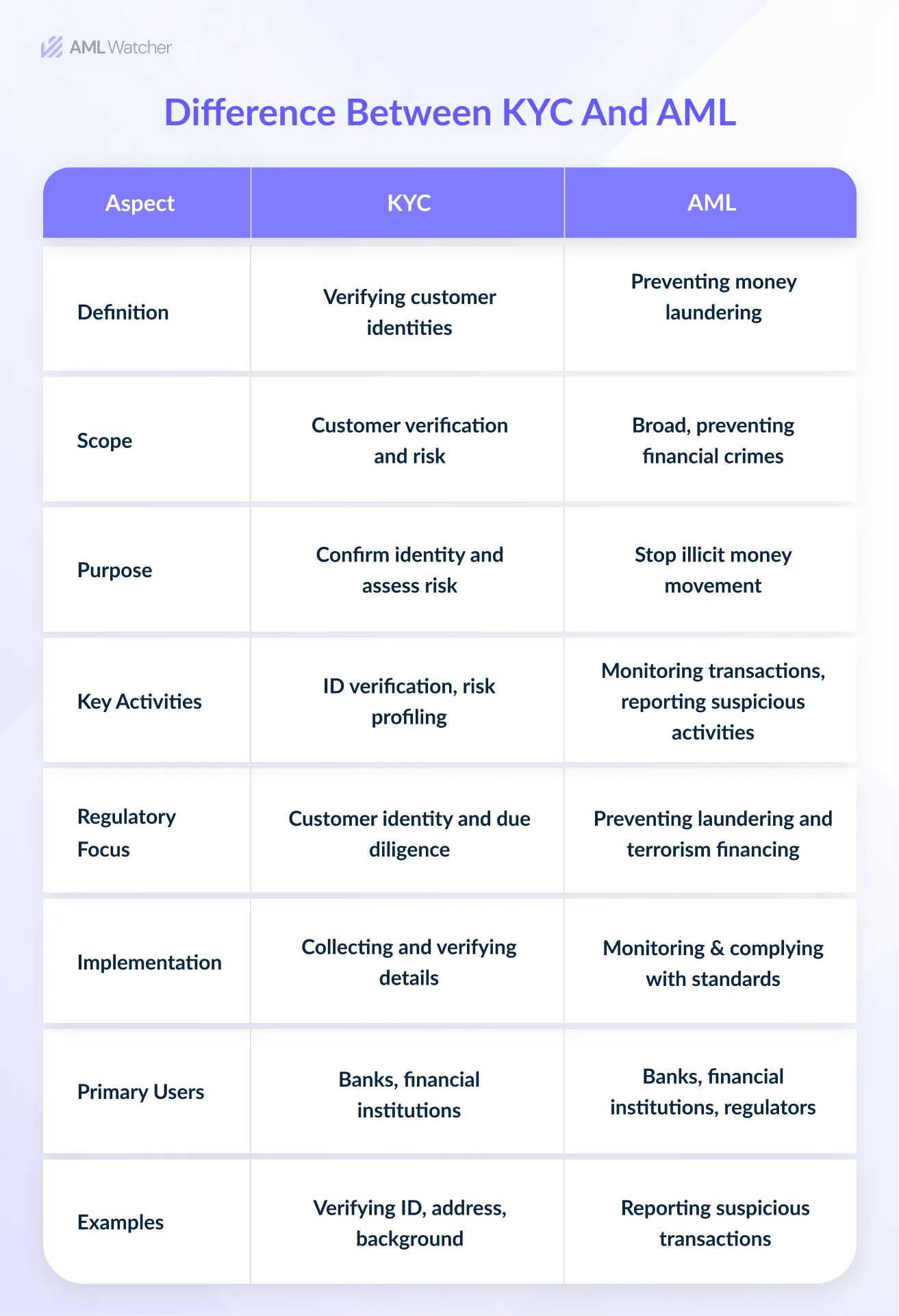

KYC and AML are commonly used terms in the AML Compliance industry. KYC Know Your Customer and AML Anti-Money Laundering Processes are very closely linked to each other.

While KYC is performed to ensure compliance with AML, there are minor distinctions between the two in the RegTech space.

The difference between KYC and AML is termed as KYC is part of the broader process of AML. The former is often used in the context of customer identification, and the latter is often used in the context of assessing a customer’s risk of association with any money laundering, terrorist financing, and other illicit activity.

Understanding this distinction between KYC and AML and the association of the two processes is essential to comply with global and jurisdiction-specific anti–anti-money laundering compliance laws and to prevent penalties and reputational damage due to non-compliance.

AML measures are a series of procedures and regulations adopted by Financial and Designated Non-Financial Businesses and Professions (DNFBPs) to comply with AML Laws.

How Does Know Your Customer (KYC) Work?

The Know Your Customer process involves collecting government-issued identity documents (like a passport or national ID) and confirming the identity by verifying additional relevant information, including residence address, tax documents, utility bills, and additional business documents in case the client is a legal entity.

In the case of remote KYC, identity document verification is accompanied by photo ID matching and liveness detection.

Financial institutions must conduct a Know Your Customer (KYC) process before onboarding a client to ensure accurate risk assessment for possible association with any illicit activity.

This helps the obligated sectors not only in accurate identification of customers’ identities in line with the Customer Identification Program but also with AML risk assessment.

Additionally, jurisdiction-specific regulations help assess the money laundering and terrorist financing risks associated with the client.

Below are the steps for conducting KYC, inclusive of AML.

- Verify clients’ identities to ensure AML compliance and prevent fraud

- Screen clients and employees against sanctions, PEP, and other Watchlists.

- Ongoing monitoring to check the change in risk status of a customer

- Constant transaction monitoring allows businesses to assess Suspicious activities associated with clients.

If suspicious activity is detected and flagged, further measures such as filing an SAR with relevant authorities for further investigation are taken.

Limitations of Manual AML Risk Assessment

Manually finding authentic information to asses the risk associated with a customer from different sources, such as social networks, search engines, or public databases, is a time-consuming process.

This is particularly difficult for big financial institutions, FinTechs, and companies with global reach and global trading partners. Such businesses not only need to comply with the local laws but also with anti-money laundering laws.

Due to the diverse nature and size of the global customers, using the manual screening processes for them is inefficient, and hence, they have to adopt the automation.

An optimal AML data screening solution should not only reduce resource time but also offer context-driven sanctions and AML screening.

This involves enhanced labelling of sanctions and risk statuses, aligned with the organization’s compliance program and local regulations. Such an approach ensures more accurate and efficient risk assessments.

Use the Best Regtech for AML Risk Screening that automates and streamlines multiple compliance procedures like KYC to improve accuracy, reduce errors, and increase efficiency.

Consequences of AML KYC Non-Compliance

AML KYC compliance is essential to mitigate financial risks and prevent illicit activities such as fraud. Following are the repercussions of Noncompliance with AML and KYC.

- Hefty fines are imposed for violating AML regulations and laws.

- Businesses may face sanctions or license suspensions.

- An individual may face legal actions such as imprisonment for years

- Violations cause reputational damage to the institution.

- Businesses can also lose potential clients.

Role of Initial KYC and AML in Ascertaining Level of Customer Due Diligence

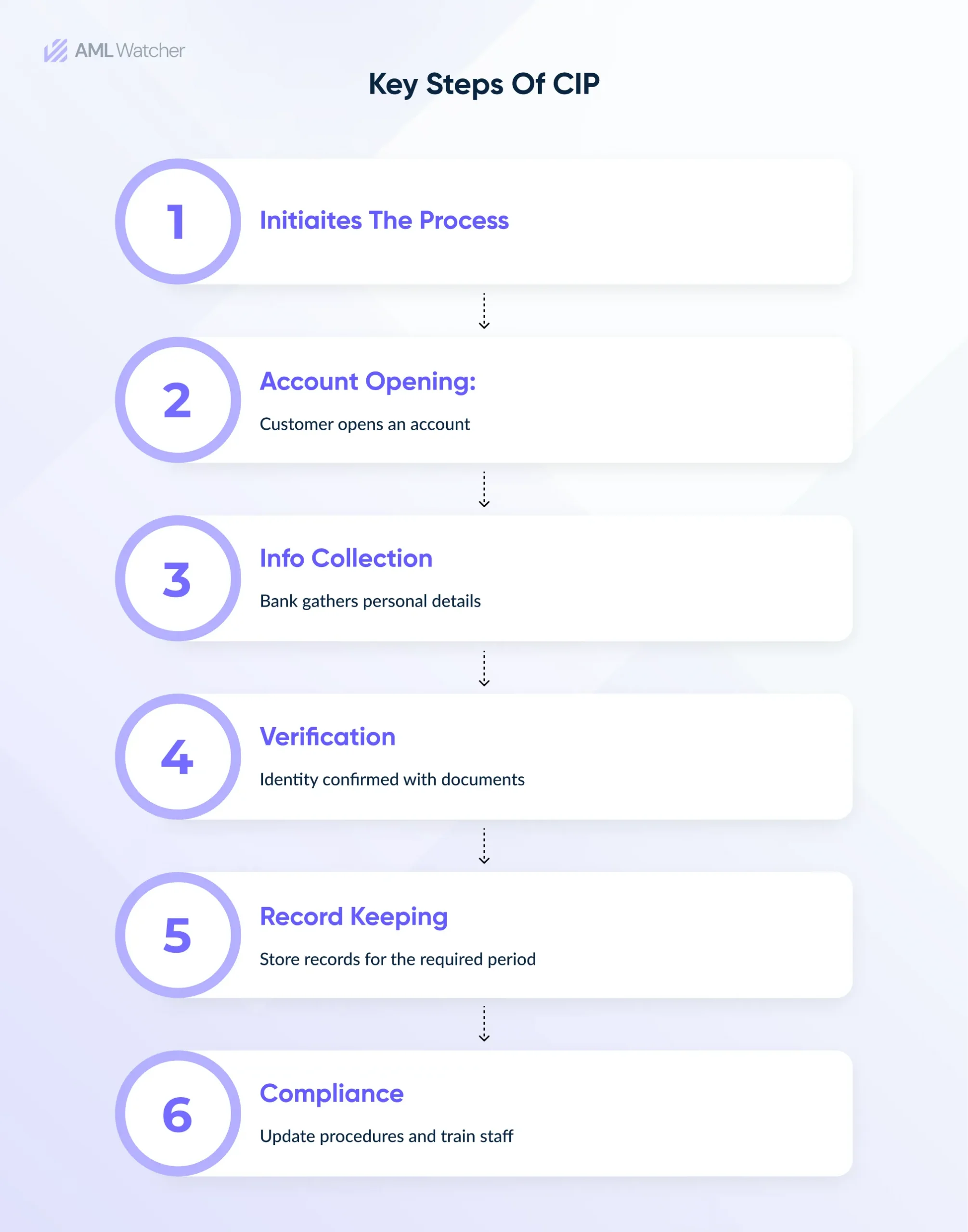

Customer Identification Program (CIP)

The Customer Identification Program (CIP) was established after the September 11 attacks and under the USA Patriot Act in 2001 to prevent financial crimes.

Clients’ Identities are verified using their name, date of birth, address, social security number, or other documents.

Per the USA Patriot Act, all banks must implement written CIPs according to the bank’s size and customer base. It mandates banks to impose CIPS into their AML policies as well.

Customer Due Diligence (CDD) and Enhanced Due Diligence (EDD)

The second main component of KYC is Customer Due Diligence (CDD). It is the process of verifying a client’s identity and assessing potential risks for money laundering or terrorism financing. It ensures compliance and protects businesses from financial crimes.

After the identity verification part is completed, an Anti-money laundering risk assessment is done to ascertain the accurate level of risk associated with a customer

Enhanced Due Diligence (EDD) is performed on clients with higher risk. Additional information is required for higher-risk clients. Regular transaction monitoring is mandatory in EDD.

The transaction pattern is monitored regularly so that if it deviates from the regular pattern, it requires further investigation to detect any suspicious activity.

Evaluation of the risk profile of clients is necessary in financial organisation to asses whether a person requires a simple due diligence or enhanced due diligence.

Ongoing Monitoring To Check Changing Risk Status

Checking the client’s transaction or sanction status at one time is not enough. Continuous Ongoing Monitoring is needed to ensure proper security.

Continuous monitoring of the activity of the client’s accounts allows obligated sectors to find irregularities early and mitigate risks.

A customer’s risk status may not remain the same. For instance, after elections, a customer may become a Politically Exposed Person (PEP), or a low-risk PEP could transition to a high-risk PEP.

Additionally, a customer’s name could be added to lists such as Specially Designated Nationals (SDN) or any other local or international sanctions list. Similarly, a customer may be subject to some investigation related to a predicate offense and have their name in any warning or regulatory enforcements.

Challenges in Implementing AML & KYC Regulations

Financial organizations and businesses face challenges in complying with KYC AML regulations. Challenges like quality data access and evolving regulatory landscapes need reliable solutions for risk mitigation and the implementation of robust KYC AML compliance.

The following are possible challenges:

- Manual risk assessment of customer profiles can slow down the process and cause errors.

- Too many false positive alarms in AML Risk Assessment can overwhelm the teams and waste time and resources.

- Ever-changing KYC and AML regulations in response to advanced threats and changes in geopolitics require obligated sectors to be dynamic.

- Businesses can have dynamic due diligence needs that may not be limited to Anti-Money Laundering compliance, e.g, doing supply chain due diligence for global partners.

- Limited staff and budget create hurdles in risk management.

What Kind of AML Compliance RegTech compliments a KYC Software?

When integrating an AML solution with KYC software, it is essential to rely on AML compliance tools that can support the dynamic nature of customer risk assessment.

The following are key features that AML tools should offer to complement KYC solutions:

- AML tools should provide real-time updates on customer risk profiles, ensuring that the data used for KYC processes is always current. This helps in identifying any changes in customers’ AML risk status due to evolving regulations or emerging risks.

- The AML tool should aggregate data from a wide range of trusted sources, including sanctions lists, PEP databases, adverse media sources, and global watchlists. This helps KYC providers assess the customer’s true risk assessment and background, reducing the risk of AML Non-Compliance and making them take a proactive approach.

- KYC/AML products should leverage data curated by expert researchers, enabling businesses to rely on accurate, verified information for comprehensive customer risk assessment..

- Real-time updates in AML tools inform continuous monitoring of clients’ activities, ensuring any unusual behavior or red flags are flagged promptly, facilitating proactive risk assessment.

- Ongoing monitoring of adverse media sources continuously screens profiles, providing updated risk assessments and enhancing decision-making.

- A strong AML solution must cater to global regulatory requirements, ensuring compliance with regional and international AML standards for diverse client data.

Big banks can ensure more accurate, real-time risk assessments, mitigate financial crime, and maintain strong compliance frameworks by choosing a KYC solution that has advanced AML screening technology.

How AML Watcher Can Help In AML Compliance

AML Watcher provides a comprehensive suite of features designed to enhance your AML/CFT compliance efforts:

- Access to over 3,500+ global watchlists for comprehensive and accurate AML screening.

- Coverage of more than 230 sanction regimes to ensure adherence to global financial sanctions.

- Access to over 2.6 million+ Politically Exposed Person (PEP) profiles to mitigate high-risk exposures.Integration with over 50,000 negative media sources to find risks from a range of local media sources.

- Evaluation against 400+ risk categories to provide a more granular and tailored risk assessment for your business.

- Continuous updates from these extensive data sources ensure you have the most up-to-date risk information for AML compliance.

- Ability to screen entities against a wide array of global sanctions, PEPs, and adverse media to ensure global regulatory coverage.

- Improved risk detection with a wide variety of data sources, reducing any gaps in AML compliance.

- Real-time screening and filtering to identify high-risk individuals, ensuring effective AML risk mitigation.

- Customizable risk assessment to give high-risk transactions and organizations priority for more targeted AML compliance initiatives.

Move Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries