Why AI in Financial Crime Prevention Is More Than a Checkbox

Others

May 14, 2026

- Why AI Financial Crime Prevention Is Reshaping Financial Services

- Regulatory Pressure Is Redefining Anti-Financial Crime Expectations

- Why Traditional Financial Crime Prevention Software Is Falling Behind

- Building a Financial Crime Framework That Adapts in Real Time

- How AML Watcher Supports Smarter Financial Crime Prevention

Financial institutions are spending heavily on compliance technology, yet financial crime losses continue to rise faster than many detection systems can respond. The estimated losses from fraud in 2024 are $442 billion, and the false-positive rate in traditional AML systems remains as high as 90%. The compliance teams remain trapped in the cycle of repetitive manual reviews. However, the cultivated criminal networks move funds across borders within seconds and almost without a trace.

In the meantime, AI-powered fraud is changing the threat landscape. Synthetic identities are gaining access through onboarding systems that are failing to keep up, and deepfake attacks are now being used to foil ID verification systems. At the same time, organized crime groups are increasing the frequency of fraud, which has become too large for legacy monitoring systems to manage.

That’s where the paradigm shift in financial crimes prevention and the use of AI has happened. AI is no longer viewed as a compliance add-on but rather a key tool. It has a significant impact on operational intelligence, fraud detection, more effective investigations, and long-term risk management.

Despite the progress made in recent years, many companies still treat AI as a checkbox exercise. They automate isolated workflows, reduce a few manual tasks, and assume their compliance framework is future-ready.

Regulators, however, increasingly expect institutions to demonstrate that they can detect evolving threats, reduce unnecessary alert noise, and adapt monitoring systems to evolving financial crime patterns in real time.

Why AI Financial Crime Prevention Is Reshaping Financial Services

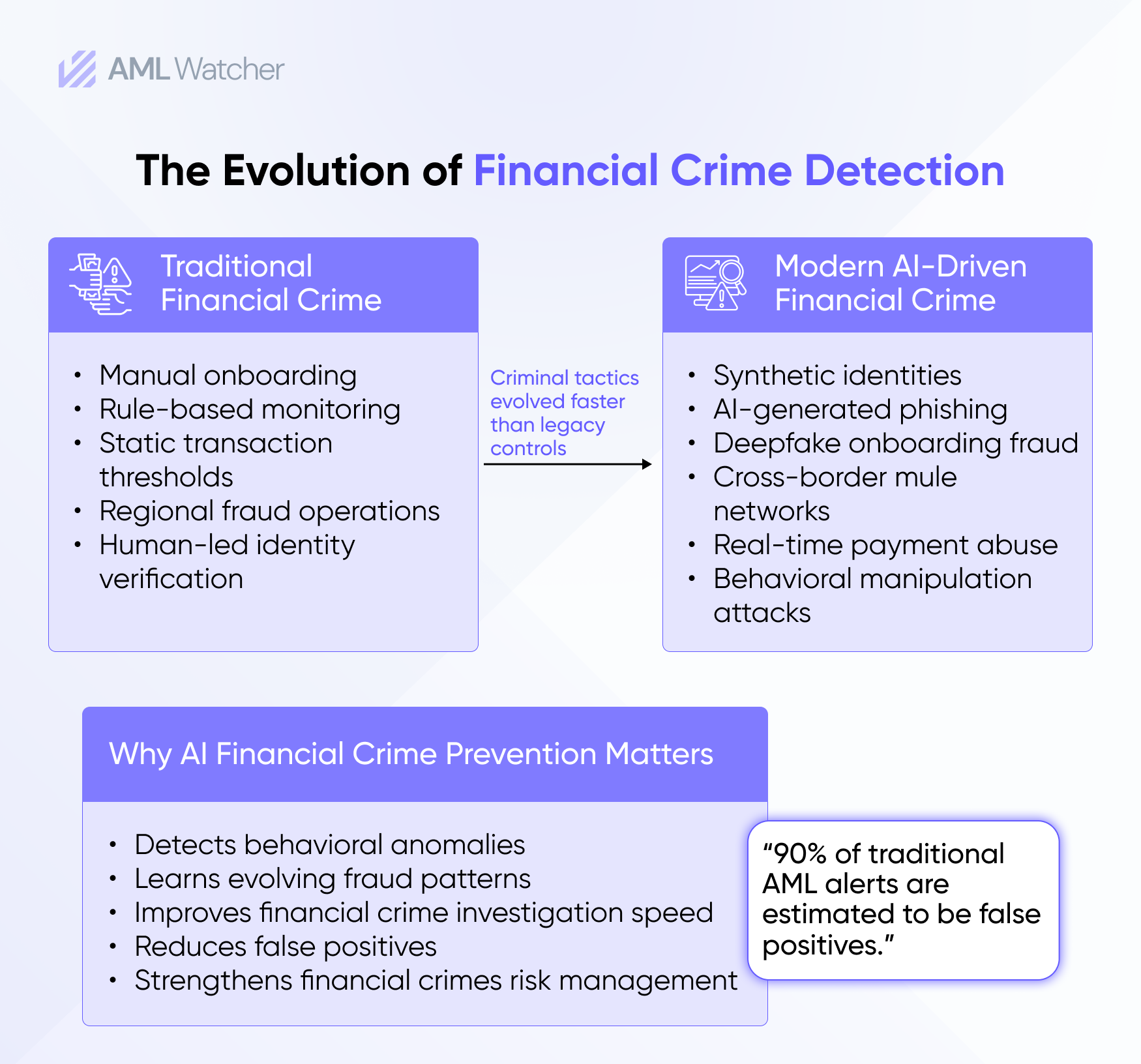

Financial crime has evolved into something quicker, more decentralized, and far more adaptable than traditional monitoring systems can effectively handle. Criminal organizations increasingly depend on sophisticated systems to create synthetic identities and automate phishing schemes. They assess transaction monitoring limits and take advantage of weak onboarding controls within digital payment ecosystems.

The speed of typology evolution has become one of the biggest challenges facing compliance teams. The United Nations Office on Drugs and Crime estimates that up to 5% of global GDP is still lost each year due to money laundering. Meanwhile, there are claims that deepfake fraud incidents surged in North America during 2024, as AI-powered fraud methods continue to proliferate in financial services.

According to Europol and the Financial Action Task Force, AI is driving up the maturity and sophistication of organized financial crime networks. Criminals exploit AI to pay at low levels, automate mule account activity at scale, and scale the customer verification process.

This makes it an easy target for traditional financial crime prevention software. Most legacy systems are based on static rules and thresholds designed for predictable transaction behavior. Criminal networks, however, continuously adapt to avoid triggering those controls.

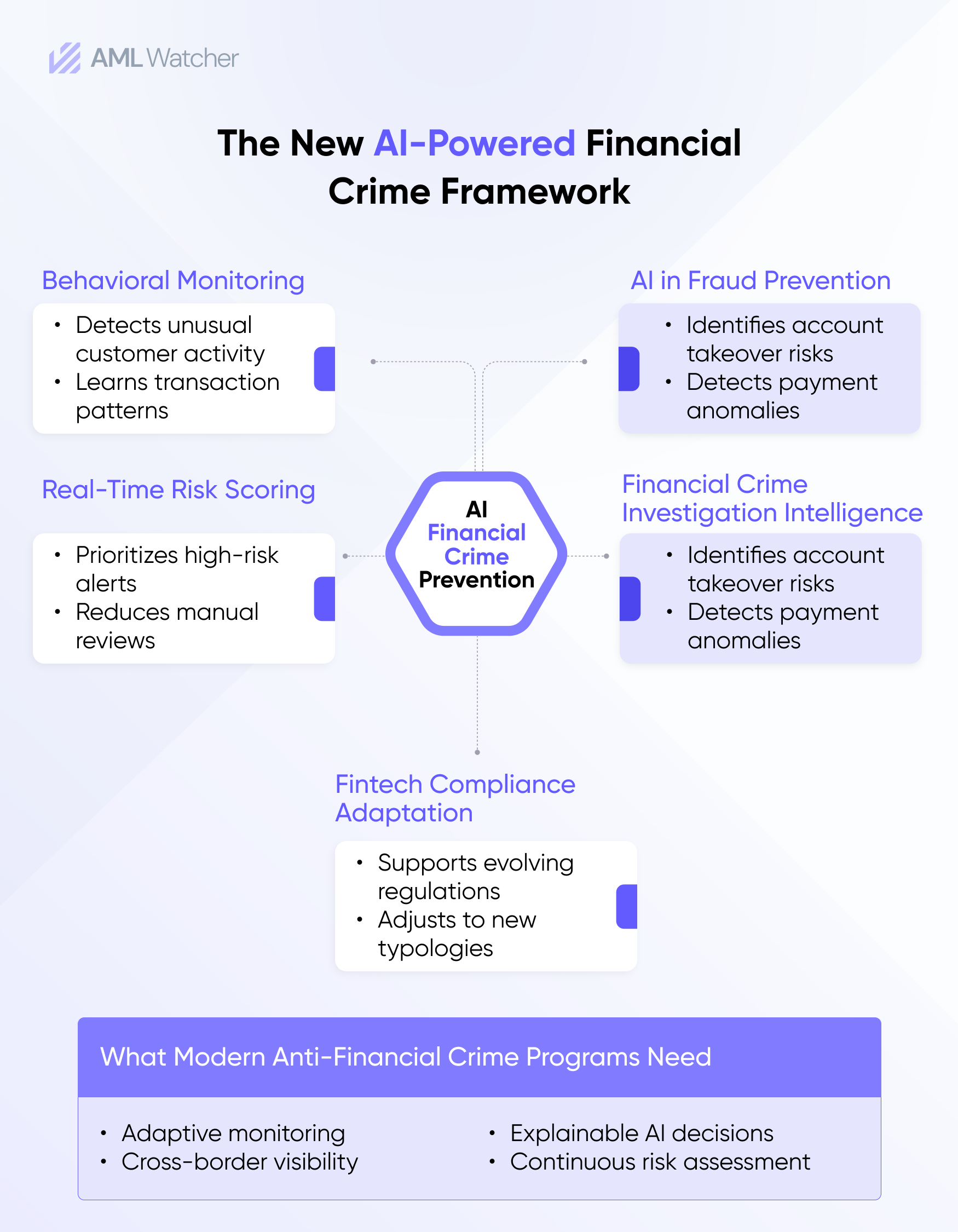

That is why sophisticated fraud detection and prevention methods are playing a big role in today’s fintech compliance processes. AI-driven monitoring tools that are able to analyze behavioral anomalies, identify suspicious transaction relationships, and identify abnormal transaction behavior across customer profiles in ways that static systems cannot.

For institutions operating in real-time payment environments, adaptive monitoring has become a core requirement and an operational necessity.

Regulatory Pressure Is Redefining Anti-Financial Crime Expectations

Regulators are no longer satisfied with institutions simply deploying AML systems. They increasingly expect firms to demonstrate that their controls are intelligence-driven, risk-based, and designed to keep up with the emerging threats.

The Financial Action Task Force updated Recommendation 16 guidance to strengthen payment transparency requirements across traditional and digital transfer systems. FATF’s updated National Risk Assessment guidance also pushes institutions to better identify AI-enabled financial crime risks and emerging money laundering typologies.

The modernization of FinCEN under the Anti-Money Laundering Act of 2020 is ongoing in the United States. FinCEN continues to promote institutions to eliminate low-value reporting noise and enhance meaningful suspicious activity detection. Moreover, the regulators are now increasingly pushing firms to employ advanced analytics and AI-powered monitoring to be more effective, rather than simply increasing alert volumes.

In Europe, the Anti-Money Laundering Authority (AMLA), established in 2022, is launching a more centralized regulatory framework for high-risk institutions. The EU AML package, which comes into effect in July 2027, sets expectations for automated monitoring, customer due diligence, and consistent cross-border compliance.

The Monetary Authority of Singapore (MAS) is further raising its compliance expectations in this regard, such as through the requirement to enhance due diligence practices and transaction surveillance, as per MAS Notice 626.

This points to a broader change in the regulatory sector: institutions are no longer evaluated solely on whether controls exist. They are evaluated on whether those controls can efficiently and consistently identify suspicious activity.

In recent years, the impact of poor monitoring frameworks has grown beyond the regulatory consequences. Measurable business risks include operational inefficiencies, reputational damage, and investigation delays.

Why Traditional Financial Crime Prevention Software Is Falling Behind

One of the biggest weaknesses in traditional financial crime prevention systems is the overwhelming volume of false positives generated during monitoring and screening.

When analysts spend hours reviewing low-risk alerts, compliance costs rise without improving detection quality. Many institutions still rely on systems that generate alerts with little contextual reasoning, forcing investigators to manually collect transaction records, customer profiles, sanctions data, and adverse media findings across disconnected workflows.

This creates severe inefficiencies in financial crime investigation processes.

Analysts tend to spend more time collecting evidence than performing actual risk analysis. Operational workflows rely on manual case preparation, and true high-risk activities could be overlooked because resources are spent on repetitive alert review.

For fintech compliance operations with high volumes of onboarding and cross-border payments, it is even more challenging. Criminal networks exploit the lack of a centralized data system, multiple ownership structures, shell companies, and multilingual publications to conceal suspicious activities across jurisdictions.

Legacy systems also struggle with typology adaptation. Existing rule-based monitoring frameworks are known to require manual rewriting when new types of fraud are identified. The delay between regulators identifying a new typology and institutions updating detection logic creates a measurable exposure gap.

Explainability has become another major concern. Financial institutions are under greater scrutiny from regulators to justify their responses to suspicious activity, whether it is escalated, dismissed, or deprioritized. Compliance risks may arise during regulatory reviews and enforcement investigations when AI systems lack transparency in decision-making and lack clear audit records.

For this reason, financial crime risk management cannot be done with individual screening tools and static monitoring engines.

Building a Financial Crime Framework That Adapts in Real Time

An effective financial crime framework today requires more than automated screening. It requires intelligence-driven monitoring, supported by models that provide clear reasoning, in a constantly shifting risk environment.

Strong AI financial crime prevention systems enhance detection quality by dynamically analyzing customer behavioral patterns rather than relying solely on predefined rules. Using AI models, the relationships among transactions, customer behavior, geographic exposure, and risk signals are assessed simultaneously, resulting in more accurate detection of suspicious activity and fewer false alerts.

AI also enhances the efficiency of investigations. Intelligent monitoring systems onboard do not create risk scores out of nowhere; rather, they provide a reason for the alert – why this activity was detected and what actions should be taken next. This minimizes delays in investigations and enhances the documentation of the audit process for regulatory examinations.

It is also crucial to adapt on an ongoing basis. There are many types of fraud, including mule account abuse, sanctions evasion, trade-based money laundering, and account takeover fraud, which is evolving quickly. Adaptive AI monitoring models that evolve with the changes without manual intervention or rule rebuilding.

This is where AI for financial crime becomes more than a compliance feature. It becomes a strategic operational capability that simultaneously improves the overall detection accuracy, analyst productivity, and institutional resilience.

How AML Watcher Supports Smarter Financial Crime Prevention

AML Watcher places AI-based financial crime prevention at the heart of risk intelligence, rather than a compliance box-ticking exercise. Its AI-enhanced infrastructure minimizes operating friction and enhances investigation accuracy and efficiency.

The TruRisk capability helps compliance teams by reducing false alerts and focusing on justified high-risk alerts. It also improves transaction monitoring using behavioral analysis and flexible anti-money laundering approaches that can adapt to changing risks.

This system brings together sanctions screening, monitoring of negative news, watchlist checks, and ownership information into a single process. This integration helps organizations see more clearly, reduces delays, and improves compliance effectiveness.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries