What is Payment Screening? Process, Challenges, and Solution

AML/CFT

August 26, 2025

Financial institutions process millions of payments every day. Many of these payments carry the risks of being associated with illicit activities such as money laundering and terrorist financing. This calls for effective payments screening because even a single missed hit can lead to sanctions evasion, fraud, or terrorist financing and consequently leads to penalties.

In July 2025, the Hong Kong Monetary Authority (HKMA) fined three banks HK$16.2 million for failing to flag illicit fund transfers.

An effective payment screening process is necessary to implement, for detection of suspicious transfers before they escalate into regulatory breaches. However, many financial institutions and payment service providers (PSPs) struggle with robust payments screening.

PSPs don’t have to comply with AML regulations only but they also have to comply with the domestic and international sanctions to prevent sanctions evasion.

What is Payment Screening?

Payment screening is a process that financial institutions and payment processors use to verify the sender and receiver of a payment to identify potential high-risk transactions. It involves checking payment details against:

- Sanctions lists (such as UN, OFAC, EU, UK OFSI)

- Watchlists (criminal, terrorist, or high-risk entities (PEPs))

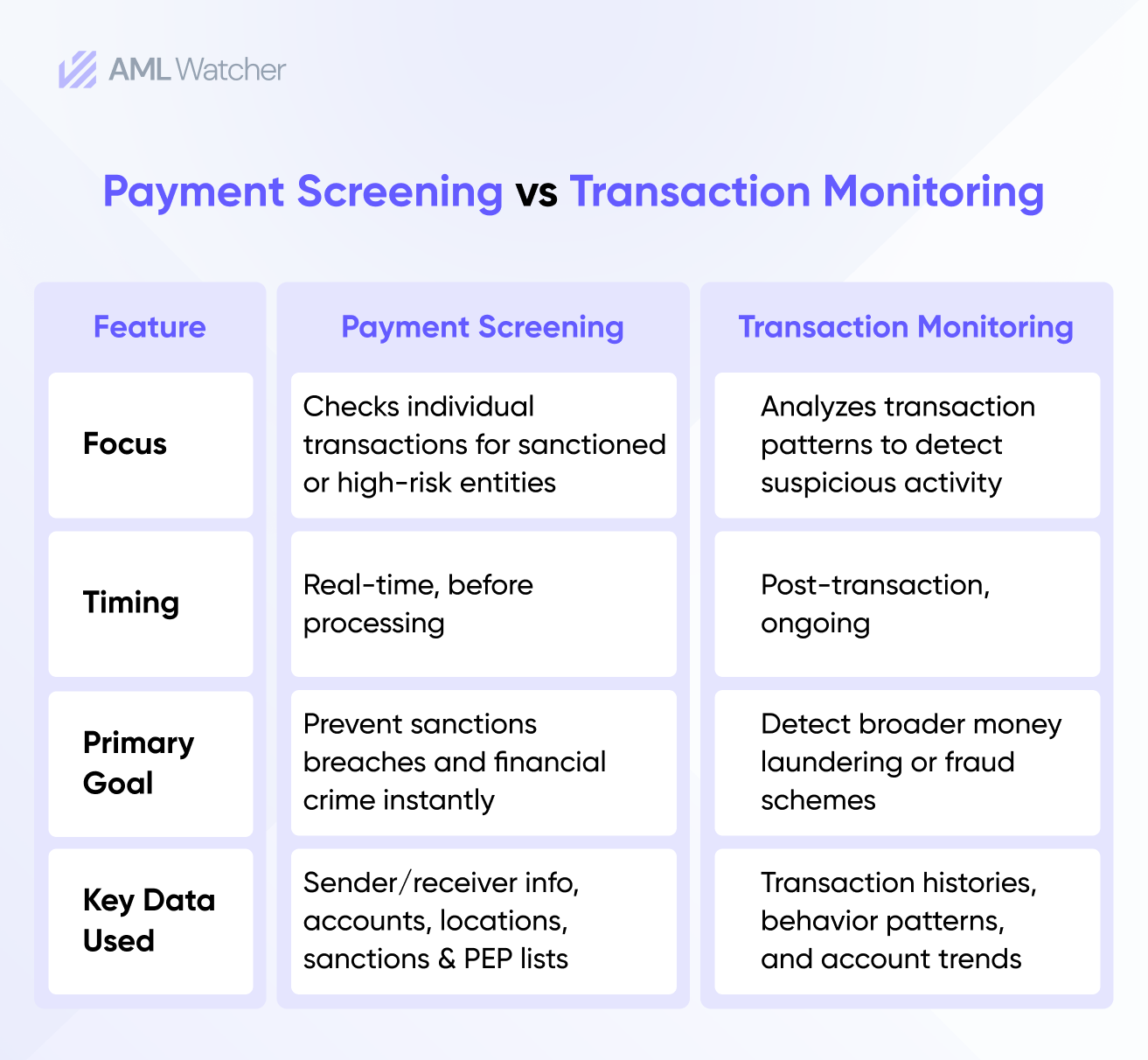

With real-time payment screening, organizations can block illicit transfers to protect financial integrity and avoid regulatory penalties. Unlike KYC (Know Your Customer), which focuses on identity verification of customers, payment screening targets the transaction itself, its originator, beneficiary, correspondent banks, and jurisdiction to assess the level of associated risk.

Payment Screening Vs Transaction Monitoring

Why Payment Screening is Necessary?

Whether you are in the fintech, financial sector, ecommerce, or cryptocurrency space, failure to screen payments accurately can lead to severe consequences, including heavy fines and sanctions.

In 2023, Binance paid a $968.6 million fine for violating U.S. sanctions for facilitating virtual currency transactions between U.S. users and individuals in sanctioned jurisdictions from 2017 to 2022.

This case is one of the largest settlements in sanctions enforcement history. It highlights the consequences of failing to screen payments against OFAC regulations.

For firms handling large international fund transfers, compliance with the payments regulations is necessary. These regulations ar designed to protect both customers and the organization itself from financial crimes and fraud abuse.

While Payments Service Providers do verify the identities of customers during onboarding, they still face the risk of facilitating money laundering, terrorist financing and sanctions evasion if they don’t screen the receiver, jurisdiction of recipient and the transaction amount.

Financial institutions worldwide are subject to many regulations and recommendations to safeguard the integrity of finance. However, the regulations may vary as per jurisdiction; they always require firms to monitor and screen the payments they have to process.

PSPs are not always required to do screening in order to follow the guidelines of Payments Service Providers only.

For instance, Travel Rule Compliance requires CASPs (Crypto Asset Service Providers) to collect and securely transmit specific identifying information for both the sender (originator) and the receiver (beneficiary) of a crypto asset transfer.

The EBA’s 2024 Travel Rule Guidelines emphasize that applying the Crypto Travel Rule ensures the ability to trace both the payer and the beneficiary of a transaction. By requiring CASPs to transmit this identifying information, the Guidelines also require firms to do the effective AML checks, as part of their compliance obligations.

FATF 40 Recommendations focuses on global AML/CTF standards, which mandate controls to detect sanctioned/high-risk entities and enhanced due diligence (EDD) for PEPs.

UK Sanctions and AML Act 2018 mandates screening for all payments to avoid sanctions breaches.

Major Challenges Organizations Face in Payment Screening

While payment screening mitigates financial crime risks, it brings several challenges, such as the following:

Speed and Customer Experience

The biggest priority for customers is speed with which transaction is processed. Digital transactions, particularly those by instant payments service providers are expected to be processed in milliseconds, but screening may slow down the process. It may result in frustrating customers and undermining the convenience that financial services promise.

High False Positives

Poor matching logic and unstandardized data often generate a large volume of false positives by flagging legitimate transactions. It creates heavy workloads for compliance teams with multiple manual investigations. Additionally, it results in increased operational costs and disrupts the customer experience by delaying payments.

Regulatory and Sanctions Updates

With constantly changing global sanctions, watchlists, and PEP databases, keeping screening systems up-to-date is a continuous challenge for financial sectors. Falling behind even slightly can expose institutions to significant compliance risks.

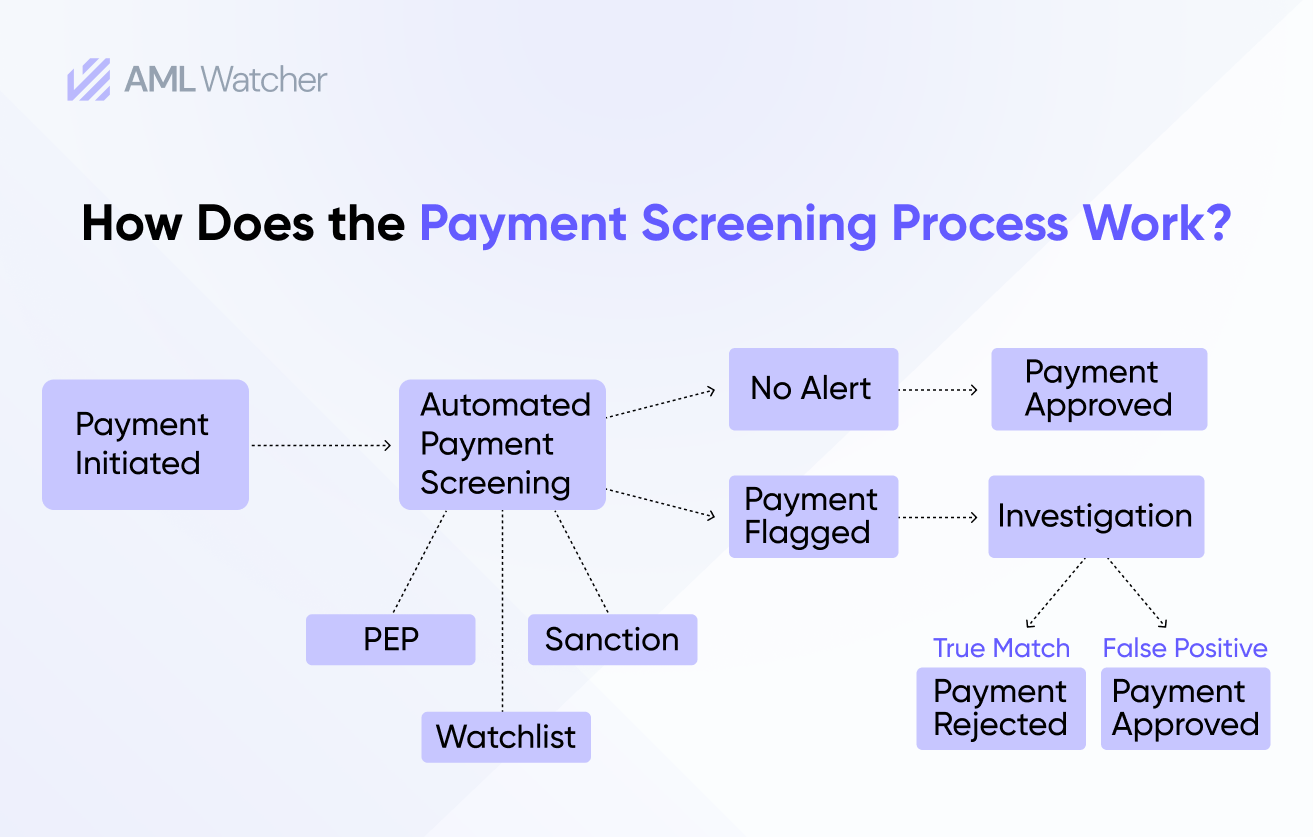

How Does the Payment Screening Process Work?

Data Collection & Verification

The screening process starts with the collection of some specific data about the payment and parties in transactions, whether domestic or cross-border. It includes the following key transaction details, which are necessary to check their legitimacy and correctness:

- Sender and receiver names

- Account numbers or identifiers

- Geographical locations

- Amount and currency

- Purpose of the payment

2. Parsing and Standardization

Before the screening process initiates, the system extracts and structures the relevant transaction fields. It ensures the correct formatting of all the details to prevent screening errors caused by variations in transliteration or missing information. This is done to reduce false positives, which burden compliance teams.

3. Sanctions Screening

Sanctions screening is the key step in the payment screening process. It includes a review of both sender and receiver information against global and domestic sanctions lists. It mainly includes:

- UN Security Council lists

- OFAC (U.S.)

- EU consolidated list

- UK OFSI

- Other country-specific and sectoral sanctions regimes

4. PEP & Watchlist Screening

PEPs can be prominent public officials or political persons with significant roles. Therefore, it’s important to assess the purpose of every payment a PEP makes, as their position puts them at a high risk of money laundering, corruption, embezzlement, and fraud.

The payment screening process reviews PEPs’ transactional activity to check if they are free from fraud and financial crimes. In addition, watchlist screening is performed within the process to check both sender and recipient against lists of known or suspected criminals, terrorists, or those subject to sanctions.

5. Risk Assessment and Evaluation

Not all payments carry the same risk; some are of low risk and some of high risk. Therefore, it is an important step in the payment screening process to determine the level of risk a payment may have. This process has customized templates with pre-defined thresholds that score risk and forward it for further investigation. There are certain red flags that the payment screening process may highlight for high-risk transactions. These red flags usually include:

- Unusual transfer of large sums

- Smurfing

- A large number of payments in short intervals

- Transfer of payments to an account in a country with low scrutiny of money laundering and fraud

6. Escalation and Reporting

If all the prior steps raise red flags that require further review, entities will then have to escalate the transfer to payments investigation through enhanced due diligence (EDD). It either results in determining the payment as suspicious for money laundering or fraud, or it can be approved for processing.

In case a payment, sender, or recipient is found to be suspicious with reasonable grounds, the process will proceed to reporting, the final step. Here, the firm needs to supply the corresponding documents to the relevant authorities.

How Can an Efficient Payment Screening Process Benefit Financial Institutions and Other Organizations?

Despite the challenges, the payment screening service remains a keystone of AML and Counter-Terrorist Financing (CTF) efforts. It delivers several benefits, such as the following.

Real-time Detection Prevents Fraud

Payment screening ensures real-time transaction monitoring, which detects and stops fraudulent activity before it is executed. It immediately flags suspicious transactions to prevent fraud and financial crimes.

Results in Regulatory Compliance

Payment screening ensures compliance with AML regulations. It involves checking sender and receiver details against sanctions lists, watchlists, and PEP databases.

Build Customer Trust and Satisfaction

In-depth screening safeguards customer transactions, enhancing confidence that their money is secure. This trust turns into stronger customer relationships with an organization.

Mitigates False Positives

Advanced payment screening systems detect irregularities that manual processes may overlook. This improves the accuracy of risk identification, leading to better decision-making and fewer false positives.

How AML Watcher Helps in Payment Screening?

Whether processing bank transfers, fintech transactions, or cryptocurrency payments, an effective screening service flags suspicious activities before they cause any harm. Effective payment sanctions screening is essential to block high-risk transactions, prevent financial crime, and maintain global compliance standards.

AML Watcher empowers financial institutions, fintechs, and crypto service providers to screen transactions in real time with:

- Crypto wallet screening for firms with digital-asset exposure.

- Comprehensive sanctions, PEP, watchlist, and adverse media data with global coverage and 80+ languages to reduce transliteration misses.

- Real-time updates as fast as every 15 minutes to keep pace with changing lists.

- Configurable risk scoring and ongoing monitoring to align with your risk appetite.

Move Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries