Detect Rising Threat of Financial Crime in the Digital World

AML/CFT

June 25, 2025

- What is a Financial Crime? Know Its Significance in the Digital World

- How are Types of Financial Crime Evolving?

- Significance of Anti-Money Laundering (AML) Regulations in Fighting Financial Crime

- How Financial Crime Analytics Assist in Identifying Other Crimes?

- Key Components of a Modern Financial Crime Analytics Solution

- Role of Adverse Media Screening

- Reinforce Your Defenses with AML Watcher

Financial crime is a growing problem for digital businesses today. It allows illicit activities, for instance, human exploitation, drug trafficking, corruption, and terrorism. This poses a threat to the economy and creates public distrust.

As the IMF illustrates, the amount of money that is laundered annually is between 2% and 5% of global GDP. The rise of online marketplaces is likely to fuel the global movement of illegal funds, as it facilitates cross-border transactions.

Furthermore, the criminal networks are developing new strategies; Therefore, it is demanded from regulatory enforcement and FIs to deploy a quicker or intelligent response to secure the financial landscape.

What is a Financial Crime? Know Its Significance in the Digital World

The digital financial crime meaning refers to an illegal process of acquiring monetary assets, including money, securities, or property, by exploiting e-platforms and emerging tech. It involves hacking to gain illicit access. When this is done, criminals demand payments in cryptocurrency, which are online payments and are difficult to trace by the authorities.

Sometimes the criminals use ransomware that locks the files until the victim pays the demanded money. Beyond all these list of financial crimes, social engineering is at the top.

This scam includes manipulating people through psychological tricks to get their sensitive information and gain access.

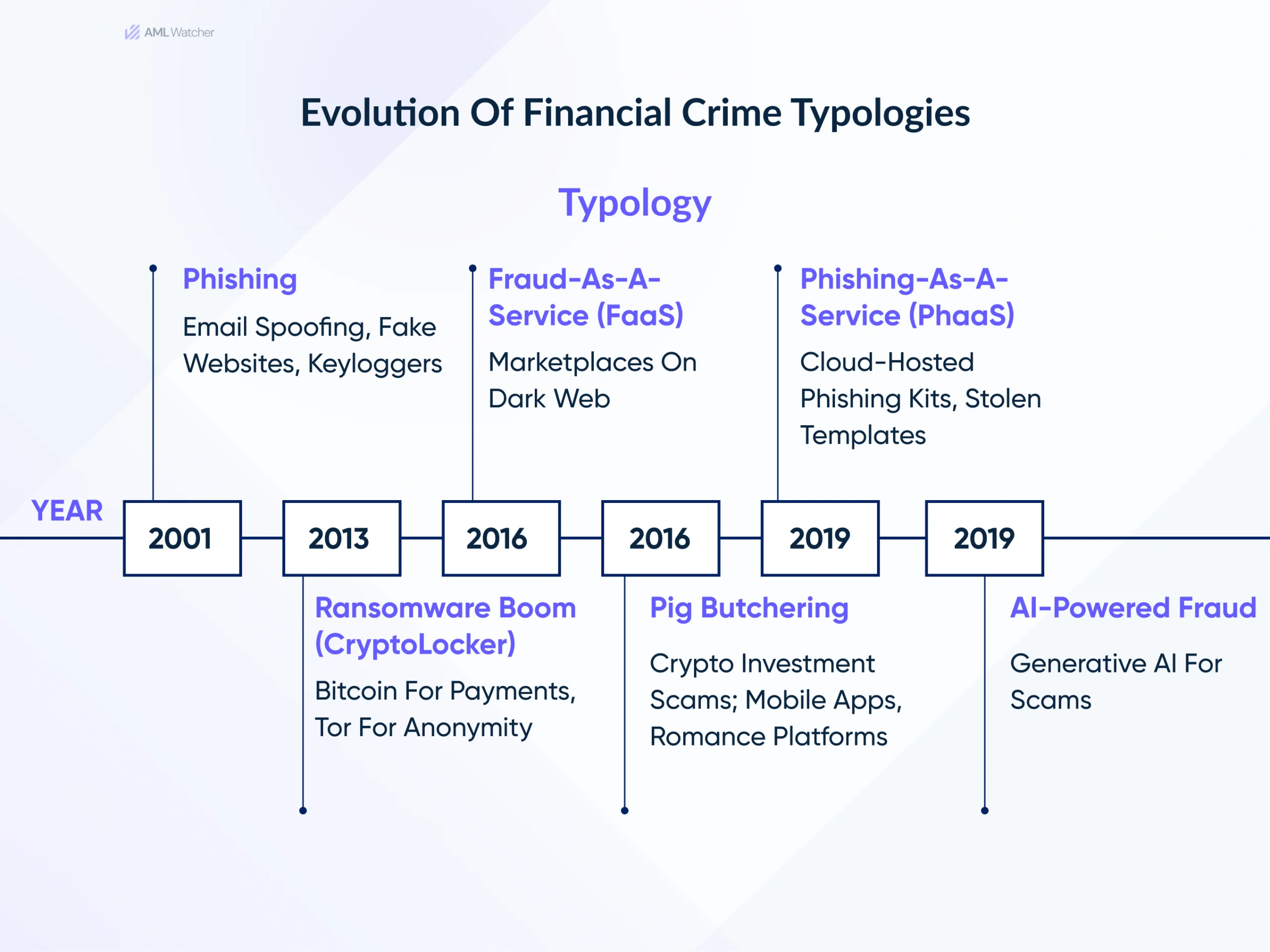

How are Types of Financial Crime Evolving?

Financial crime is going through a spectrum of transformation supported by similar technologies that are driving the legal digital economy.

New technologies such as encrypted messaging chats, dark web forums, and other anonymous e-platforms have made it accessible for criminals to begin and find new ways to commit crimes.

According to a 2025 Europol report, organized crime is developing in the digital world. One of the major issues that the report highlights is AI-powered fraud, which uses stolen data and advanced social engineering as a top threat.

A 2024 report by Africa Cyber Threat Assessment proves this statement right by illustrating a collaboration of Interpol and Afripol, where they arrested approximately 1,006 suspects and deactivated 134,089 malicious networks and infrastructures.

In such cases, criminals use different financial crime examples such as:

- Ransomware

- Use of different IP addresses

- Cryptocurrency Laundering

- Trade-based money laundering

- Online Investment and Romance Scams

As the financial crime framework is getting more complex with time, criminals rely on the following services:

- Phishing-as-a-Service (Phaas)

- Fraud-as-a-Service (Faas)

Phaas assists scammers in making the initial contacts and building confidence, mostly by promoting fake messages and profiles.

After the victims are drawn in, Faas takes over to commit the actual fraud, providing things like fake investment platforms and deceptive scripts to illicitly obtain funds.

For example, Pig-Butchering scams involve a chain of crimes, including human trafficking, cybercrime, romance scams, and investment scams.

Effective detection and combating of this crime through the financial system requires using a diversity of anti-fraud and anti-money laundering tools.

Significance of Anti-Money Laundering (AML) Regulations in Fighting Financial Crime

In order to ensure due diligence, transparency, and reporting, government and international legislative authorities (like the UN, EU, G7/G20) have established legal structures.

In this case, the Financial Action Task Force forms the core, serving as the global standard for AML and counter-terrorist financing (CTF) compliance.

These guidelines are for the FIs to have clarity about the real Ultimate Beneficial Owners (UBO) and enforce risk-based approaches. Additionally, FATF guides and asks for identifying the customers who could be politically exposed persons (PEPs).

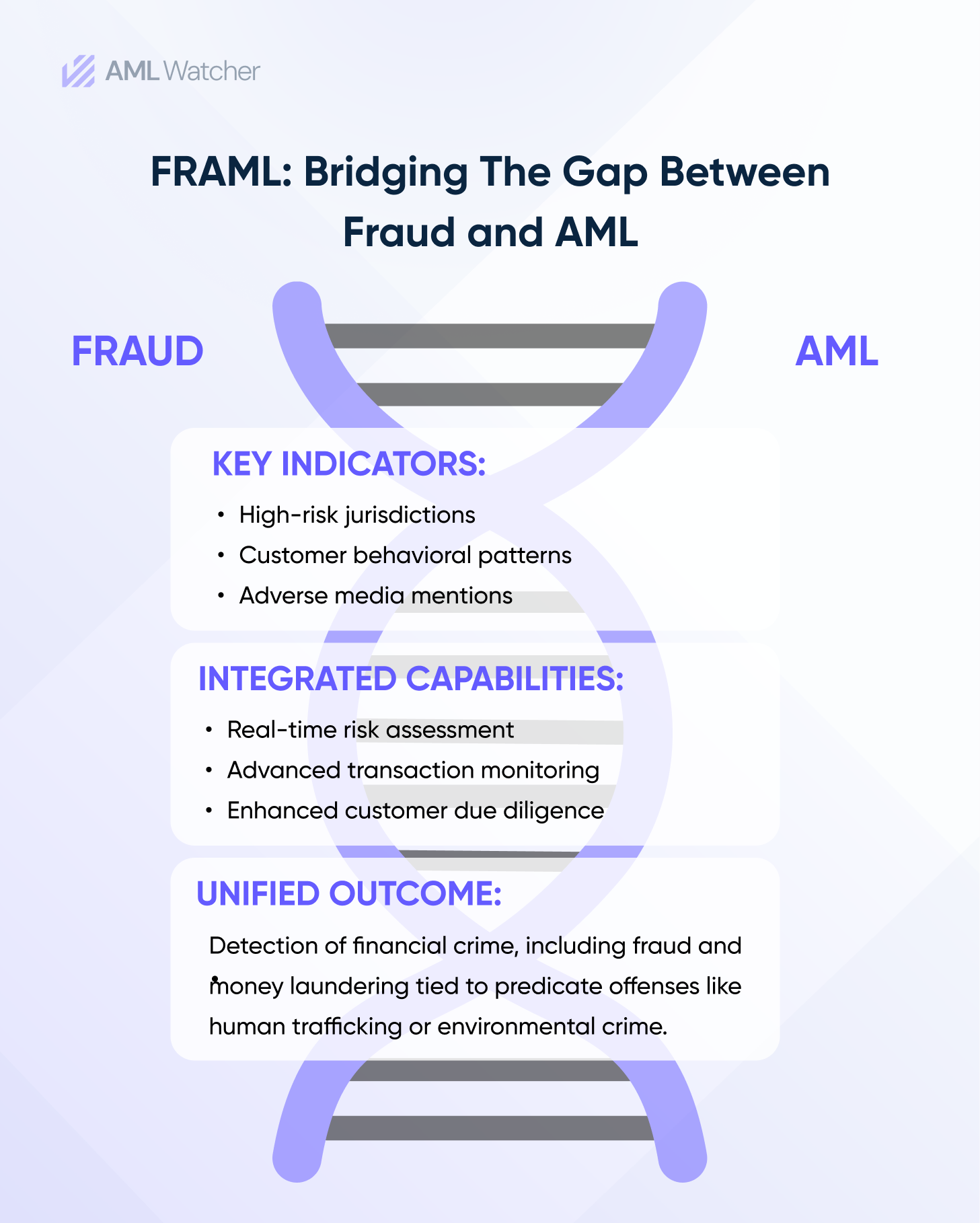

Understanding Fraud and Anti-Money Laundering (FRAML)

FRAML stands for “Fraud and Anti-money Laundering”. It’s the combined form of fraud and Anti-money laundering.

As the AI-powered fraud and the limitations of conventional systems in detecting the new fraud typologies pose problems for businesses, there is a dire need for a new approach, i.e, FRAML.

It’s a defensive act against advanced financial crimes, allowing financial institutions to be more adaptive and stay ahead of the criminals.

FRAML is not just a concept; it plays an active role in fighting money laundering and fraud. Many individuals think that fraud can’t be detected by an AML solution. However, it is possible.

Suppose an individual who sends money to a region that is famous for any predicate offense, or in another scenario, if the person sends a lot of money to one similar account within a region where cybercrime compounds exist.

Both of them can be a source for human trafficking. Therefore, there is a need to detect fraud, and it is possible through adverse media screening and transaction monitoring.

When banks and other financial institutions do not adhere to the anti-financial crime regulations, it makes it convenient for criminals to perform such predicate offenses.

A lack of robust AML compliance actually leads to hefty penalties, as reflected in 2024’s major AML fines.

The year 2024 has come up with diverse penalties for the FIs that mostly have no control over their AML programs. For Instance, City National Bank faced a penalty of $65 million for risk management failures.

Similarly, National Westminster Bank plc (NatWest) was fined €264 million by the UK’s Financial Conduct Authority (FCA) in 2021. This penalty was the result of poor AML controls.

Having good laws at the jurisdiction and international levels is not enough; organizations need effective internal systems that help them actually adhere to these regulations.

How Financial Crime Analytics Assist in Identifying Other Crimes?

Financial crimes are mostly a way to hide even worse criminal activities, such as human trafficking, damaging the environment, and corruption.

With the proper analysis of irregular transaction patterns like sending money to high-risk jurisdictions or making huge payments to shell companies, institutions can successfully link transactions to criminal networks.

A 2018 report by FATF, including their ongoing work on human trafficking typologies, exposes the fact that payments seen as regular from certain entities, such as job agencies or recruitment firms, can actually conceal the exploitation of migrant workers. This slight shift in money flows actually hides human trafficking.

To identify associations with predicate offenses, FIs shouldn’t only monitor transactions, but they should also perform investigations incorporating customer behavioral patterns and external intelligence; such tactics assist financial institutions in detecting these crimes.

A 2024 MALTA Human Trafficking report by FIU Malta guides financial institutions on identifying trafficking and modern slavery with financial red flags.

Suspicious transaction patterns, geographical indicators, and customer behaviors are of major focus, and the report mandates modern tracing systems along with enhanced AML compliance to combat financial crimes.

Key Components of a Modern Financial Crime Analytics Solution

An ordinary compliance checklist is not enough for today’s financial institutions in order to counter the emerging dangers. An advanced financial crime analytics solution must exhibit the following crucial components to sustain itself. These key components are:

-

Ongoing Customer Risk Assessment

Advanced crime analytics must skip the static financial crime risk management, instead of checking the client’s risk the moment they sign up they and assessing their behavior.

In terms of any changes or new information, the customer’s risk score is updated instantly, which assists financial businesses in understanding the risk status of their client.

-

Sanctions and Watchlist Screening

A financial crime analyst responsible for operating the advanced financial analytic solution must check the newly entered customers against the sanctioned lists, which helps FIs know if the client has their name on any sanctions list.

-

AI-Powered Monitoring

AI-powered transaction monitoring is the core of an AML program; it integrates smart analysis to spot anomalies and financial behaviors. It must look for patterns that the rule-based systems mostly ignore.

-

Adverse Media Screening

It’s a must-have component for an advanced financial crime software. When a solution offers adverse media screening, it means it can identify global news sources against the customers for verifying whether they have their names in any negative news.

It can be about an individual or an organization. With this, FIs are able to identify the hidden risks about the customer even before it hits the headlines.

Role of Adverse Media Screening

In order to effectively detect financial crime according to evolving crime typologies, FIs can implement adverse media screening that serves as a critical early warning for them.

Adverse media screening plays a significant role when businesses struggle to properly trace global news, legal announcements, and regulatory updates, as it assists in preventing unnoticed potential reputational damage and emerging risks.

It has the ability to detect the red flags associated with individuals, and this task is done efficiently by adverse media screening during the rapid processing of unstructured data.

FI’s with proper negative news coverage can easily reinforce their defenses against financial crime and ensure adherence to legal standards.

Crown Melbourne and Crown Perth were fined by Austrac in 2023. This fine was a huge amount, approximately $450 million. The reason behind this penalty was weak AML/CFT Programs and a lack of proper checking of fund origins.

Reinforce Your Defenses with AML Watcher

With the constant growth of financial fraud crimes, a mere baseline compliance is not enough. FIs need actionable intelligence.

This is not only necessary to ensure effective compliance with Anti-Money Laundering regulations, but also for mitigating the risks and saving the costs that may be incurred in the form of reimbursement.

AML Watcher empowers businesses to effectively detect financial crime, designed specially to meet the emerging challenges.

- Risk scoring and customer profiling

- Updated sanctions list screening

- Real-Time Adverse Media Screening

- Ongoing Customer Risk Scoring

- Warnings and Regulatory Enforcements Screening

- Ongoing transaction monitoring

Frequently Asked Questions

Financial crime compliance (FCC) is the regulations, policies, and practices that the FIs integrate in order to prevent money laundering and organized crime.

Fraud is a category of crime that involves trickery in order to gain an illegal benefit, whereas financial crime is something that includes the illicit activities that involve any asset, such as money or property.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries