Neobank Fraud Risks Surge in 2026 as Digital Banking Threats Escalate

Fraud Prevention

May 22, 2026

AML enforcement across fintech and digital banking sectors has intensified in recent years, placing neobank compliance under increased regulatory scrutiny. This accelerated growth in customers also increases the risk of fintech and digital banking fraud, driven by fast onboarding, embedded finance, instant payment rails, and cross-border account access. Fraud networks now take advantage of the quick onboarding times, outpacing many compliance teams’ ability to catch suspicious activity.

So, what is a neobank?

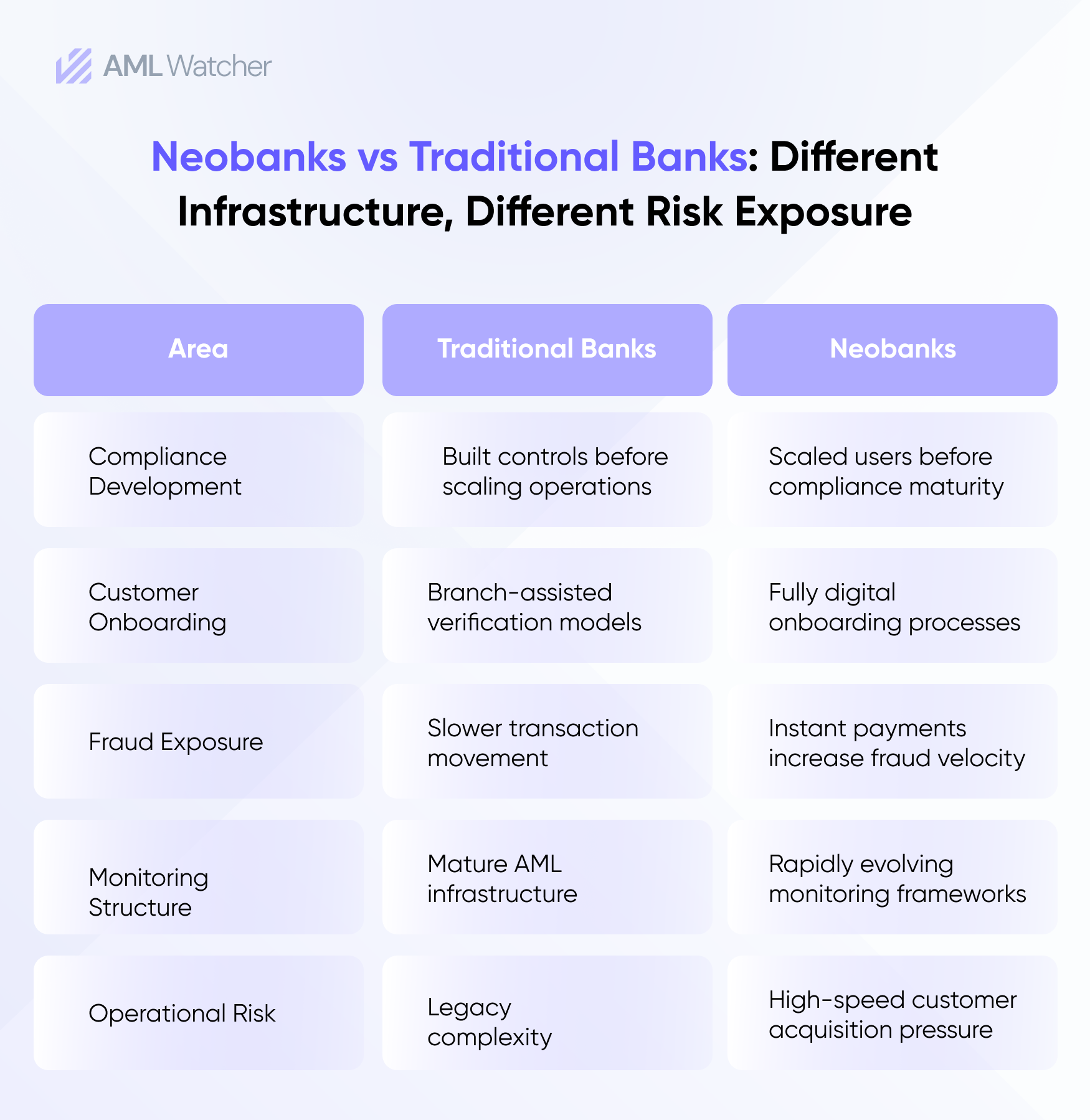

A neobank is a bank that operates without brick-and-mortar locations, primarily via mobile and online platforms. A challenger bank offers digital-first banking services and is a direct competitor to traditional banks.

The distinction between neobank and digital banks matters less to regulators because both face identical AML and sanctions obligations.

Regulators expect fintech AML compliance programs to detect AI-generated identity fraud, mule account activity, and sanctions exposure in real time. This article examines the operational weaknesses, regulatory pressure, and fraud typologies shaping modern neobank risk management in 2026.

Why Neobanks Became Prime Targets for Financial Crime

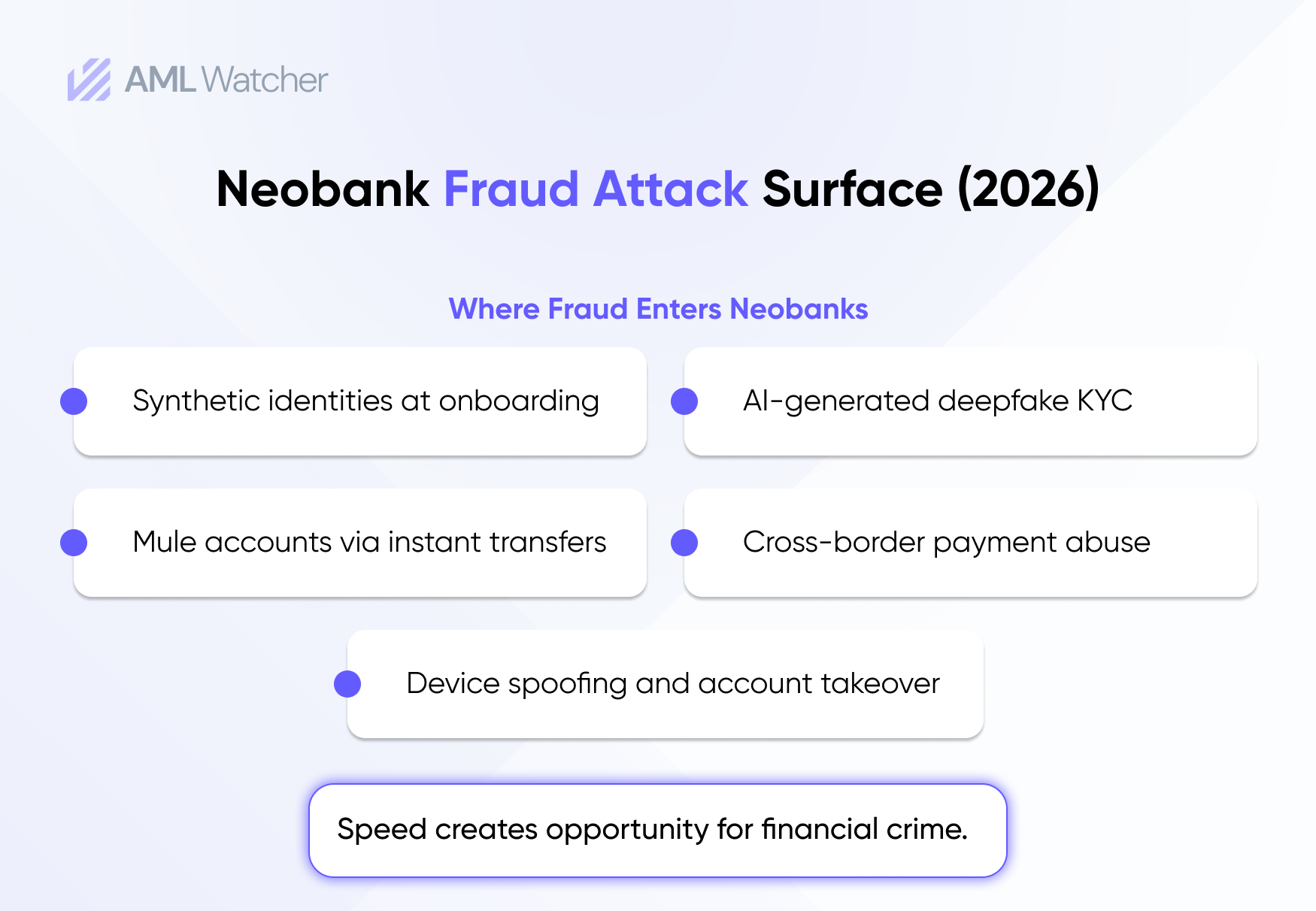

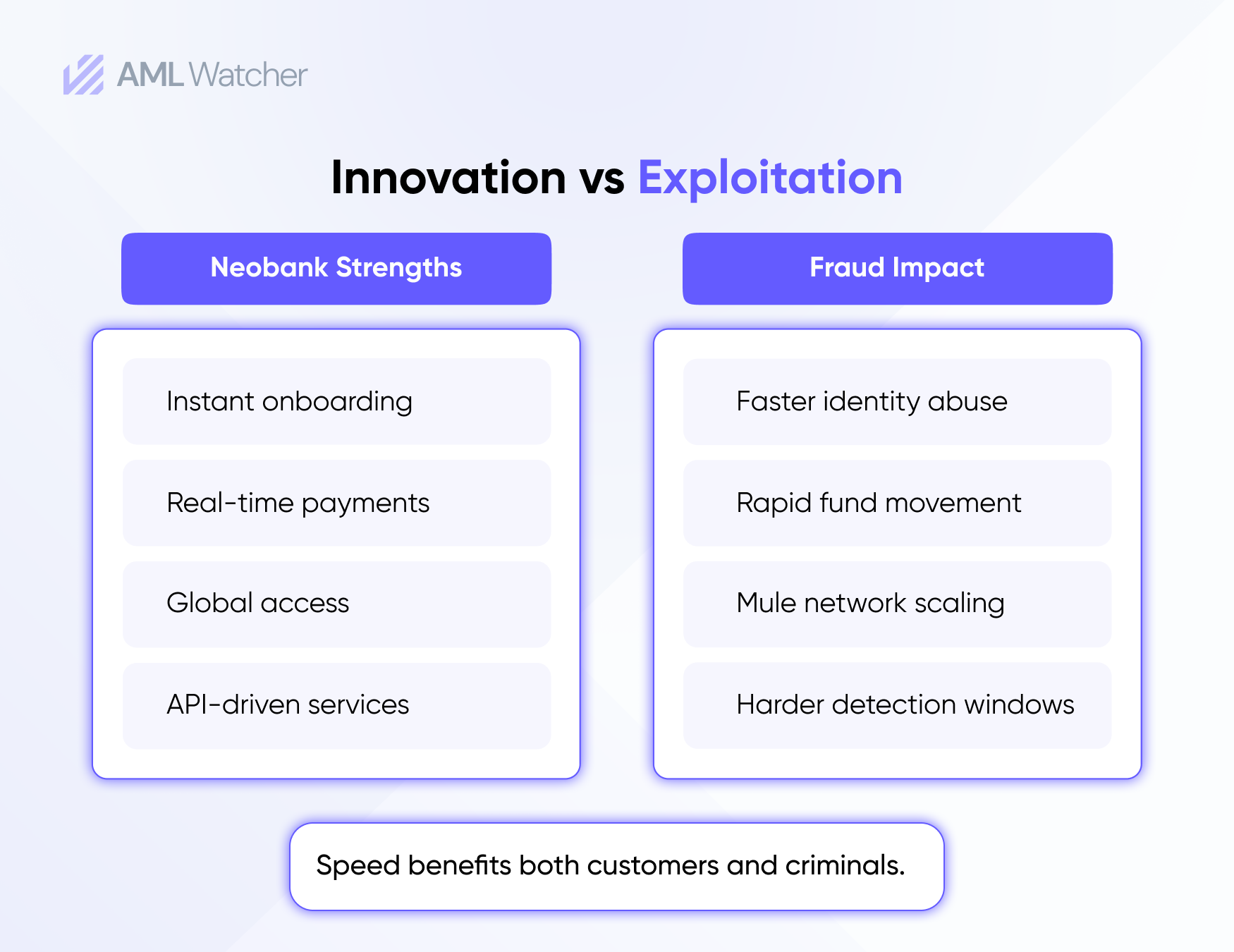

Neobanks expanded rapidly by removing friction from onboarding, payments, and account access. The convenience also provided an appealing opportunity for the financial crime networks to operate. Synthetic identity fraud is difficult to detect in a digital-first environment where thousands of applications are processed daily, with no multiple verification layers.

Instant account creation further increased mule account abuse across cross-border payment channels. Fraud groups now move illicit funds through temporary accounts before monitoring systems identify suspicious behavior. At the same time, embedded finance partnerships introduced additional compliance dependencies between fintech providers, sponsor banks, and Banking-as-a-Service platforms.

Automated mule recruitment is now expanded by using encrypted messaging platforms and social engineering as recruitment techniques.

The FCA’s enforcement actions shed light on the weaknesses in customer due diligence and financial crime controls of fast-growing neobanks.

The Global Regulators Increasing Pressure on Neobank Compliance

Regulatory pressure on digital banks is no longer reactive. Now, authorities are intervening at an earlier stage, investigating with greater strength, and expecting to see the results of controls. However, for neobanks operating across several jurisdictions, this has heightened the risk to fintech AML compliance programs.

In June 2025, the Financial Action Task Force (FATF) further enhanced Recommendation 16 by clarifying the scope of Travel Rule data to cover cross-border transfers. International payments require neobanks to send far more complete data from the originator and beneficiary, adding to the strain on transaction monitoring and identification processes.

Meanwhile, Financial Conduct Authority enforcement actions signal a tougher accountability model. The regulator is increasingly taking individual responsibility for AML and sanctions failures, following the £28.9 million penalty issued against a major neobank. This shift is changing perceptions of governance in neobank compliance.

In the U.S., the Financial Crimes Enforcement Network is continuing to remind digital-first institutions of their Bank Secrecy Act compliance responsibilities. Neobanks, even when using a sponsor bank, are required to have Customer Identification Programs, submit high-quality SARs, and provide proof of risk-based AML controls.

Several frameworks now define the operational baseline for fintech AML compliance:

- FATF Travel Rule updates requiring enhanced payment transparency

- EU 6AMLD expanding criminal liability and predicate offenses

- MiCA obligations introducing AML and custody requirements for crypto-enabled platforms

- MAS Notice 626 mandating CDD, EDD, and PEP screening

- Real-time monitoring expectations across high-risk payment environments

Regulators Are Moving From “Check-the-Box” AML to “Prove Effectiveness”

One of the key regulatory developments for 2026 will be the move from policy evaluations to effectiveness testing. It is no longer enough for regulators to find compliance manuals; if controls are proposed to lower real-world financial crime exposure, they are increasingly determining that they do.

Now, false-positive rates, investigation quality, SAR accuracy, alert resolution speed, and decision-making consistency based on risk are all examined. This development has resulted in operational performance, a central component of neobank compliance reviews.

BaFin restrictions against N26 established an early warning for the sector, while the Monetary Authority of Singapore continues enforcing strict onboarding and screening obligations under Notice 626. Overall, these actions confirm that fintech AML compliance has entered a far more measurable, enforcement-driven phase.

The Biggest Compliance Failures Inside Modern Neobanks

Rapid growth has exposed structural weaknesses across many neobank compliance programs. Several failures now appear repeatedly in enforcement actions, sponsor-bank audits, and fintech AML compliance reviews.

Weak Digital Onboarding Controls

Digital onboarding creates significant identity verification exposure when controls lack stronger contextual awareness and validation. Synthetic identities increasingly bypass onboarding workflows using manipulated credentials and fragmented identity data.

The onboarding process has become even more complicated due to deep fake KYC fraud. The dependence on fragile verification techniques is being challenged by fraud actors’ use of AI-generated selfies, synthetic voice generation, and fake identity documents. In many cases, document verification checks will only verify formatting, not the owner’s actual identity.

Transaction Monitoring That Cannot Handle Real-Time Banking

Many systems that are used for transaction monitoring were originally designed for slower banking environments with lower payment velocity. Modern neobanks process high transaction volumes within seconds, creating serious scalability problems for legacy rules engines.

Genuine mule account activity often disappears within alert noise, particularly during high-volume payment spikes. This operational gap remains a key contributor to digital banking fraud exposure.

Poor PEP and Sanctions Coverage

Global neobanks frequently onboard customers from jurisdictions with inconsistent sanctions and politically exposed person datasets. Incomplete screening coverage significantly increases regulatory exposure, particularly when ongoing monitoring controls remain weak or fragmented.

Missed adverse media signals and secondary political connections create additional fintech fraud risks across cross-border customer portfolios.

Fraud and AML Teams Working in Silos

Fraud teams typically monitor behavioral anomalies, device risks, and account takeover indicators. AML teams focus on identities, transactions, and obligations related to suspicious activity reporting.

When those systems operate independently, operational detection gaps emerge. The same actor may trigger fraud while bypassing AML controls without coordinating an escalation.

Sponsor Bank Oversight Is Becoming Stricter

Weak compliance programs create operational risk, reputational exposure, and compliance-related liability for sponsor institutions managing fintech relationships.

What Effective Neobank Compliance Looks Like in 2026

Meeting compliance requirements is essential in operating a neobank in 2026, and reaching that goal requires precision in operations, scalable systems, and tangible risk mitigation. Regulators increasingly expect fintech AML compliance programs to demonstrate effectiveness under real transaction pressure, not theoretical policy design.

Real-Time Risk Detection Instead of Static Rules

Static thresholds cannot effectively manage modern payment velocity or complex digital banking fraud typologies. Leading neobanks deploy adaptive monitoring models that continuously review how customers interact over time.

Behavioral analytics, velocity detection, and mule activity identification help compliance teams distinguish suspicious conduct from legitimate high-frequency activity. Risk scoring models also dynamically adjust based on transactional context, device intelligence, and shifts in customer behavior.

Continuous AML Monitoring Beyond Onboarding

Customer risk does not remain static after account opening. Triggers and material risk changes, adverse media monitoring, and dynamic PEP monitoring are all forms of effective fintech AML compliance.

Therefore, this approach helps reduce exposure to new sanctioned counterparties, new political affiliations, and new fraud networks.

Unified Fraud and AML Intelligence

Fraud and AML systems now require integrated intelligence sharing to increase detection accuracy. Device anomalies, chargeback spikes, and account takeover indicators provide a clearer understanding of AML risk-scoring decisions.

Shared risk signals help compliance teams identify coordinated financial crime activity earlier and with greater precision.

Lower False Positives Without Missing Real Risk

Operational efficiency has become a regulatory expectation. Reduces unnecessary investigations while maintaining detection quality through smarter screening calibration, contextual name matching, and risk-based alert prioritization.

Audit-Ready Compliance Infrastructure

Regulators increasingly expect structured investigation workflows supported by documented reasoning and explainable decisions. The new standard in scalable neobank compliance architecture is based on AI-driven compliance operations, centralized case management, and regulatory reporting.

How AML Watcher Helps Neobanks Strengthen AML and Fraud Controls

As customer volumes and fraud techniques have grown increasingly sophisticated, keeping attention on onboarding, screening, and transaction monitoring can be difficult for neobanks. Fragmented systems and disconnected risk signals can obscure emerging financial crime threats. AML Watcher helps neobanks with integrated screening and systems that track to boost risk visibility across all stages of customer engagement. Continuous data alignment across jurisdictions helps reduce gaps in sanctions and PEP coverage, while contextual matching supports more efficient alert prioritization and investigation workflows.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries