Essential Regulatory Requirements in AML

AML Regulations

January 20, 2026

- The Role of FATF Standards in Shaping Essential Regulatory Requirements for Anti-Money Laundering (AML)

- Essential AML Regulatory Requirements for Financial Institutions

- United States’ Essential Regulatory Requirements for AML

- Key EU Laws Setting Regulatory Requirements for AML

- AML Watcher Empowers Financial Institutions to Meet Essential Regulatory Requirements in AML

Money laundering remains a silent partner of crime. As global finances get tighter and more inter-connected so have unanimous governmental efforts to overcome and stay ahead of financial crime.

The world is currently grappling with financial crimes, theft, fraud and money-laundering. In order to tackle and keep up with the pace of such actions, the emergence of regulatory requirements and their fulfillment has become an essential necessity that has been worked on for many years and is currently still under progress.

Countries across the world came up with their own regulatory standards that were bound to be met by companies functioning and growing over there.

The Role of FATF Standards in Shaping Essential Regulatory Requirements for Anti-Money Laundering (AML)

The Financial Action Task Force more commonly known as the FATF, is an international financial watchdog. It sets the international agreed upon standards for AML compliance. It was established in 1989 and since then more than 200 jurisdictions are associated with FATF’s international network. The FATF in 1990 released a set of recommendations “The International Standards on Combating Money Laundering and the Financing of Terrorism and Proliferation” that became the benchmark for internationally accepted measures for AML.

It also published nine special recommendations, adding to the previous 40, which were later merged into 40 recommendations.

Essential AML Regulatory Requirements for Financial Institutions

These are the “non-negotiables” regulators expect from businesses to have in place so they can build trust on how they operate and control the scope for risks. The FATF sets standards for AML. Countries as a result transpose them in their national laws, and those national laws state obligations for the regulated sectors.

Maintain an AML Program

The maintenance of an AML program is essential for organizations because it is a customized comprehensive framework of the companies’ internal policies and procedures. It basically helps the organizations to prevent and detect money laundering and other financial crimes that adhere to laws like the Bank Secrecy Act (BSA) and the EU AML Directives.

Adopt a Risk-Based Approach

According to FATF Guidance for the Banking Sector “ a risk based approach means that countries, competent authorities and banks, identify, assess and understand the money laundering and terrorist financing risks to which they are exposed and take appropriate mitigation measures in accordance with the levels of risk.”

FATF also highlights for businesses that the mandatory adoption of a risk-based approach does not equate to it demanding a “zero-failure approach”; institutions may still face money laundering risks despite having reasonable measures in place.

Conduct Sanctions Screening

Compliance with sanctions laws is not specifically a requirement applicable only on AML obliged entities, however, regulators globally expect that financial institutions maintain a robust sanctions screening system. Therefore, sanctions screening remain a crucial tool for financial institutions to avoid dealing with individuals and parties restricted by the law.

Implement Transaction Monitoring

Monitoring transactions remains an important task for compliance officers. This is because after onboarding there still remains a risk for suspicious activity from clients that seemed harmless during the screening process. They may indulge in some suspicious activity after successful onboarding, therefore consistent transaction monitoring is key to avoid such circumstances.

Maintain internal AML SOPs

Maintaining internal policies, procedures and controls is a necessary foundational requirement globally. A step-by-step procedure that shows how the organization detects money-laundering and other related financial crimes. These procedures keep laws and the firm’s policies in sync with each other. They are further translated into daily actions for staff and employees.

Conduct Customer Due Diligence

CDD is a fundamental requirement for regulated businesses. CDD is the process of verifying and identifying customers and assessing any risks that can be associated with them to ensure compliance with AML regulations. It includes identity verification, risk profiling and enhanced due diligence. The process of identifying and verifying a customer identity to assess their risk profile.

File Suspicious Activity Reports (SAR Filing)

The fact that there are a handful of AML requirements that need to be catered to, the purpose of them to exist trickles down to achieving this particular outcome which is filing SARs. Trained employees are to identify red flags that signify any suspicious behaviour post successful onboarding screening process of a client.

Comply with Documentation and Retention Requirements

Any company or organization adhering to compliance regulations must keep records of all customer identification documents, transaction records as well as SARs for a period of time in order to facilitate any inquiry by higher authorities. Flagged transactions must always have manual investigation in order to determine their legitimacy.

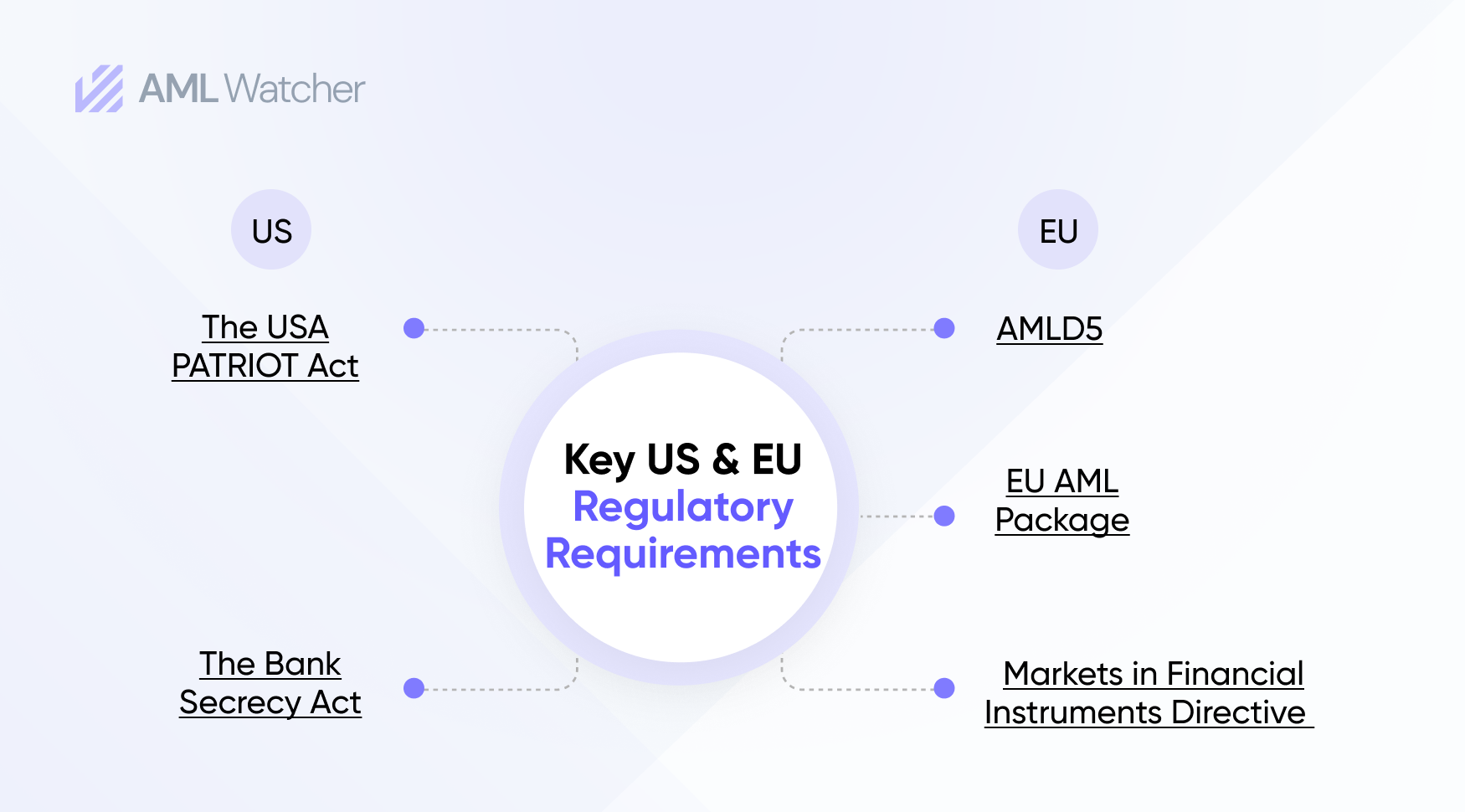

United States’ Essential Regulatory Requirements for AML

As the financial service sector remains one of the most regulated industries across the world, the United States came up with certain necessary regulations to keep up with all relevant and necessary requirements.

Organizations are required to uphold fair and transparent reporting that are in sync with federal laws and rules. The United States came up with two laws that serve as the cornerstone for financial regulations in the country.

- The USA PATRIOT Act was implemented to deter and punish terrorist acts in the United States. Section 326 of the Act prescribes minimum requirements essential for identification of the customers of financial institutions. Similarly, section 352 of the same Act requires financial institutions to maintain an AML compliance program with set minimum standards like development of internal policies, procedures and controls, appointment of a compliance officer, employee training and independent audit function.

- The Bank Secrecy Act imposes reporting requirements on financial institutions to help detect money laundering. It requires financial institutions to maintain records, report SARs, especially cash transactions (CTRs) of over $10,000 to FinCEN.

Key EU Laws Setting Regulatory Requirements for AML

Similar to the United States, the European Union in accordance with the demand of the financial service sector proceeded to implement its own regulations to meet all requirements.

- EU AML Package published in the official journal in June 2024 seeks to harmonize and strengthen anti-money laundering regulations across the EU. This package included an EU-wide applicable Anti-Money Laundering Regulation (AMLR), and a regulation (AMLAR) to establish a new Anti-Money Laundering Authority (AMLA). Additionally, it included the 6th AML Directive which seeks to harmonize and extend transparency registers across the EU.

- AMLD5 is an EU Anti-Money Laundering directive that brings virtual currencies and wallet providers under AML obligations.

- Markets in Financial Instruments Directive increased clarity in financial transactions and operations, it also created uniform reporting standards for investment firms and banks.

AML Watcher Empowers Financial Institutions to Meet Essential Regulatory Requirements in AML

Financial institutions often struggle to keep screening, monitoring, and documentation consistent while onboarding volumes rise and typologies change. AML Watcher supports compliance teams with sanctions and PEP screening and configurable matching using Custom Search Profile so reviews focus on higher-quality alerts. Businesses spend less time and resources on reviewing false positives when screening solutions are customized as per their risk appetite and needs.

A demo can show how these controls fit into existing AML workflows.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries