Measuring the ROI of AML Screening in Financial Crime Prevention

Others

June 18, 2026

Financial crime continues to impose a significant burden on the global economy and regulated institutions. According to the International Monetary Fund (IMF) and the United Nations Office on Drugs and Crime (UNODC), the estimated amount of money laundered each year globally ranges between 2% and 5% of global GDP. At the same time, financial institutions face rising compliance obligations, with global financial crime compliance costs exceeding $206 billion annually. As criminal networks adopt increasingly sophisticated methods and regulators intensify oversight, organizations must strengthen their screening and monitoring capabilities to identify risks more effectively and maintain regulatory compliance.

Financial institutions continue to increase investment in compliance with financial crime as the regulatory expectations expand across jurisdictions. Despite rising spending, enforcement actions remain high, which reveals a disconnect between compliance investment and measurable risk reduction. This gap has shifted attention toward how AML screening performance is evaluated and whether return on investment is being properly measured.

Financial Crime Growth and International Regulatory Response

As financial crime schemes become increasingly sophisticated, regulators continue to strengthen anti-money laundering requirements and enforcement efforts. Regulatory expectations surrounding financial crime compliance continue to expand globally. PwC’s Global Economic Crime Survey 2024 found that economic crime risks are becoming increasingly complex due to geopolitical tensions, sanctions obligations, supply chain risks, and evolving fraud schemes. Additionally, 59% of surveyed organizations reported that export controls have become more complex and are being enforced more rigorously than two years ago. Organizations are therefore under growing pressure to implement stronger risk management, due diligence, and screening programs.

OFAC continues to broaden its Specially Designated Nationals (SDN) list. This has increased enforcement against non-US entities caught transacting with sanctioned parties through secondary sanctions. Meanwhile, the Financial Crimes Enforcement Network (FinCEN) requires organizations to identify beneficial owners and submit Suspicious Activity Reports (SARs) in compliance with the Bank Secrecy Act and the Customer Due Diligence Rule. It’s worth noting that in 2024, more than 10,000 SARs were filed each day.

Moreover, the EU’s 6th Anti-Money Laundering Directive (6AMLD) extended predicate offense categories to 22 types and introduced criminal liability for legal persons. MAS Notice 626 in Singapore mandates customer due diligence, enhanced due diligence, together with continuous monitoring for all licensed financial institutions. FATF Recommendations 12 and 22 require enhanced due diligence on politically exposed persons across financial institutions and designated non-financial businesses and professions.

Regulatory obligations now extend across more customer categories, transaction types, ownership arrangements, and high-risk jurisdictions. Enforcement penalties for AML control failures continue to increase across major jurisdictions. Any assessment of AML screening ROI needs to reflect this reality, expanding regulatory burden and enforcement environment.

The Hidden Costs Eating Your AML Compliance ROI

The cost of AML screening inefficiency rarely appears in a single budget line. It accumulates across investigation workloads, onboarding delays, and compliance backlogs, creating investigation workflow delays and staffing pressure as workloads grow.

False positives represent one of the highest operational in compliance cost. Many institutions underestimate the resources required to investigate alerts that later turn out to be legitimate. Industry research consistently estimates that 90% to 95% of alerts produced by conventional AML systems are false positives. Compliance analysts spend approximately 32% of their working day reviewing transactions that are ultimately cleared as legitimate. At scale, this consumes substantial analyst capacity that could instead be allocated toward higher-risk investigations.

The operational consequences extend well beyond alert review workloads. Manual review backlogs slow customer onboarding. Studies show that between 50% and 70% of customers abandon account opening during identity verification. Every abandoned application represents potential revenue that never reaches the institution. Each delayed onboarding is a competitive disadvantage against more agile institutions.

False Negatives Carry A Different, More Acute Risk

A system configured to lower false positives too aggressively ends up missing genuine matches. A sanctioned entity slips through. A politically exposed person onboards without enhanced due diligence. A money mule moves funds undetected. The resulting risks include regulatory exposure, penalties, and damage to brand trust that dwarf the cost of the screening program itself. Maintaining compliance averages $5.47 million annually, but non-compliance costs average $14.82 million when fines, remediation, and lost business are combined.

The bigger issue is not the cost of AML screening itself. It is the cost of poorly calibrated controls that creates large volumes of irrelevant alerts, misses meaningful risk, exhausts analysts, and still leaves institutions exposed.

How to Calculate the AML Screening Benefits That Actually Matter

The return on investment of AML screening isn’t a single number. It’s a composite of avoided costs, recovered efficiency, and protected revenue. Three categories drive most of the value.

Penalty avoidance is the most direct AML screening benefit. A single enforcement action can cost hundreds of millions in fines, remediation, and legal fees. In 2023, AML non-compliance fines globally exceeded $6.6 billion. The portion of penalties that can be avoided, based on the level of risk an institution faces, serves as a tangible input for calculating return on investment. Compliance departments that calculate their regulatory risk exposure and assign probability-weighted penalty scenarios have a defensible number to present to the board.

Efficiency improvements are where AML screening software delivers measurable, recurring savings. Every reduction in the false-positive rate directly translates into analyst hours recovered. Cutting false-positive alerts by 44% in a team managing 500 alerts per week eliminates more than 200 unnecessary reviews. Those recovered hours can instead be focused on higher-risk investigations or help control staffing costs as screening volumes increase.

Revenue protection and onboarding efficiency provide the final component of AML screening ROI. AML screening solutions that integrate directly into onboarding workflows reduce verification friction. Faster, cleaner customer onboarding retains customers who would otherwise abandon the process, protects fee income, and helps organizations scale confidently without increasing regulatory exposure.

Cost savings from AML compliance, when accurately measured, stem from all three categories at once, rather than solely from avoiding fines.

What Effective AML Screening Solutions Must Deliver

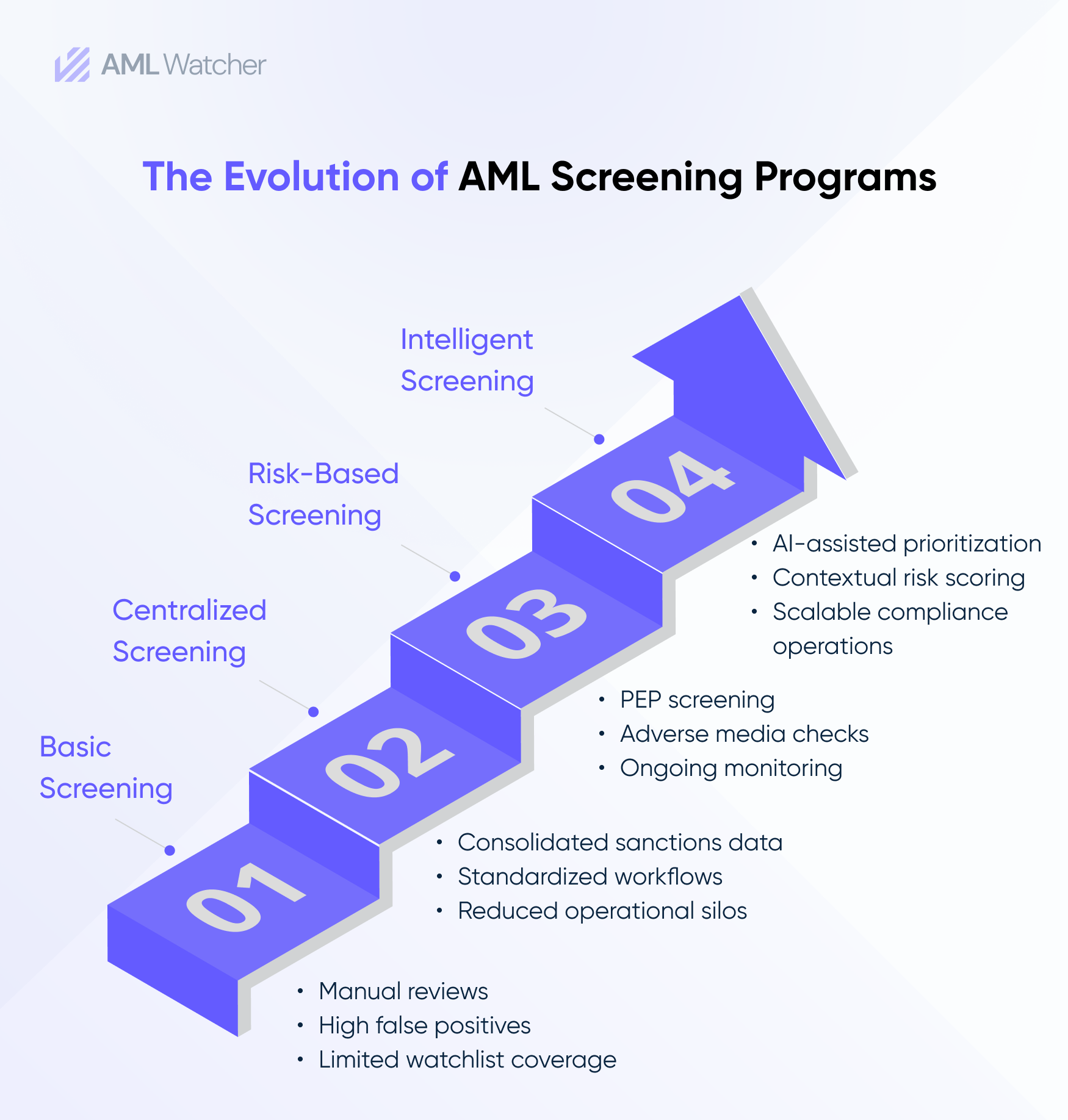

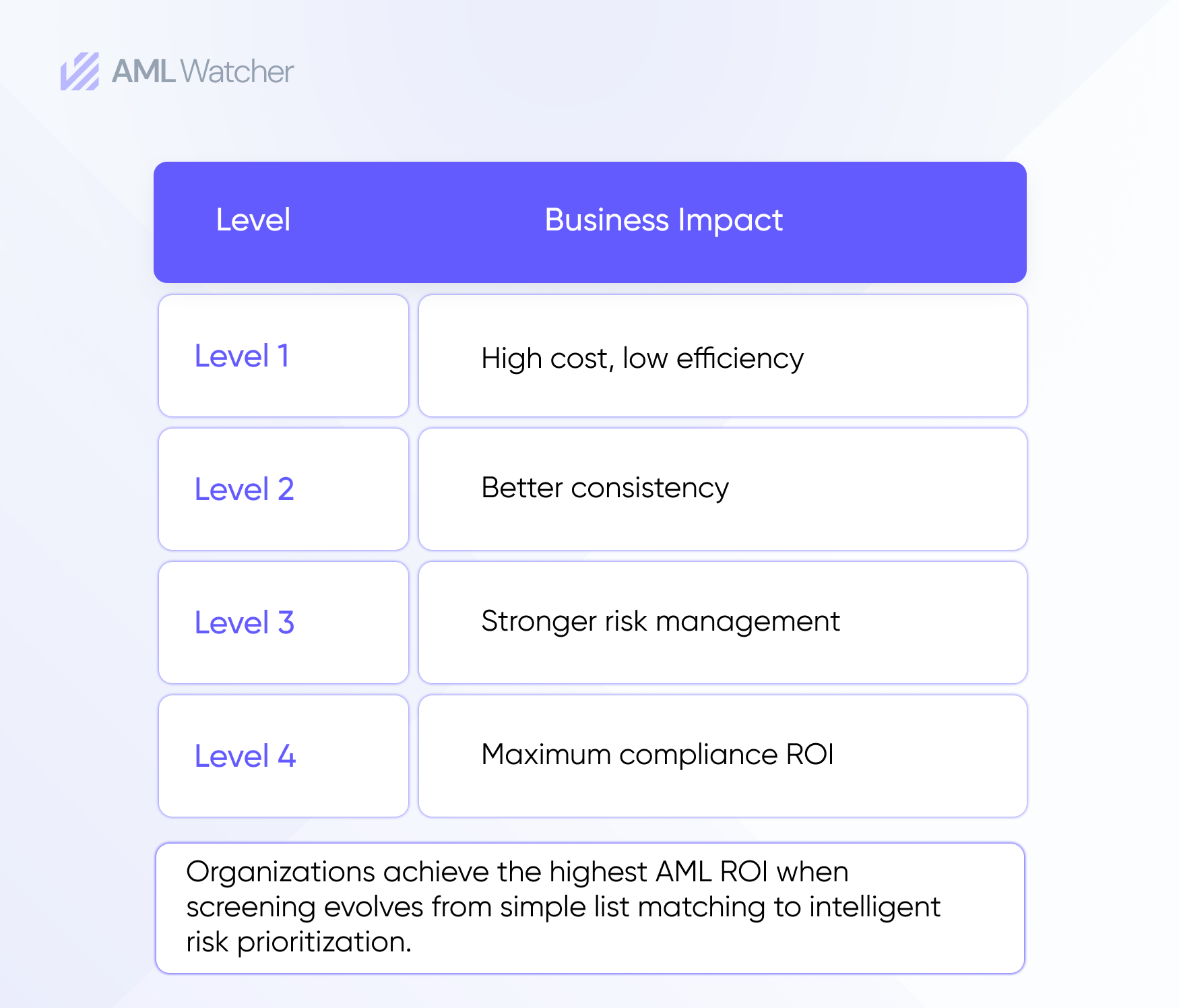

Institutions that produce measurable compliance value typically apply a consistent screening strategy. They view screening as a fundamental risk-management function rather than a compliance expense.

Effective AML screening solutions need to do more than check names against lists. They need to deliver accurate matching across sanctions, PEP databases, adverse media sources and watchlists in a single workflow. Gaps in any one dimension create regulatory exposure. Fragmented providers, separate systems for sanctions screening, PEP screening and adverse media screening, multiply integration costs, and create data consistency problems that undermine the quality of the match itself.

Strong data coverage requires both the breadth of available data and sufficient depth within each dataset. PEP databases must cover far beyond heads of state and senior ministers. Missing Level 3 and Level 4 officials, mayors, provincial executives, and judicial appointees can expose institutions to the types of risks regulators examine during mutual evaluations. Sanctions data that updates once per day is inadequate when OFAC and EU designations can change at any time. Ongoing monitoring that automatically rescreens customers as their status changes is not a premium feature; it is a regulatory expectation.

Many modern AML screening platforms now use AI-assisted prioritization to reduce false-positive levels without sacrificing risk-detection accuracy. Compliance teams that still rely on rule-based systems are absorbing costs that AI-augmented screening eliminates at the point of alert generation, before analysts engage.

How AML Watcher Delivers Measurable Compliance ROI

AML Watcher addresses operational inefficiencies in AML screening, including high false positive rates, fragmented risk intelligence, and resource-intensive alert investigations. The platform consolidates sanctions data across 215+ domestic and international regimes supported by regular updates and broad watchlist coverage.

TruRisk applies contextual identifiers and structured risk indicators to enhance matching relevance, helping compliance teams reduce unnecessary alert reviews and investigative workload. This improves screening efficiency across customer onboarding and continuous monitoring while helping teams process higher screening volumes without increasing staffing requirements.

As alert volumes keep increasing, many financial organizations find it difficult to maintain investigative efficiency without expanding compliance resources. Screening systems that generate an overwhelming number of false alerts can slow onboarding, drive up operating expenses, as well as reduce the total value derived from compliance investment.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries