The Role of Advanced AML Systems in Meeting Global Regulatory Standards

AML Regulations

June 27, 2025

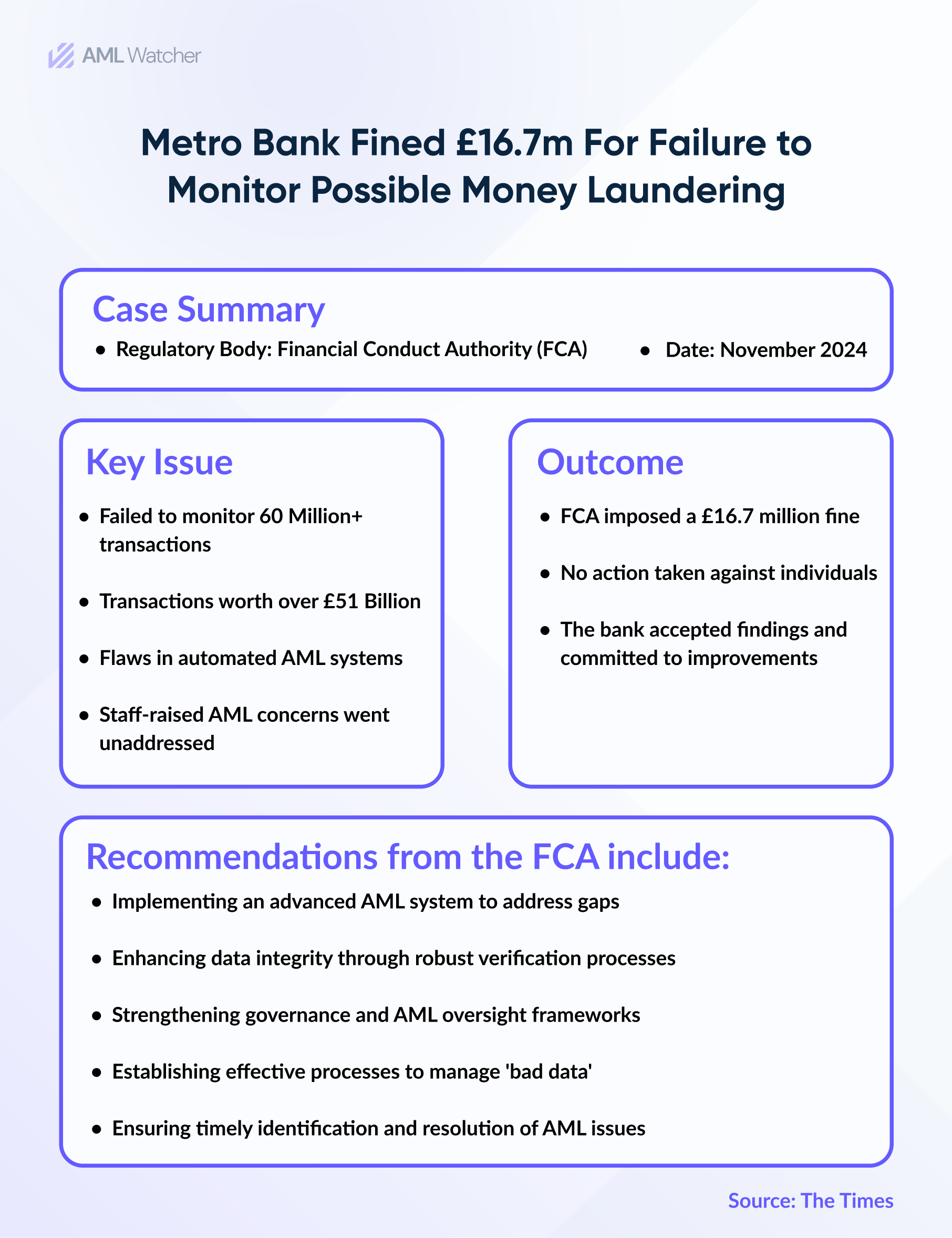

In November 2024, FINMA fined the Swiss bank $5 million due to serious AML and compliance failings in detecting high-risk clients. This Enforcement decision became public on 14 May 2025.

Regulators fined the Swiss bank due to the failure to detect and report suspicious activities from 2009 to 2019. Accounts that were linked to a Russian embezzler and clients from India, involving several branches of the bank.

The case highlights the consequences of inadequate AML systems in businesses, which fail to detect suspicious activities, leading to financial penalties and reputational damage.

Financial institutions, designated non-financial businesses and professions (DNFBPs), or other AML-obligated sectors, must comply with AML/CFT rules and regulations to detect illicit finance routing through their business.

A robust AML System includes multiple elements, starting from planning to implementation and even evaluation.

These elements include the use of automated and advanced AML software for screening and transaction monitoring, a series of internal policies, comprehensive procedures, and staff training.

It helps mitigate financial crime risks and protects businesses and financial institutions from regulatory penalties and reputational damage.

Creating a proper AML System Checklist is essential for ensuring that your business’s AML framework is comprehensive, compliant, and consistently effective.

It helps identify gaps, standardize procedures, and align your systems with regulatory expectations, minimizing risk and reinforcing operational integrity.

How AML Software Anchors Risk-Based and Regulatory Compliance?

AML software is a core element of any organization’s AML Compliance program. AML software enables customer risk assessment and the early detection and prevention of suspicious activities, ensuring AML/CFT compliance.

Usually, regulators require financial institutions and businesses to follow a risk-based approach in AML Compliance. A robust AML Software helps businesses comply in line with the risk-based approach.

An AML/CFT system must be designed to screen risks and monitor transactions in line with the organization’s risk appetite. In this way, it works optimally by reducing false positives and minimizing the workload.

Regulatory bodies, such as the Financial Action Task Force (FATF) and the Financial Conduct Authority (UK), mandate that AML-obligated entities must implement measures, including Customer Due Diligence (CDD) and AML screening, which involves checks for Politically Exposed Persons (PEPs), sanctions, and adverse media, particularly when dealing with high-risk clients.

Additionally, transaction monitoring and ongoing monitoring are required to detect and report suspicious activities.

Significance of AML Software

Businesses operate internationally to upscale their financial growth. Companies interact with diverse clients and deliver their services on a global stage. Exposure to financial crimes in such cases is higher, thus leading to increased regulatory scrutiny by governments.

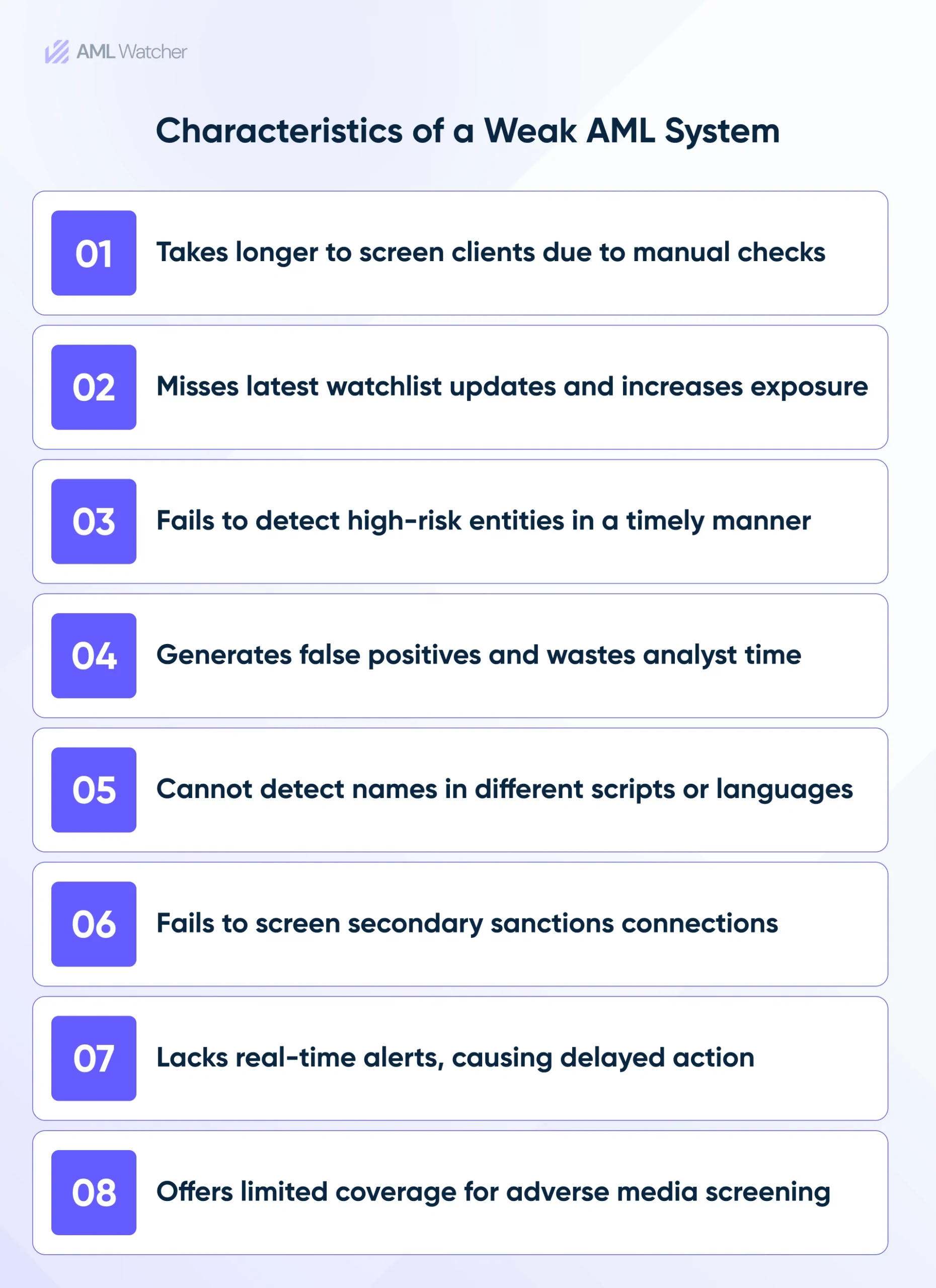

As criminals employ sophisticated methods to launder money and conceal the source of funds, compliance teams can’t rely on outdated or manual AML software in this modern era.

A contemporary, well-integrated, automated AML software allows regulated entities to seamlessly comply with AML/CFT regulations in line with the risk exposure.

An AML screening system helps achieve compliance by facilitating customer due diligence (CDD) and enhanced due diligence (EDD) processes, screening clients against politically exposed person (PEP) databases and sanctions lists.

Through additional features, such as checking against watchlists and regulatory enforcement, adverse media screening, and ongoing monitoring, it enables financial institutions to assess high-risk clients based on their association with predicate offenses and to monitor for changes in risk status.

Furthermore, Real-time detection of suspicious activities through transaction monitoring ensures the timely identification and prevention of potential financial crimes, such as money laundering and terrorist financing.

The Integration of AML Laws, Policies, and Software for Effective Compliance

AML laws and regulatory frameworks worldwide are influenced by the Financial Action Task Force (FATF) recommendations, which aim to mitigate financial crimes, including money laundering and terrorist financing.

These standards guide countries in establishing anti-money laundering (AML) laws, and based on these guidelines, regulators develop AML policies, which are then adopted by financial institutions and entities that are obligated to fulfill the regulatory requirements.

Internal AML policies, as mandated by law, establish the foundation for customer due diligence (CDD) risk assessment, transaction monitoring, AML screening, reporting obligations, and staff training to ensure AML compliance.

These components collectively build an integrated AML system, enabling organizations to identify and mitigate illegal activities proactively.

An AML Verification system that includes identity verification and AML risk assessment as core components, delivering fast and accurate identity checks to support your AML/CFT efforts, is mandatory to optimize the due diligence process.

Effective AML software within the AML system ensures seamless execution, automation, and timely and reliable enforcement of AML compliance.

AML software solutions empower compliance teams by responding quickly to emerging risks as per the business’s risk appetite and remain aligned with evolving AML laws and FATF standards.

AML solutions must incorporate specific key features that align with regular requirements and industry best practices to implement AML policies effectively

Following an AML software checklist, many of which directly align with FATF recommendations, ensure your AML compliance program is efficient and effective.

Core features in the AML Software Checklist

Customer Due Diligence (CDD) and Enhanced Due Diligence (EDD)

An AML software designed in line with FATF Recommendations 9 and 10 helps financial institutions in verifying customers through a customer due diligence process and implement enhanced due diligence on high-risk clients, such as Politically Exposed Persons (PEPs), who may be linked to financial crimes, including money laundering and terrorist financing.

Sanction Screening and PEP Screening

AML software should screen clients and transactions against global sanction lists, such as the OFAC Sanctions List, UN Sanctions List, and EU Sanctions List, to detect and block potential matches and prevent dealings with sanctioned entities.

According to FATF Recommendation 12, enhanced due diligence must be implemented for high-risk individuals, such as politically exposed persons (PEPs), who may be associated with illicit activities.

AML software must screen higher-risk clients against the PEPs list and their respective RCAs to follow a risk-based approach and ensure AML compliance.

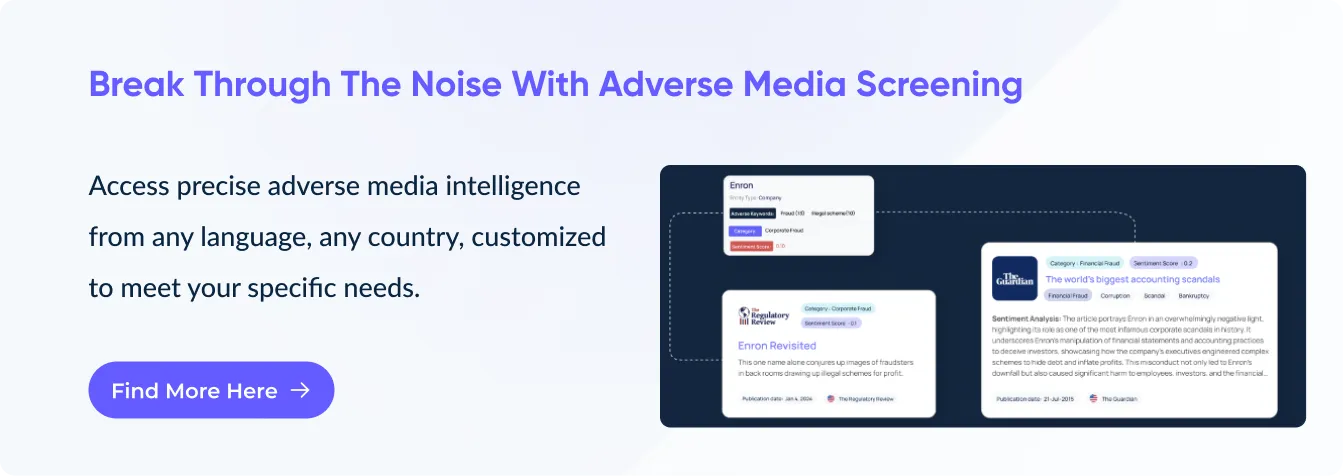

Adverse Media and Negative News Screening

Criminals often appear late on the watchlists and sanctions lists only after a crime has been formally confirmed.

However, Adverse media screening tools help financial institutions screen high-risk clients earlier by scanning press releases from authorities, regulatory announcements, and news sources for associations with predicate offenses.

Financial institutions must perform adverse media screening to detect potential financial crimes before the official AML watchlist integrates the latest updates related to financial crimes.

Stay ahead by screening beyond sanctions and PEP lists and meet regulatory standards. Adverse media screening helps businesses identify reputational risks by flagging individuals and entities linked with negative news or suspected criminal activity.

Suspicious Transactions Monitoring In Real Time

Financial institutions must incorporate AML software into their AML systems that are capable of detecting suspicious activities and generating reports promptly, as required by FATF Recommendation 10, to identify potential financial risks promptly.

Compliance in line with Risk-Based Approach

According to FATF Recommendation 1, a risk-based approach must be followed to combat money laundering and terrorist financing. Financial institutions (FIs) must assess, identify, and understand their specific risks and allocate resources accordingly. Financial institutions must understand and implement measures commensurate with their risk appetite to mitigate risks.

An AML monitoring system tailored to an organization’s risk appetite enables the assessment of risk profiles accordingly, allowing teams to prioritize risk alerts and enhance the accuracy and relevance of those alerts.

Quick Generation of Risk Alerts

In accordance with FATF Recommendation 20, financial institutions and entities subject to AML obligations are required to report suspicious transactions to the Financial Intelligence Unit( FIU).

Following that, AML solutions should generate alerts upon detecting suspicious transaction patterns to ensure timely investigation of potential illicit activities.

So that these activities can be reported to the relevant Financial Intelligence Units (FIUs).

Record Keeping and Audit Trails

The anti-money laundering system must maintain detailed records of all AML compliance activities, as well as records of decisions made based on these activities, to ensure transparency and support regulatory audits. This ensures smooth AML compliance reporting by maintaining accurate records.

Ongoing Transaction Monitoring

AML software must conduct ongoing monitoring of clients and transactions to identify and mitigate financial risks throughout the duration of the business relationship with high-risk clients.

It includes identifying PEPs, verifying their source of wealth, and performing ongoing monitoring of their transactions to mitigate risks linked with PEPs, such as bribery and corruption.

Additional Features for choosing the robust AML Software are given below:

Fewer False Positives

The AML screening system must have the ability to minimize unnecessary alerts and reduce false positives, thereby improving operational efficacy by targeting actual risks.

User-Friendly Interface and Workflow Automation

The AML monitoring system must have a user-friendly interface that simplifies the workflow. It must automate the AML compliance activities to reduce manual work and enhance productivity by shifting the compliance team’s time to investigate and mitigate financial risks. In this way, it increases the team’s productivity and saves time.

Integration Capabilities

AML software solutions must seamlessly integrate with existing software in an organization to ensure smooth AML/CFT compliance tasks.

Global Coverage of AML/CFT Regulations

AML system software must facilitate AML compliance with regulations across multiple countries, adopting a risk-based approach, streamlining reporting tasks, and preventing financial crimes globally.

Having a comprehensive AML software checklist ensures that the AML system includes all the essential features necessary to maintain compliance.

AML Watcher as Your Trusted Compliance Partner

AML Watcher delivers high-quality AML data, covering over 100,000 data sources, thanks to the efforts of hundreds of researchers spanning over.

It simplifies AML screening by encompassing data from over 235 countries and states. It supports more than 80 languages, which helps screen in diverse languages. Phonetics and transliteration feature helps in accurate name matching.

Sanctions Screening

Its sanctions screening feature combines and organizes data from over 215 sanctions regimes to ensure comprehensive coverage. AML Watcher’s unique Sanctions 2.0 ensures that this sanctions data updates every 15 minutes. Such an update is further ensured without delay by adverse media screening.

Adverse Media Screening

Through adverse media screening, financial institutions and AML-compliant entities can scan through 415+ risk categories using NLP-powered sentiment analysis. This ensures that clients are screened against diverse kinds of predicate offenses, including sex trafficking, environmental crimes, ESG violations, and more.

PEP Screening

PEP Screening enables screening clients across 2.6 million+ profiles at 4 PEP risk levels, unlike the legacy AML system.

Fewer False Negatives and Confused Matches

It enhances efficiency by automating AML compliance activities to 90%. It minimizes manual workload and, compared to traditional AML software, delivers 15% fewer false negatives and 11% fewer confused matches to ensure accurate results.

Move Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries