How Payment Service Providers Prevent Hidden Money Laundering Risk

Money Laundering

June 8, 2026

A payment service provider managed what seemed like countless small, routine transfers. The transaction volumes appeared typical, and the merchants successfully passed their onboarding checks. At no point did any alerts go off during this process. However, regulators later uncovered a sophisticated money laundering scheme hidden among the very transaction volumes that the PSP was supposed to oversee.

The European Banking Authority has stated that payment institutions lack sufficient rules to deter money laundering and terrorist financing. Their current anti-money laundering and counter-financing of terrorism controls are ineffective, especially in addressing the risks associated with these issues. Payment service providers are at the heart of global payment systems, which makes them particularly vulnerable and appealing targets for financial crime.

Compared with conventional banks, PSPs operate in a business model centered around speed, scale, and cross-border connectivity. Thousands of transactions can move through payment rails in seconds, often across multiple jurisdictions and merchant networks. That operational advantage poses a challenge for compliance teams, as criminal actors can conceal suspicious activity among vast numbers of legitimate payments, making illicit transactions difficult to identify unless risk-based controls and ongoing monitoring.

The real challenge for payment service providers lies not in understanding the rules, but in implementing controls that can match the speed of transactions, the growth of merchants, and the regulatory demands. The six strategies outlined below focus on the key areas where compliance programs typically struggle.

What Global Regulators Are Now Demanding From PSPs

Regulatory scrutiny of PSPs has shifted from guidance to enforcement, with major supervisory bodies increasing compliance standards and enforcement actions across the payments sector.

FATF continues to push member states toward risk-based Anti-Money Laundering supervision of payment institutions, with Recommendation 16 requiring the Virtual Asset Service Providers to collect and transmit originator and beneficiary information on transfers, a requirement now being applied to a broader range of payment providers.

The EU’s AML Package, comprising the 6th Anti-Money Laundering Directive (AMLD6), the Anti-Money Laundering Regulation, and the new Anti-Money Laundering Authority, will become directly applicable across all EU member countries by July 2027. The revised Funds Transfer Regulation has been in effect since December 2024. PSPs doing business in the European Union have a limited runway to build compliant systems before these obligations take effect.

FinCEN, under the Bank Secrecy Act, requires Customer Due Diligence and Suspicious Activity Report filings from payment processors operating in the US. The Federal Financial Institutions Examination Council has separately flagged weak Know Your Customer practices, including KYC for merchants’ customers (also known as KYCC), as core vulnerabilities in payment processor risk programs.

The UK FCA, Singapore’s MAS under Notice 626, and Australia’s AUSTRAC have each increased supervision intensity for PSPs. In 2024 alone, US regulators issued nearly 50 fines, with North America accounting for roughly 95% of the $4.6 billion in global financial penalties. Compliance teams dealing with payments are now facing enforcement as an immediate reality rather than a distant concern.

Where PSP Compliance Programs Break Down

Understanding what the rules require is easier than fixing the operational gaps that create exposure. Most PSP compliance failures trace back to four specific problems.

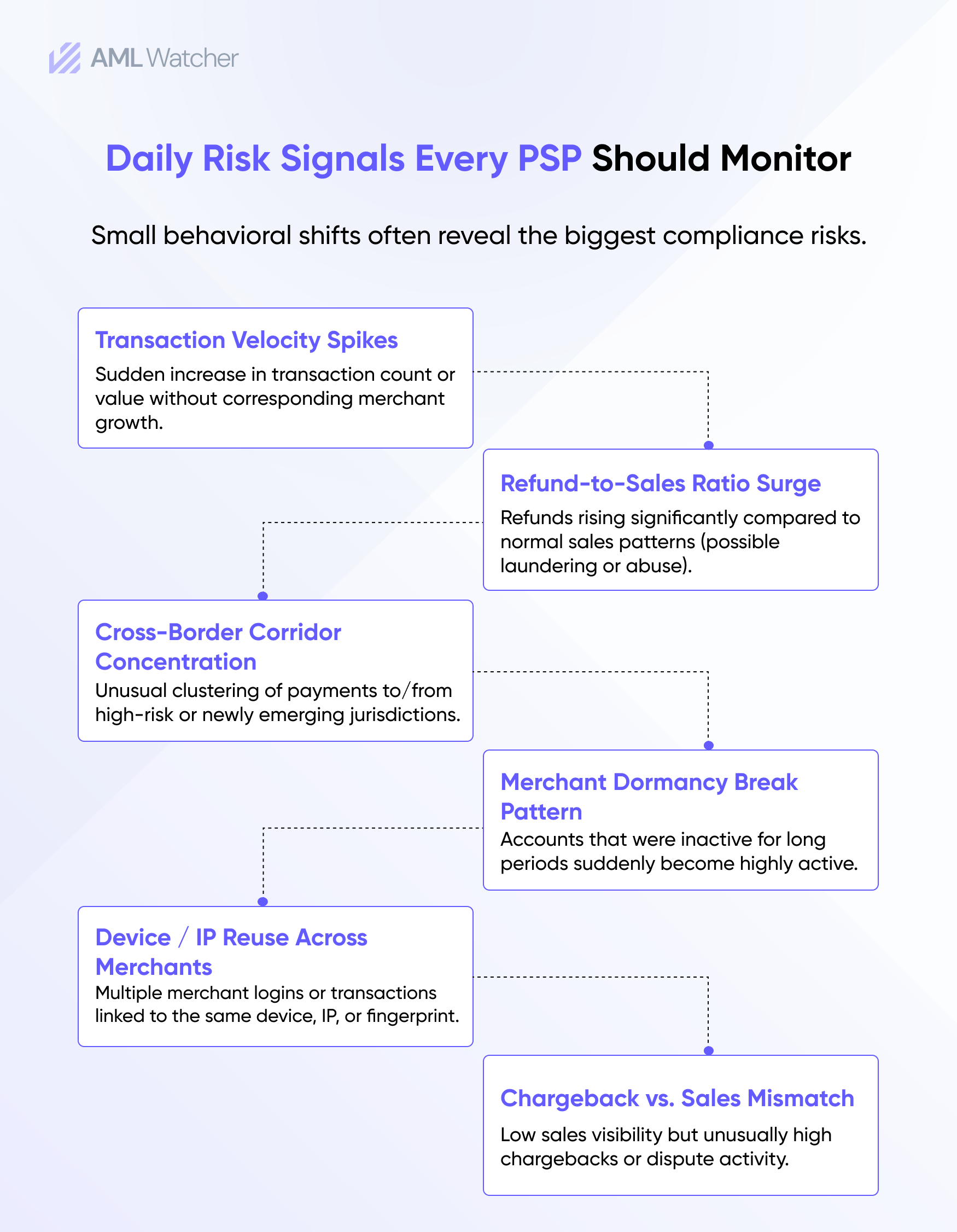

Transaction Volume Outpaces Monitoring Capacity

PSPs can process payments more quickly and at a greater scale than legacy rule-based monitoring can. Criminals exploit legitimate transactions to hide illegal ones. They make many transactions that appear normal but are actually suspicious. They also break up larger transactions into smaller amounts to avoid detection. Additionally, they move money among businesses and even use prepaid cards to disguise their funds. When the alert queue is full of noise, real risk gets buried.

Merchant Onboarding Creates a KYCC Blind Spot

A PSP does not just take on customer risk; it also takes on its merchants’ customer risk. Weak onboarding methods to verify business registration, but stop without evaluating the merchant’s own customer base, creating a gap that financial crime networks actively exploit. The FFIEC has specifically called this out as a high-risk vulnerability.

High-Risk Jurisdiction Exposure Goes Unmanaged

PSPs that do not restrict cross-border payment corridors or apply heightened scrutiny to countries where AML oversight is limited, AML supervision takes on regulatory exposure that is not offset by revenue. Facilitated transactions through high-risk countries do not just result in fines; they also cause reputational harm that customers and banking partners notice.

Siloed Risk Assessments Miss Layered Crime

When fraud, AML, and sanctions teams work in separate systems, they miss the connection between a structuring pattern, a watchlist hit, and an adverse media result that together point to the same threat and criminal activity. Viewing financial crime risks in silos is one of the most cited contributors to program failures.

6 PSP Compliance Strategies That Actually Reduce Exposure

1. Build a Risk-Based Approach With Real Teeth

A risk-based approach to PSP risk management is mandated by the FATF, but most implementations stop at documentation. The operational version needs to be tuned to customer profiles, transaction corridors, and merchant categories, not just a box ticked off for the regulators. PSPs that apply the same approach to all merchants lead to two blind spots: over-screening low-risk relationships and under-screening high-risk ones.

Risk scoring models need to take into account merchant category, transaction volume, geographic exposure, payment corridors, customer type, and historical behavioral indicators, rather than relying solely on static onboarding information.

2. Screen Payments in Real Time, Not After the Fact

For PSPs operating at scale, post-transaction review is too slow. PSPs often facilitate instant payment settlement, leaving little opportunity to recover funds once a sanctioned individual or illicit network receives payment. Real-time screening reduces this exposure by interrupting suspicious transactions before settlement occurs.

3. Implement Transaction Monitoring Built for Payment Patterns

Standard transaction-monitoring tools built for banking do not account for PSP-specific behaviors, seasonal merchant spikes, cross-border payment corridor patterns, or stored-value reload sequences. Criminals frequently exploit merchant networks, transaction splitting, and rapid fund movement across payment channels, behaviors that differ from those seen in conventional banking typologies. Monitoring platforms need typologies that reflect how money actually moves through payment rails, not generalized bank account patterns. Customizable detection rules that adapt to the transaction environment reduce both false negatives and the volume of false positives that bury compliance teams.

4. Close the Merchant Onboarding Gap With Structured KYC

Fraud prevention for Payment Service Providers starts during onboarding. That is why it is essential to verify a merchant’s identity and also to gain visibility into their customers and transaction patterns. Failing to address this can lead to issues later on, particularly when it comes to monitoring. Using risk scoring at the onboarding stage, along with tools such as adverse media checks, watchlist data, and behavioral analysis, sets a standard for ongoing monitoring. This method helps ensure compliance and makes it easier to defend during regulatory audits.

Furthermore, Merchant due diligence must include far beyond verifying the identities and business registrations. Payment service providers need to understand who really owns the business, where the funds come from, the types of customers involved, and what kind of transactions to expect. This matters most in sectors such as online marketplaces, gaming apps and sites, forex services, digital assets, and high-volume e-commerce, where customer risks can differ from those of merchants.

5. Apply Sanctions and Watchlist Screening Continuously

A clean sanctions screen at onboarding quickly loses value if it is not updated regularly. Therefore, the sanctions and watchlist screening must occur continuously, with real-time notifications of any status changes. In 2024, the European Union introduced 695 financial sanctions. Relying on periodic manual reviews to keep up with this many changes is not practical. For Payment Service Providers operating across multiple jurisdictions, ongoing automated re-screening is the only effective solution.

6. Assign Clear Accountability and Document Everything

Compliance programs need clear ownership. If no one is responsible for the ML/TF risk assessment, if no one checks how well the controls are working, and if there’s no record of screening decisions, the program will fail to meet regulatory standards, no matter how advanced the technology is. Senior management must take responsibility; there should be a clear risk appetite, defined escalation paths should be in place, and a structured case management workflow should be in place. These elements are not optional; they are crucial for turning a program into something that works rather than just a policy on paper.

Emerging Money Laundering Risks PSPs Cannot Ignore

Payment service providers face financial crime risks that extend beyond traditional structuring and sanctions evasion techniques. As criminals are now more likely to use mule account schemes, synthetic identities, and other marketplace payment systems to facilitate transactions using legitimate payment methods. The layered merchant relationships and complex payment ecosystems can also make it difficult to trace beneficial ownership and the transactional connections among criminal networks.

As embedded finance and digital payment platforms continue to evolve, the potential for security vulnerabilities has increased significantly. A payment service provider might successfully onboard a legitimate merchant without realizing that risky activities are occurring further down in the merchant’s customer network. These indirect exposure points are receiving more attention from regulators, who are increasingly requiring PSPs to demonstrate visibility into the entire payments journey, not just onboarding controls.

Payment orchestration platforms and embedded finance companies are creating additional layers between PSPs and end users. These models increase payment efficiency but can also lead to a loss of insight into customer behavior and beneficial ownership, posing fresh challenges for transaction monitoring and risk assessment.

Payment ecosystems are increasingly complex, requiring PSPs to adopt a unified risk control framework that integrates customer data, payment transactions, and sanctions data. This broader view helps identify hidden relationships and suspicious patterns before they develop into regulatory issues.

How AML Watcher Supports PSP Compliance Operations

Payment providers face growing pressure from regulators, banking partners, and customers to demonstrate effective financial crime controls. Programs that combine risk-based onboarding, real-time screening, and transaction monitoring are better positioned to detect hidden money laundering activity before it becomes a regulatory issue.

Many PSPs struggle to maintain that level of visibility as transaction volumes increase. AML Watcher supports PSP compliance with real-time payment screening across global sanctions, watchlists, and PEP databases, transaction monitoring built around payment-specific typologies, and AI-powered risk intelligence to help reduce false-positive review volumes.

AML Watcher helps payment providers strengthen customer due diligence, screen transactions in real time, and identify suspicious activity across complex payment ecosystems.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries