How Financial Institutions Use Device Intelligence to Stop Fraud?

Fraud Prevention

June 3, 2026

- What Is Device Intelligence and How Does It Work?

- The Regulatory Pressure Compliance Teams Cannot Ignore

- Where Compliance Programs Are Actually Failing

- Device Intelligence for AML Compliance and Fraud Detection

- How AML Watcher Strengthens Risk Detection Beyond Device Signals

- Building Stronger Fraud and AML Defenses

Fraudsters no longer need to steal the customer’s identity to take over their account. They only need the right device, a spoofed environment, and a stolen credential bought for pennies on the dark web. By the time a transaction monitoring alert fires, the money is already gone. Device intelligence closes that gap. According to an FBI report, bank account takeover fraud alone caused over $262 million in losses in 2025.

The problem is with the way identity verification is structured. Traditional methods, such as passwords, one-time codes, and KYC document checks, only confirm a person’s identity at a specific moment. They cannot tell whether the person using those verified credentials today is the same person who passed onboarding last quarter. Synthetic identities, credential stuffing, and AI-generated deepfakes have made the question of “who is this user?” much harder to answer from identity data alone.

What Is Device Intelligence and How Does It Work?

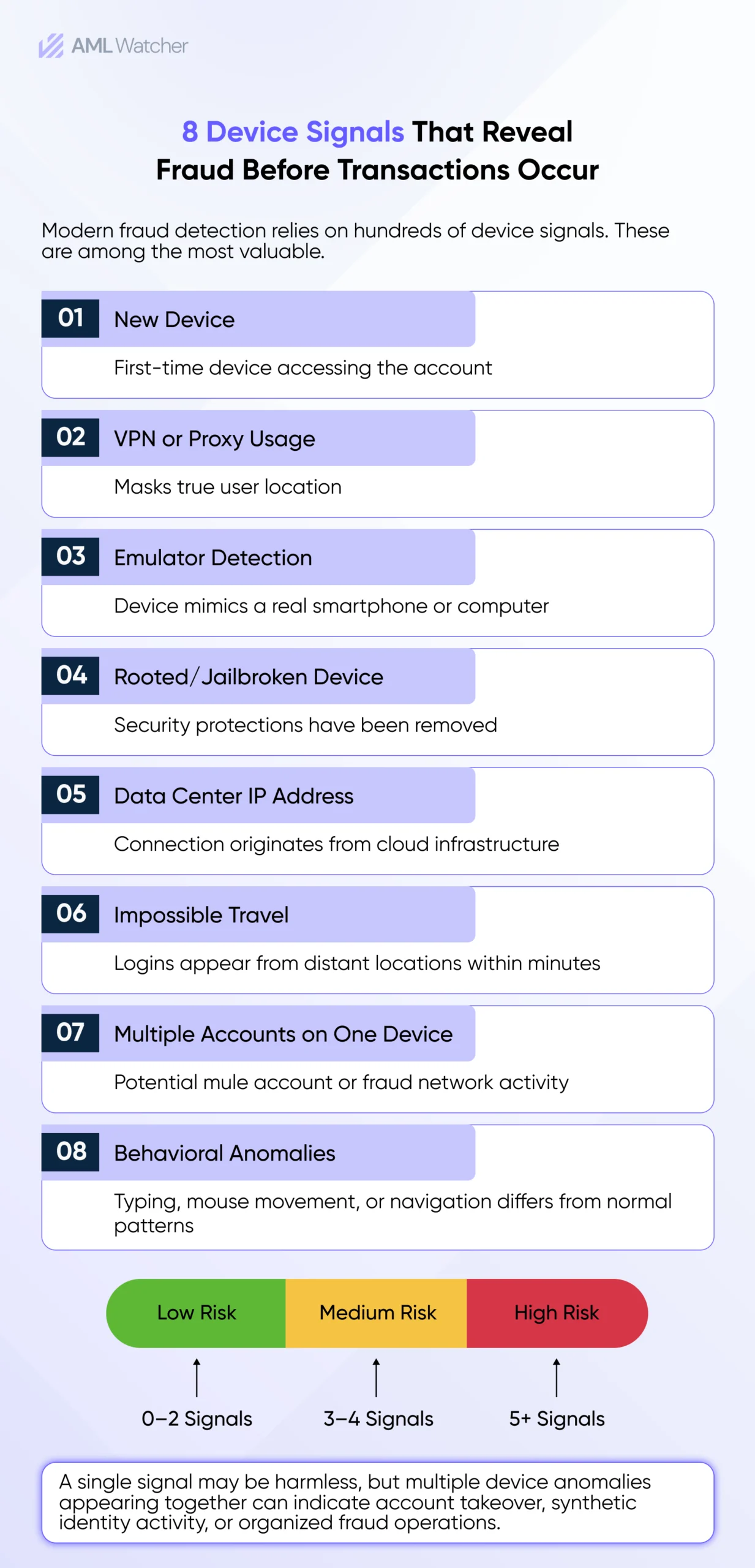

The process of gathering and analyzing signals from a user’s device, network, and behavioral environment to determine the legitimacy of an interaction is referred to as device intelligence. As a user joins a platform, their device transmits hundreds of data points during login, including browser and operating system types, IP address, GPS location, VPN signals, and network configuration. Behavioral signals, typing speed, mouse movement patterns, swipe pressure, and navigation flow add an element of dynamism.

These signals are then fused together into a device fingerprint. A device fingerprint cannot be stolen or copied like a credential, and cannot be shared like a password. This fingerprint is then matched against historical fingerprint baselines and recognized fraud patterns to produce a real-time risk rating.

Device intelligence also plays an important role during customer onboarding. A single device submitting multiple applications under different identities, repeatedly attempting account creation, or appearing across known mule account networks can indicate synthetic identity fraud or organized financial crime activity. Identifying these patterns before an account is approved helps institutions prevent fraudulent actors from entering the financial system.

The outcome is a continuous, context-aware assessment. A login with valid credentials from a recognized device and a consistent behavioral pattern carries a very different risk than the same credentials appearing on a new device, behind a proxy, with no prior history and an unusual navigation pattern. Device intelligence automatically separates the two scenarios.

The Regulatory Pressure Compliance Teams Cannot Ignore

Regulators are moving more swiftly than many institutions understand. The European Union established the Anti-Money Laundering Authority (AMLA) in 2024, and it is set to commence its operations in 2025. The authority will directly supervise high-risk financial institutions and help member states coordinate enforcement actions. The EU AML Single Rulebook came into full effect on 10 July 2027 and will need consistent, intelligence-based customer screening.

In the USA, FinCEN is still encouraging the use of risk-based AML/CFT programs that enable institutions to identify new threats, enhance customer risk assessment, and enhance existing monitoring. Regulators are not mandating any particular technology, but are asking institutions to demonstrate that their controls are effective in detecting suspicious activity across ever-more digital journeys. The updated National Risk Assessment guidance by FATF mandates a more detailed, thorough assessment of financial institutions’ emerging risks, including those related to digital channels and device-level fraud vectors.

According to the FCA in the UK, 75% of regulated firms currently use artificial intelligence, and a further 10% intend to do so within 3 years. Regulators don’t specify mandatory fraud-prevention technology, but continually demand that institutions know what their customers are doing, recognize evolving risks, and maintain effective monitoring programs. Device intelligence supports these objectives by providing visibility into the environment behind account access and transaction initiation.

Where Compliance Programs Are Actually Failing

Transaction monitoring catches a pattern after it has started. This creates a specific and costly problem. Account takeover fraud is now the second-most common form of third-party fraud globally. Credential-stuffing tools allow attackers to automatically test thousands of stolen username-and-password combinations against a platform. Even with MFA in place, social engineering attacks can still bypass it. Once inside, a fraudster can initiate a payment, change a beneficiary, or extract funds before any downstream alert triggers.

False positives compound the problem further. Compliance analysts are already overwhelmed. Broad, rule-based alerts generate review queues that exceed team capacity and drive analyst fatigue. Without device context, teams cannot quickly distinguish a genuine customer traveling abroad from an attacker operating behind a VPN.

Device Intelligence for AML Compliance and Fraud Detection

Effective device intelligence for AML compliance means treating device signals as a first-class input to the risk decision, not an afterthought added after a transaction has already cleared.

A device intelligence layer evaluates whether the environment behind an account interaction has been manipulated. It can identify rooted or jailbroken devices, emulators, headless browsers, virtual machines, spoofed geolocation signals, and devices linked to previous fraudulent activity or multiple accounts.

Behavioral analytics provides valuable insights by examining factors such as typing speed, mouse movements, and overall device interactions. This approach enables the creation of unique profiles that are difficult to replicate at scale. Just as the automated bots and remote-access tools often reveal distinct patterns, even if they attempt to mimic human behavior. By combining device signals with network information, like shared IP addresses, proxy chains, and VPN services notorious for misuse, it’s possible to track not only individual sessions but also identify organized fraud rings.

An alert on a suspicious transfer carries very different weight when the compliance analyst can see that it originated from a new device, behind a data-center IP, with an emulator signature and a navigation pattern inconsistent with the customer’s past behavior. That same alert, with device context indicating a recognized device and consistent behavioral signals, can be resolved more quickly with a lower risk of misclassification.

For AML teams, this persistence is particularly valuable when investigating mule account networks and layered financial crime schemes. Device-level relationships can reveal links between accounts that appear unrelated through traditional customer data alone.

How AML Watcher Strengthens Risk Detection Beyond Device Signals

Device intelligence can identify suspicious sessions and account activity before funds move, but financial institutions still need a broader view of customer risk to make informed compliance decisions. Device-level signals become more valuable when combined with transaction monitoring, sanctions screening, adverse media intelligence, and ongoing customer risk assessment.

AML Watcher helps institutions build that wider risk picture through continuous monitoring across the customer lifecycle. The platform combines transaction monitoring, watchlist screening across 3,500+ global lists, sanctions intelligence updated every 15 minutes from 215+ regimes, adverse media monitoring across 5,000+ sources, and ongoing customer risk assessment to help compliance teams identify and investigate potential financial crime.

Building Stronger Fraud and AML Defenses

Financial institutions often discover suspicious activity only after a transaction has entered the review process. The challenge is gaining enough context early to distinguish legitimate customer behavior from account takeover attempts, mule account activity, and coordinated fraud networks.

AML Watcher helps compliance teams identify suspicious activity earlier, reduce unnecessary investigations, and maintain stronger oversight of customer risk throughout the customer lifecycle.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries