Managing AML Risks in Correspondent Banking Without De-Risking

Anti Money Laundering

September 15, 2025

Correspondent Banking is truly a cornerstone for international financial transactions. Simply put, smaller, less connected financial institutions can access foreign markets, currencies, and services through a correspondent bank in another country. Essentially, then, the rationale of correspondent banking is to remove the hurdles smaller financial institutions face in accessing international markets.

However, while correspondent banking is a crucial part of the global financial system, the complex nature of such banking carries with it a high risk of money laundering. From opaque transaction chains coupled with subpar due diligence to the frequent use of shell companies to hide illicit funds, financial institutions can no longer afford to engage in correspondent banking without a robust AML solution system.

What is Correspondent Banking?

The very existence of global commerce relies on a vast financial network. The correspondent banking system lies at the core of this global financial network.

But what is a correspondent bank?

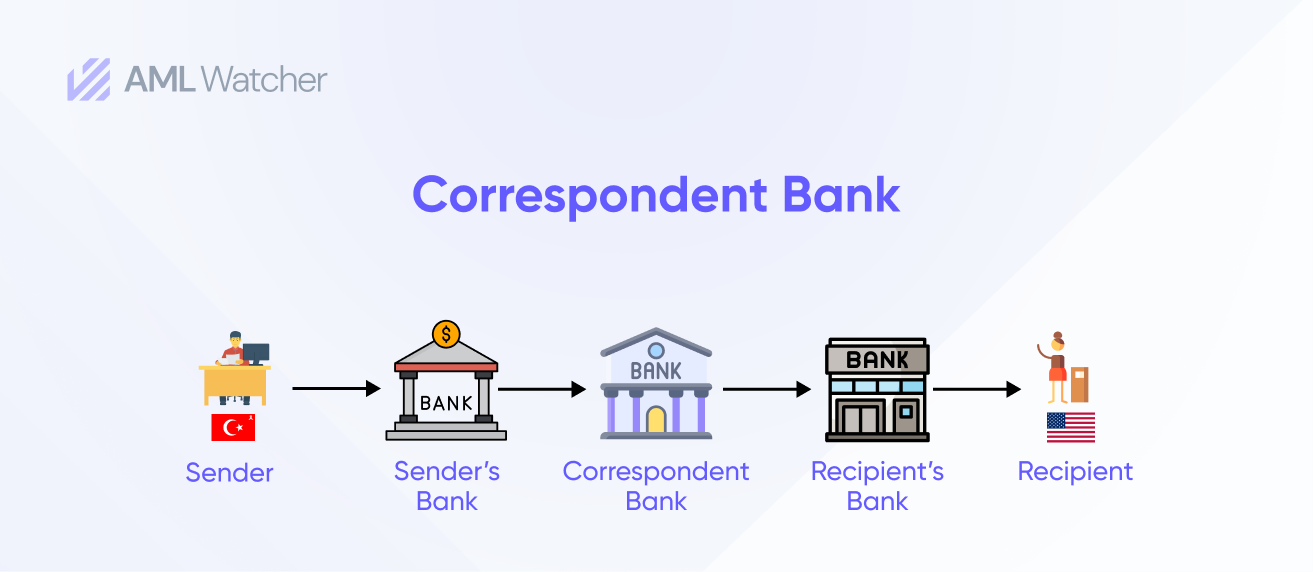

It is where one bank (the correspondent) provides services to another bank (the respondent) to process a cross-border transaction, settle payments, or even access foreign currencies.

In practical terms, picture correspondent banks as intermediaries that act on behalf of domestic or regional banks, allowing them access to the international financial system. To give a typical correspondent banking example, the Philippine National Bank (PNB) has a correspondent banking relationship with JPMorgan Chase, enabling PNB to facilitate U.S dollar-denominated transactions through the correspondent bank (JPMorgan Chase) for its customers without them having direct access to the U.S financial system.

For Filipino nationals, then, this feature of banking allows them to make wire transfers and invest in programs in the U.S, with their national bank account in the Philippines.

While correspondent banking is essential for international financial activity, bad actors exploit this structure for money laundering activities.

Hidden Correspondent Banking AML Risks

By using the same services that enable locals to access the international market through correspondent banking, financial criminals use this process to transfer illicit funds across the global banking network. Financial criminals particularly target the complex nature of correspondent banking agreements to obscure the source and ownership of dubious funds.

- Opaque Payment Chains:

One of the primary AML vulnerabilities in correspondent banking transactions is the opacity of payment chains. The originating customer, the final beneficiary, and even the true purpose of the transfer can be obscured, especially when multiple correspondents are involved. This vagueness creates blind spots for AML compliance teams, rendering it difficult for traditional AML solution systems to track the movement of illicit funds.

The European Central Bank (ECB) reported that roughly $746 billion worth of daily transactions channeled through correspondent banking arrangements within Eurozone countries alone in 2019.

-

Inadequate fraud detection monitoring tools:

While correspondent banks may perform basic due diligence on their direct clients (the respondent banks), they cannot effectively monitor the full range of transactions or scrutinize indirect relationships. Traditional AML solution systems are not equipped with modern fraud detection tools that provide a comprehensive risk report. This leaves compliance gaps that criminals can exploit, using methods like layering or smurfing to disguise illicit transactions.

-

Complex Money-Laundering Techniques in Cross-Border Transfers:

Money launderers frequently exploit correspondent banking to break large sums into smaller, structured payments (a process known as smurfing), moving them across jurisdictions, and reassembling them later. Additionally, this layered movement is difficult to track in high-volume corridors.

-

De-Risking and Its Dangerous Consequences:

In response to AML pressure from regulators, many financial institutions have adopted “de-risking” strategies, cutting off entire categories of respondent banks deemed high-risk (e.g., in certain African or Caribbean countries). While this may protect the correspondent bank from regulatory penalties, it also forces legitimate transactions into less-regulated or informal financial systems, creating systemic risks. This trend runs counter to FATF’s Correspondent Banking guidance, which strongly encourages financial institutions to adopt a risk-based approach, not a blanket exclusion.

How AML Gaps Lead to De-Risking in Correspondent Banking

In 2014, BNP Paribas, one of the world’s largest banks, was hit with an $8.9 billion fine by U.S. authorities for violating sanctions related to Iran, Sudan, and Cuba.

The investigation revealed that BNP Paribas, as a correspondent bank, facilitated illegal transactions through its relationships with foreign banks in Sudan, Cuba, and Iran. Processing billions of dollars in trades for countries under U.S. sanctions, the bank’s AML systems failed to detect and subsequently prevent money laundering. Allowing sanctioned transactions to flow through its correspondent banking network. Despite the size and prominence of BNP Paribas, its lack of stringent controls allowed these illicit funds to flow unchecked.

“The [BNP] penalty led to a sharp reassessment of the costs of financial crime compliance among correspondent banks – both with respect to the required level of due diligence and expected fines – and contributed to the withdrawal of correspondent banks from countries with a high risk of financial crime.”

Borchert, L., de Haas, R., Kirschenmann, K., & Schultz, A. (2021)

How the withdrawal of global correspondent banks hurts emerging Europe

The BNP Paribas case was a seminal moment in the AML landscape. The case highlighted multiple correspondent banking AML red flags. It demonstrated that even the largest banks were vulnerable to being caught up in illicit activity if their correspondent banking controls were insufficient.

In the aftermath of the BNP fine, correspondent banks reassessed their monitoring systems, especially regarding compliance with U.S. sanctions and broader AML regulations. The case was an essential reminder that AML risks in correspondent banking are not only a concern for the respondent banks but also for the correspondent banks that provide access to global financial markets.

In an effort to avoid the regulatory penalties imposed on BNP Paribas, many global financial institutions invested in advanced monitoring tools and real-time alert systems to strengthen their correspondent banking protocols.

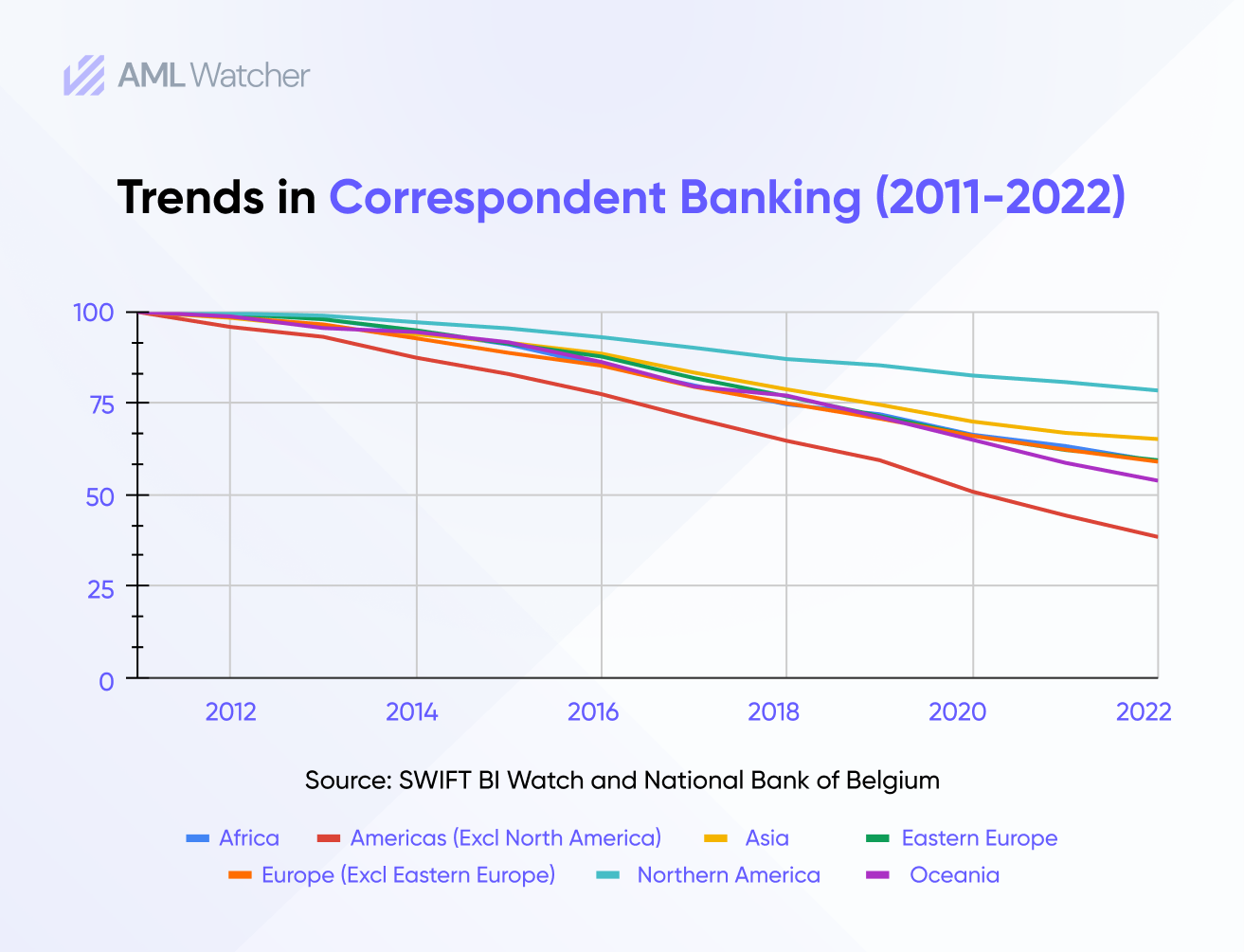

The graph above clearly illustrates the significant decline in correspondent banking relationships since 2011, primarily driven by mounting compliance costs and the increased regulatory scrutiny following high-profile fines, such as the BNP Paribas penalty. As institutions faced escalating costs related to compliance, coupled with the potential reputational stain, many banks opted to reduce their exposure by severing correspondent relationships.

Consequently, these de-risking policies had an adverse effect on the global economic network, limiting access to banking services in high-risk regions while pushing suspicious transactions into less regulated channels.

However, the financial institutions that do still actively participate in correspondent banking adopt stringent AML compliance measures to ensure bad financial actors cannot launder money through correspondent banking.

Guidelines of the FATF on Correspondent Banking:

FATF Recommendation 13 outlines stringent due diligence measures that financial institutions must follow when establishing or maintaining correspondent banking relationships. In addition to regular customer due diligence (CDD), institutions must:

- Conduct in-depth research about the respondent institution, such as its business nature, reputation, and effectiveness of AML frameworks. Further, a financial institution must also ensure that the respondent bank has not been the subject of an AML/Combating the Financing of Terrorism Compliance (CFT) investigations or action.

- Assess the respondent’s AML/CFT controls to ensure they meet international standards.

- Obtain senior management approval before entering into new correspondent relationships, ensuring accountability at the highest levels.

- Clearly define the responsibilities of both institutions involved in the correspondent relationship, establishing a solid framework for cooperation.

- For payable-through accounts, ensure that the respondent bank has conducted proper CDD on customers with direct access to the correspondent bank’s accounts and can provide relevant CDD information when required.

Furthermore, FATF prohibits financial institutions from engaging with or continuing correspondent banking relationships with shell banks, and mandates that institutions verify that their respondents do not allow shell banks to use their accounts.

Fortify Your Correspondent Banking Compliance with AML Watcher

The landscape of correspondent banking has become increasingly complex, with institutions facing mounting compliance costs and regulatory scrutiny. High-profile cases like the $8.9 billion fine against BNP Paribas emphasize the importance of effective AML solution systems. AML Watcher offers a comprehensive solution to tackle these challenges.:

- Real-Time Transaction Screening: Ensure complete visibility of cross-border payments through correspondent banking transaction monitoring by screening payments as they occur. AML Watcher’s system detects hidden risks, sanctions, and PEP links, helping you track illicit funds and reduce opacity in your payment chains. By identifying these illegal financial activities in real time, we provide the tools to intercept them before they breach your network.

- Customizable Transaction Monitoring: AML Watcher offers you the flexibility to adopt custom rules according to your risk profile and exposure, ensuring identification of suspicious activity across multiple spheres of correspondent banking. With over 50,000 predefined rules, our platform can be customized to your institution’s needs, ensuring a robust AML monitoring system in line with FATF’s risk-based approach to managing correspondent banking risks.

- Advanced Fraud Detection: With the power of AI and pattern recognition, AML Watcher spots layering and smurfing techniques used by criminals to disguise illicit transactions.

- Scalability and Flexibility: AML Watcher helps your institution to operate in line with FATF Recommendation 13, ensuring your correspondent banking operations meet global compliance standards. Our system can adapt to your needs, providing enhanced due diligence, senior management approvals, and constant monitoring to prevent financial crime.

- Comprehensive Screening: As de-risking continues to dictate the correspondent banking sector, AML Watcher empowers businesses to assess and manage high-risk correspondent relationships by screening against over 3,500 watchlists, 215+ sanctions regimes, and real-time adverse media monitoring. AML Watcher ensures you can sustain relationships without compromising compliance.

By integrating AML Watcher, financial institutions can strengthen their compliance frameworks to mitigate the risks associated with correspondent banking and money laundering.

Frequently Asked Questions

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries