How to Ensure AML Compliance in Money Remittance and Exchange Services

Anti Money Laundering

July 16, 2025

- An Overview of the Remittance Industry

- FATF Guidelines for AML Compliance in Money Value Transfer Services

- FATF/MONEYVAL Typologies Report

- FATF Mutual Evaluation Report On Kuwait (Oct 2024)

- ML/TF Risk Assessment of UAE’s Remittance Sector

- AML Risks in Money Remittance Services

- Implementation of Enforcement Actions

- Best AML Practices For Remittance Service Providers

- How AML Watcher Addresses Challenges in the Remittance Sector?

An incredible $930.44 billion is expected to flow through digital money transfer services globally by 2026. This surge highlights the impact of speed and convenience offered by digital apps and online payment platforms. The exact features that attract customers also risk being exploited by the illicit actors.

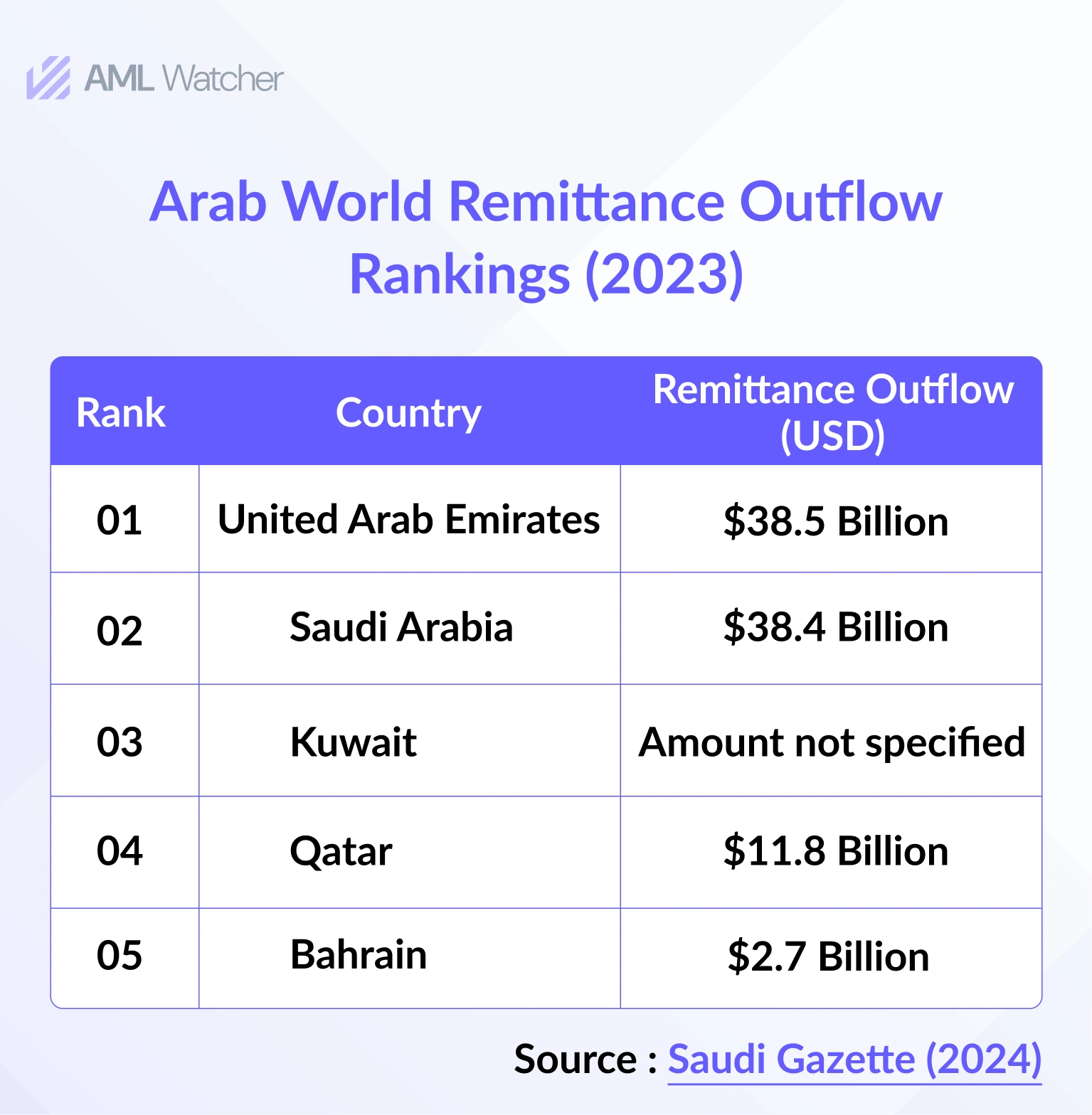

The risk of criminal exploitation of remittance is higher in some countries, due to factors like population demographics and geographic linkages. Some Gulf countries, such as Saudi Arabia, the UAE, Kuwait, and Qatar have large and growing remittance sectors due to their sizable expatriate workforces.

An Overview of the Remittance Industry

National Risk Assessments (NRAs) of certain countries and FATF Mutual Evaluation Reports have consistently pointed out that the remittance sector is highly vulnerable to financial crime. The FATF’s 2020 evaluation of the UAE highlights that informal remittance channels and the high volume of cross-border transactions make it difficult to perform thorough customer checks.

Likewise, the European Commission’s 2023 regulation on high-risk countries flagged nations like the UAE for having weak AML systems, leaving industries such as remittances open to criminal exploitation.

These reports highlight that without proper monitoring, rules, and regulations, the remittance industry becomes an easy target for illicit activity. People from South Asia and Africa work in these countries and send money through digital apps, making the region highly active in remittance transactions and exposed to financial crime.

Financial criminals take advantage of money remittance systems due to their speed, lack of transparency, and weak compliance rules, which increases the risk of currency exchange money laundering.

Due to limited regulation in some regions, Money Value Transfer Systems (MVTS) are an easy target for financial criminals to misuse. The FATF guidelines offer crucial recommendations for regulating MVTS to prevent financial crimes such as money laundering and terrorist financing.

FATF Guidelines for AML Compliance in Money Value Transfer Services

FATF Recommendation 14, as outlined in the Guidance for MVTS (2016), mandates that countries ensure all money value transfer services (MVTS) are licensed or registered to provide services and are monitored by the government to ensure remittance AML compliance with relevant FATF recommendations.

Countries should take stricter legal action, such as implementing sanctions, to stop MVTS that offer services without licenses or registration.

Companies should keep a record of all agents that provide money or value transfer services and ensure their registration with the relevant legal authority. These agents must be supervised to assess their compliance with AML/CFT rules.

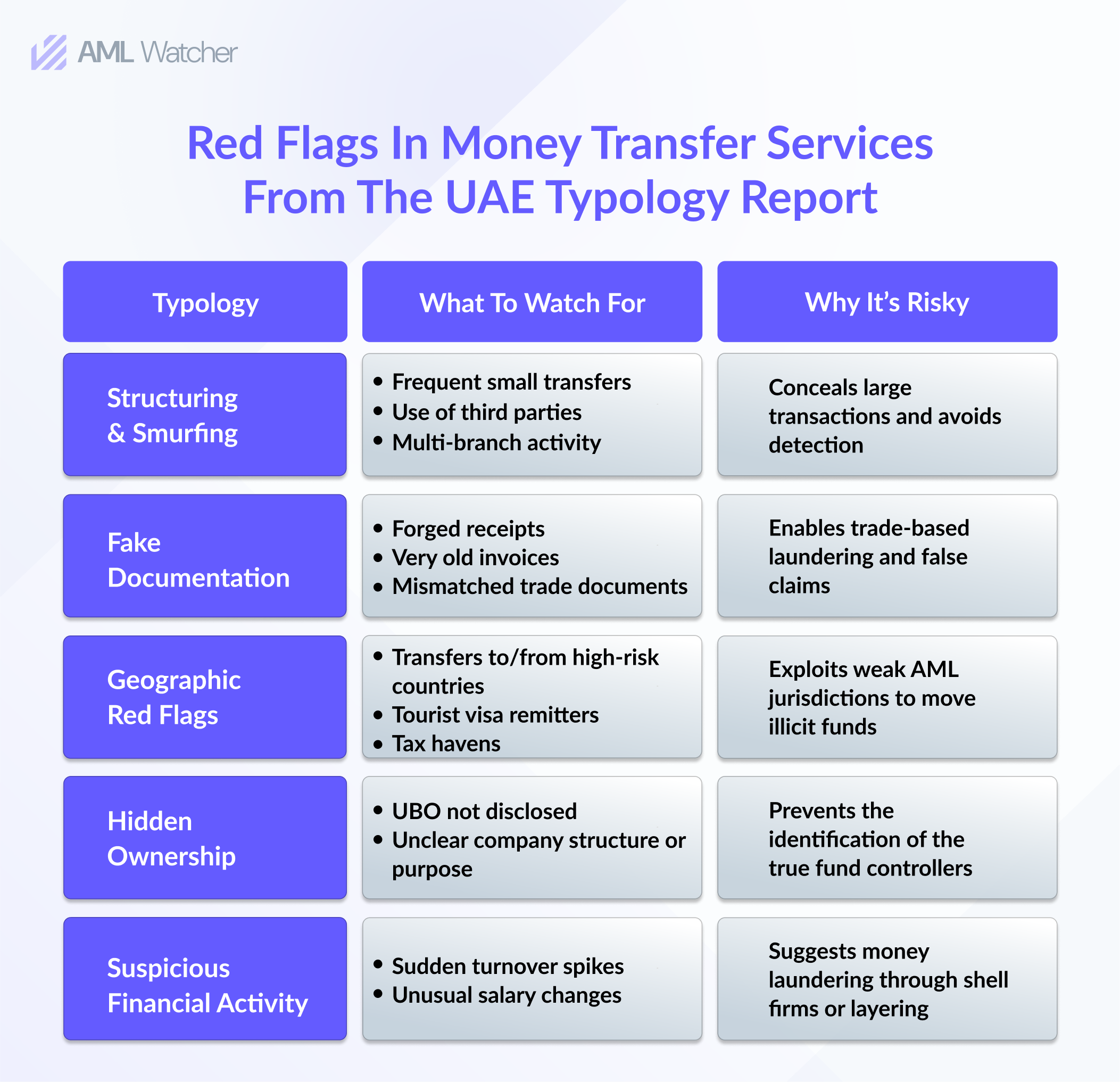

FATF/MONEYVAL Typologies Report

The FATF/MONEYVAL typologies report titled “Money Laundering through Money Remittance and Currency Exchange Providers” (June 2010) highlights the significant risks in the sector by showcasing real-world case studies.

Many case studies in the report show that money remittance and currency exchange businesses have been engaged in money laundering activities. Businesses were reported to have shown involvement in all three stages of the money laundering process: placement, layering, and integration.

Risks of money laundering and terrorist financing were linked with clients, owners, and agents. The cases also mention that the remittance sector is linked with facilitating other illicit activities, such as terrorist financing, fraud, human trafficking, smuggling, and drug trafficking, is also mentioned in the report.

One case involved a money transfer business that was used to funnel illicit funds to terrorist groups by layering multiple transactions across various jurisdictions. Another case involved a currency exchange business that unknowingly facilitated human trafficking by transferring large sums to individuals involved in illegal migration activities.

FATF Mutual Evaluation Report On Kuwait (Oct 2024)

The FATF Mutual Evaluation Report on Kuwait (October 2024) highlighted the vulnerability of the country’s remittance sector due to weak oversight of remittance agents and a reliance on manual compliance checks rather than automated ones.

Operators lacked proper AML training and were unsure of how to implement suitable Know Your Customer (KYC) procedures.

Identifying the beneficial owner of funds remains a challenge in the sector, which significantly raises the risk of financial crimes. Without proper identification, criminals can easily move illicit funds through remittance channels, obscuring their origin and circumventing detection by authorities, thereby facilitating money laundering and other illegal activities.

The report also highlighted the negligence of authorities and weak oversight in overseeing the remittance sector. Despite being aware of real cases, authorities did not take adequate steps to mitigate the risks of terrorist financing.

There was a lack of collaboration between agencies to combat financial crimes. In the context of remittance vulnerabilities, the National Risk Assessment (NRA) 2020 for the UAE also highlights similar challenges faced by the sector.

ML/TF Risk Assessment of UAE’s Remittance Sector

The National Risk Assessment (NRA) 2020 for the UAE identifies significant vulnerabilities in the remittance sector, particularly regarding blue-collar expatriates, who are at high risk of being exposed to financial crime, especially money laundering.

Low-income migrant workers are unintentionally involved in suspicious transactions by using cash-intensive exchange houses and digital money transfer services. These money transfer services might get exploited by financial criminals and unintentionally facilitate money laundering.

These channels handle a large volume of small and quick transactions with minimal checks, which escape detailed scrutiny.

Fines Imposed in the UAE on Exchange Houses

To reinforce compliance, the UAE has taken significant enforcement actions against non-compliant entities. The Central Bank of the UAE (CBUAE) imposed a 3.5 million dirhams fine on the exchange house as a financial sanction on June 23, 2025, for failing to comply with AML policies. It demonstrates the country’s ongoing commitment to maintaining the integrity of the financial system by following AML/CFT laws.

On June 24, 2025, the authority penalized another money exchange house with “2 million dirhams” for non-compliance with AML/CFT regulations.

According to Article 137 of Decretal Federal Law No. (14) of 2018, this penalty was issued. This law regulates financial institutions and the Central Bank in the UAE. The purpose of this legislation was to ensure that all exchange houses comply with the AML/CFT laws in the UAE.

The UAE has taken this series of actions to ensure that all licensed exchanges operating within its jurisdiction adhere to the regulatory regimes aimed at mitigating financial crimes.

AML Risks in Money Remittance Services

Money remittance and currency exchange services are vulnerable to financial crimes, such as money laundering and terrorist financing, due to their global reach and other factors. The following are some key risks:

-

High volume of transactions

Money Remittance & Currency Exchange providers deal with millions of small transactions on a daily basis. These transactions are complex to monitor for the detection of suspicious transactions and make them less transparent.

-

Digital Money Remittance Services

New money laundering ML risks are introduced due to the rise of technology in digital remittance platforms. Online money remittance services are becoming increasingly popular, raising concerns that authorities are not providing sufficient supervision, which could allow criminals to exploit. Non-bank remitters often lack an identity verification process, leaving a loophole for facilitation of illicit activity, which is a major red flag for money laundering.

-

Challenges in Client Onboarding

Many remittance compliance programs rely on local agents for client onboarding, and these agents often have limited knowledge of AML procedures. Due to a lack of AML training, they are unable to implement AML regulations in client risk assessment.

-

Money laundering risks in Prepaid cards

Some prepaid payment cards can be used for multiple purposes, such as sending or receiving money, or withdrawing cash from ATMs without providing your identity online. Some open-loop cards can be used internationally to transfer money, withdraw funds, pay for online services, or make in-store purchases without requiring face verification.

-

Regulatory Disparity

Criminals often target countries with weak regulatory rules, choosing them to bypass these checks. Cross-border money transfers raise the risk of violating anti-money laundering regulations when dealing with sanctioned or corrupt countries.

-

Quick Money Transfers

Criminals exploit the speed of instant transfers to move funds before deductions. Quick money transfers provide less time for real-time AML screening to detect red flags. Money transfer AML compliance ensures detailed AML screening and transaction monitoring to prevent criminals from exploiting remittance channels.

-

Risk of Money Mules

Money launderers often interact with third parties, known as mules, to solicit paid assistance or are forced into helping to conceal their identities. When mules pay on behalf of others, they protect the identities of the moneylenders.

-

Incomplete reporting

Some unregulated remittance money services usually do not submit suspicious activity reports due to poor practices, lack of oversight, and the risk of being caught. Thus, Authorities are unable to detect suspicious patterns and take time to prevent money laundering.

-

Exploiting the Ownership of the Remittance Sector

As remittance services are growing, money launderers may want to take ownership of a remittance company to bypass the AML compliance requirements. They can exploit the remittance sector by establishing their own remittance firm, partnering with an existing remittance firm owner, or utilizing an agent.

-

Using the Structuring Method

Money launderers may try to involve multiple remittance transactions using a structuring method. They transfer money to multiple locations to evade investigation and conceal the origin of the illegal funds. It makes it challenging for compliant and authoritative staff to assess illicit funds.

Implementation of Enforcement Actions

FATF Recommendations 14 & 15 for MSBs and VASPs

FATF has updated recommendations 14 and 15 to instruct Money Service Businesses (MSBs) and Virtual Asset Service Providers (VASPs), both of which play key roles in remittance transfer systems, to enforce AML/CFT measures such as customer due diligence (CDD), record-keeping, and obtaining proper registrations to mitigate risks.

UAE Central Bank Rulebook on AML/CFT

The Central Bank of the UAE’s Rulebook demonstrates the specific regulations for licensed exchange houses, such as conducting CDD, enhanced due diligence (EDD), beneficial ownership verification, and transaction monitoring to detect illegal activities.

UK FCA Oversight

The FCA, the UK’s Financial Conduct Authority, has increased Scrutiny of Small Money Transfer Operators (MTOS) to demonstrate their implementation of AML practices, such as having an adequate AML system to prevent financial crimes, including money laundering and terrorist financing.

Gaps Identified in MONEYVAL Reports

The Committee of Experts on the Evaluation of Anti-Money Laundering Measures (MONEYVAL) mentions the constant gaps in EU countries related to due diligence and reporting obligations linked to money transfer operators (MTOs). It highlights the requirement for improved supervision and remittance AML compliance.

Best AML Practices For Remittance Service Providers

The FATF mandates that financial institutions, firms, and remittance service providers must follow a risk-based approach to assess the money laundering risks associated with their clients. Remittance service providers should implement an AML program comprising the following features.

-

Customer due diligence (CDD)

Remittance companies must implement CDD procedures to verify the identity of their clients. Engaged due diligence is conducted for clients that may pose a higher risk, such as politically exposed persons (PEPs).

-

Transaction Monitoring

Money transfer or currency exchange firms should utilize advanced tools that automatically detect suspicious patterns and generate alerts. For example, if a person suddenly starts to send transactions exceeding the firm’s reporting threshold, or unusual patterns of transactions are detected, it might be linked to money laundering.

-

Suspicious Activity Reporting (SAR)

Transactions with high-risk countries are also flagged as suspicious activity, and a Suspicious Activity Report (SAR) must be generated and submitted to the relevant authority. Ongoing monitoring ensures that firms remain compliant with updated AML/CFT laws and regulations.

-

AML Screening

Clients must screen their clients and transactions against global watchlists and sanctions lists to mitigate financial crimes. Clients should be screened against the PEP list and also be monitored for links to adverse media sources. It identifies higher-risk clients and ensures that firms conduct only legitimate transactions that comply with AML regulations.

-

Appointment of Compliance Officer

Remittance firms must hire an efficient compliance officer to oversee the AML program with great expertise. A compliance officer can prevent breaches of AML/CFT rules and protect companies from reputational and financial loss.

-

AML training

The compliance team must be aware of AML/CFT roles and how they will be implemented effectively. For this purpose, employees must receive AML training in recognition drills to detect money laundering risks in a timely manner.

-

Internal audits and record keeping

Internal audits must be conducted to assess the effectiveness of implementing the AML framework, and records must be maintained of all transactions, including client data, in accordance with regulatory time requirements.

How AML Watcher Addresses Challenges in the Remittance Sector?

AML Watcher is the ideal solution for remittance service providers, where speed is critical. With diverse demographics to cater to, AML Watcher’s advanced name matching accuracy ensures comprehensive screening with minimal false positives, significantly reducing the time spent on manual reviews and accelerating compliance processes.

False Positives and False Negatives

Traditional AML software is unable to detect and often yields false positives and negatives results, whereas AML Watcher reduces false positives by 44% and false negatives by 44%, ensuring accurate screening results.

Real-Time Transaction Monitoring

Old and outdated AML solutions don’t offer real-time transaction monitoring and skip detection of suspicious activities. AML Watcher enables financial institutions to conduct customizable transaction monitoring with over 50,000 predefined rules.

PEP Screening

AML Watcher allows remittance to screen high-risk clients against PEP screening using 2.6 million PEP profiles across 235+ countries, assisting in enhanced due diligence.

Cost Efficiency

Transitional AML solutions lack the ability to provide streamlined processes and require excessive resources. AML Watchr reduces compliance costs by 50%.

Tailored Risk Scoring

AML Watcher provides precise risk assessment through customizable models that consider various factors, including transaction behavior, client data, and external indicators.

Comprehensive Data Coverage

It integrates with the existing systems and offers smooth operations covering comprehensive data from 60,000 data sources, including sanctions, PEP lists, and adverse media.

Biometric Screening

It utilizes facial recognition technology to screen users against potential matches with adverse media, sanctions, and PEP lists. This ensures zero false positives where biometric data is available.

Frequently Asked Questions

No, money laundering doesn’t always involve currency; while currency exchange can be one of the methods used by criminals to launder illicit funds.

Money launderers can utilize various channels, including digital transactions, real estate, and investments, to conceal the origin of illicit funds. Irrespective of whether they are in cash or other forms.

Move Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries