Alert!

Alert!

Top 3 Requirements of AML Compliance For Credit Unions

AML Compliance

November 3, 2025

- What Exactly are Credit Unions?

- Why Credit Unions Are an Attractive Target for Criminals?

- Recent Cases to Reveal Credit Union’s AML Vulnerabilities

- Top Requirements of AML Compliance For Credit Unions

- Key Steps to Build a Risk-Based AML Program

- Staff Training and Autonomous Testing

- Use of Automation and Outsourced Solutions

- Why is AML Compliance Important in this Case?

- How Credit Unions Can Enhance CDD Controls?

- How AML Watcher Empowers Credit Unions to Meet Modern AML Standards?

Credit unions are not frontline warriors against money laundering like mainstream financial institutions, but today, they are left with no choice. The regulators have raised expectations in response to these rising risks, making AML compliance for credit unions more essential than ever.

In the United States, the National Credit Union Administration (NCUA) is responsible for enforcing compliance expectations across the credit union sector. Its main emphasis is on whether the sector is meeting the federal AML and CFT standards.

Under the U.S. Code of Federal Regulations (eCFR), regulators expect credit union governance structures to adopt risk-based AML/CFT programs at a level comparable to banks, but supervisory approaches are personalized to each institution’s size and risk profile under NCUA rules.

Compliance with AML regulations is quite challenging for credit unions because they have to meet similar standards compared to the big banks, even though they have limited compliance staff, smaller budgets, and outdated systems. Furthermore, they also have to balance the compliance challenge with their member-centric goal and community trust.

Let’s dive in to know what the top three compliance requirements are that the credit unions must implement in the contemporary world.

What Exactly are Credit Unions?

Credit Unions, the member-owned financial institutions, operate in a similar way to banks but do not work for profit. They accept members’ deposits and typically offer lower loan rates, higher savings interest, or fewer fees.

Why Credit Unions Are an Attractive Target for Criminals?

In the U.S., federally insured credit unions now serve over 143 million members and hold about $2.37 trillion in assets (as of Q1 2025). Because of that large size, they are appealing targets for complicated financial criminals, especially as payments move faster, geographic boundaries for transactions blur, and regulatory gaps remain.

Further, there are many factors that contribute to weakness in the AML programs of the credit union. For instance, the FinCEN outreach report 2011 on depository institutions demonstrates that credit unions in recent years have expanded membership beyond their original affiliations and now handle international wires/remittances and shared-branch networks.

However, the legal terrain is evolving, for which enforcement agencies now expect even smaller institutions to maintain risk-based AML programs, perform strong customer due diligence, and continuously monitor member activity.

For community credit unions, this is a radical transformation; compliance must become a core necessity rather than just a checklist.

Recent Cases to Reveal Credit Union’s AML Vulnerabilities

In recent years, several U.S. credit unions have faced enforcement actions where weak AML controls enabled serious financial crime risks.

- North Dade Community Development FCU (Florida) was fined $300,000 by FinCEN for willful BSA violations tied to high-risk MSB activity, where nearly $2 billion in wires and remote deposits flowed through the institution. The NCUA later liquidated the credit union.

- Live Life Federal Credit Union (Michigan) received an NCUA cease-and-desist order in 2021 for cannabis-related AML deficiencies. It was required to deploy automated suspicious-activity monitoring and file timely SARs and CTRs; the order was lifted after remediation.

These illustrations highlight that both FinCEN and NCUA actively enforce AML expectations when programs are ineffective, regardless of an institution’s size.

Top Requirements of AML Compliance For Credit Unions

Below are the top three requirements of AML compliance for credit unions that matter most today.

Requirement 1: A Robust Risk-Based AML Program

Under the Bank Secrecy Act (BSA) and subsequent regulations, federally insured credit unions (FICUs) are required to have AML/CFT (counter-financing-of-terrorism) programs that are “reasonably designed” to detect and prevent money-laundering and terrorist-financing activities. As per National Credit Union Administration (NCUA) regulation § 748.2, a FICU’s program must include:

- written policies, procedures, and internal AML controls;

- designation of a compliance officer;

- Ongoing training for appropriate personnel;

- independent testing of the program.

Many credit unions are smaller in scale. The median asset size for FICUs in 2023 was only around US$56 million, but that means resources may be comparatively limited. Yet regulatory expectations remain.

Why AML Compliance for Credit Unions is Important?

The financial crime threat is no longer just about large banks or offshore players. Credit unions are part of the ecosystem, with many serving business members, digital accounts, and community organizations. Criminals may exploit perceived “smaller fish” for layering or placement of illicit funds. A weak AML program can expose a credit union institution to severe consequences such as regulatory penalties, credibility loss, and reputational damage. According to FinCEN’s joint statement on Risk Focused Bank Secrecy Act, regulatory bodies held their sole focus on developing frameworks that contain a risk-based approach in order to verify relationships and conduct customer due diligence.

Key Steps to Build a Risk-Based AML Program

-

Involvement of Board and Senior Management

The final say must be of the board for AML programs, and compliance officers are obligated to report directly to them and the audit committee.

-

Institution Specific AML/CFT Risk Assessment

Credit unions must conduct institution-specific AML risk assessments based on their operational footprint, services, and delivery channels.

-

Internal Supervision

Internal monitoring must be performed depending on the risk level of an activity. The activities that are at high risk are subject to stronger checks. Whereas, the credit unions at a small scale and often operating in less conflict areas can integrate shared services, or they can ask for third-party help. However, an outsourcing company will help manage finances; the credit unions are still accountable for the inefficiencies and failures.

-

Staff Training and Autonomous Testing

Credit unions must ensure their staff are trained on what the money laundering typologies are, know the top red flags, and how to file a suspicious activity report (SAR). They must also conduct testing of AML programs, which can either be internal or external, but should be done independently.

-

Use of Automation and Outsourced Solutions

Credit unions that are not large-scale and often operate in complex areas are required to integrate automated and outsourced solutions because of their limited internal capabilities.

Requirement 2: Customer Due Diligence (CDD) & Beneficial Ownership

Customer due diligence is performed on an ongoing basis by a financial institution to identify, authenticate, and learn about a client and their beneficial owners in detail.

Financial Crimes Enforcement Network (FinCEN) CDD Rule (31 C.F.R. § 1010.230) obligated the FIs to:

- Identify and verify the identity of customers;

- Identify and verify the beneficial owners of legal-entity customers;

- Understand the nature and purpose of the customer relationship to develop a risk profile;

- Conduct ongoing monitoring to detect suspicious activity and update customer information.

For credit unions, NCUA guidance emphasizes appropriate risk-based procedures for conducting ongoing CDD, including obtaining and analyzing member information, maintaining and updating member information, including beneficial owner(s) of legal-entity members.

Why is AML Compliance Important in this Case?

One of the fastest-growing threats in financial crime is the use of legal entities, shell companies, and beneficial-owner anonymity to move illicit funds. Credit unions may unwittingly open accounts for entities without fully understanding who ultimately controls them. Failure to identify the beneficial owner opens the door to layering and integration of criminal proceeds.

With the passage of the Corporate Transparency Act (CTA) in 2022, beneficial-ownership data is more accessible, but institutions must still integrate the information into their own CDD processes. Credit unions, though not always directly reporting under the CTA, will be able to validate BOI (beneficial ownership information) in FinCEN’s database.

How Credit Unions Can Enhance CDD Controls?

- Verification During Member Onboarding: When a company becomes a member, the credit unions are required to verify whether the entities behind that organization are real or not.

- Risk-Based Categorization: Credit unions must segment the entities depending on their risk score. Members should be checked after segmentation depending on their risk level.

- Enhanced Due Diligence for High-Risk Entities: If a member is a politically exposed person or someone with foreign ownership, the credit unions are expected to perform enhanced due diligence (EDD) on such an entity.

- Ongoing Monitoring and Updating information: Once the account is opened, credit unions must perform ongoing checks to trace the member’s transactions and update information in case of any changes.

- Record Keeping: Credit unions must keep records of due diligence processes, their decisions, and updates in line with the examiner’s expectations.

Requirement 3: Transaction Monitoring & Suspicious Activity Reporting (SAR)

Customer Due Diligence programs help with the initial client risk assessment. However, transaction monitoring through a feedback loop helps in assessing the actual associated risk. Continuous transaction monitoring is the next line of defense designed to identify unusual or potentially suspicious activity and trigger further investigation or SAR filing. Under the BSA/AML framework, credit unions must:

- Monitor transactions for potentially suspicious behavior.

- Maintain records and data to support alerts.

- File suspicious-activity reports (SARs) when appropriate (usually within 30 days of detection).

NCUA examiner guides emphasize that examiners will review federally insured credit unions (FICU) for internal controls, independent testing, compliance officer designation, staff training, and risk-focused monitoring.

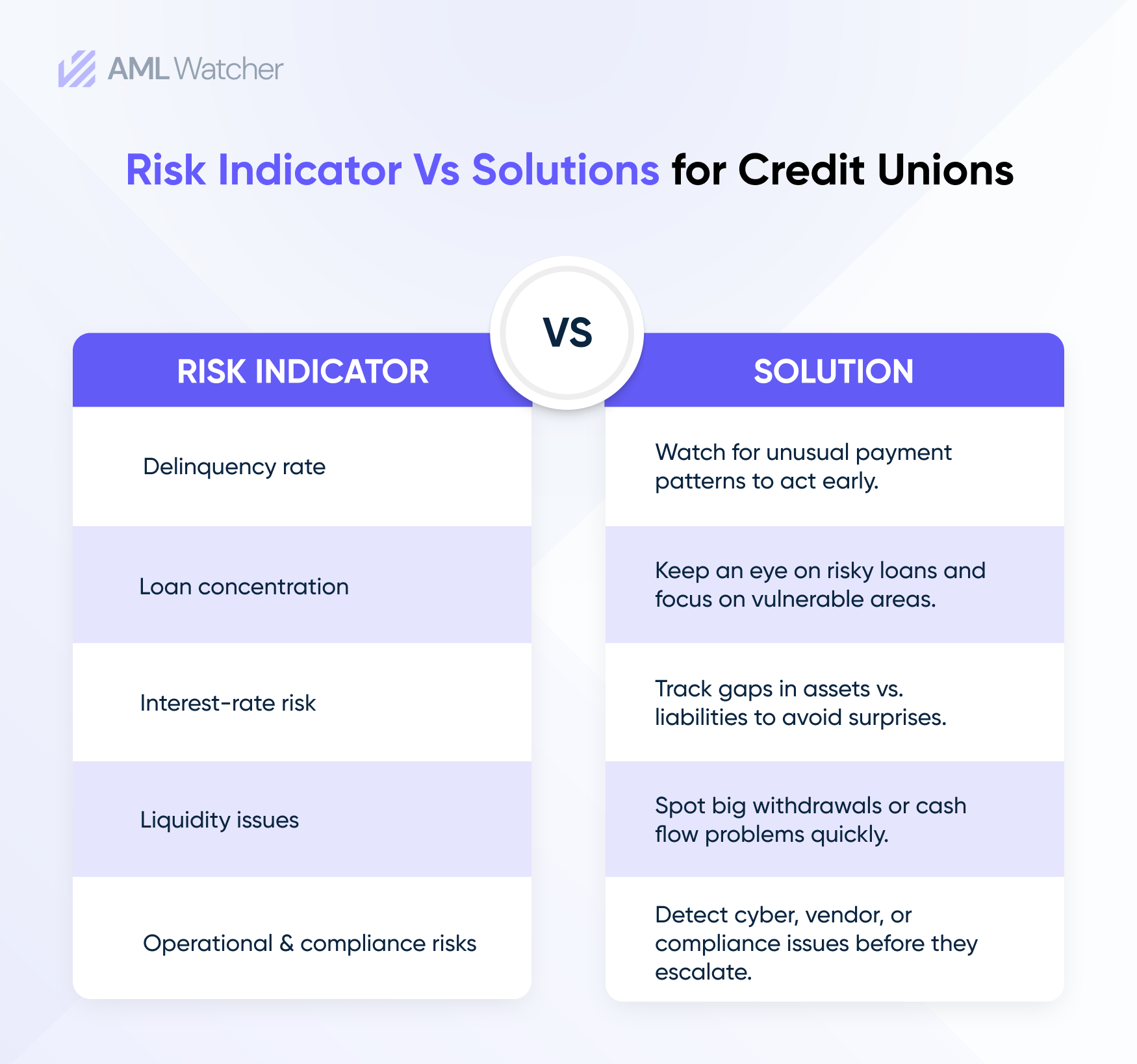

What are the Challenges of Compliance with AML in Credit Unions?

A major drag on compliance efficiency is false positives. Although publicly available data specific to credit unions is less frequent, studies of legacy AML systems show that up to 90 % of alerts are false positives, placing strain on limited compliance staff and diverting attention away from true threats.

Criminals exploit faster payment platforms, peer-to-peer (P2P) transfers, third-party service providers, and cross-border flows. These channels may be less well-monitored, offering vulnerabilities. If a credit union’s transaction-monitoring framework is weak, undetected movement of illicit funds can occur. This can lead to not only regulatory fines but also reputational damage and loss of member trust.

Key Steps for Smarter Monitoring and SAR Compliance

Credit unions should choose the transaction monitoring solution by considering the following aspects:

- Define alert-logic rules: Customize transaction-monitoring rules based on product, channel, and member risk profile. Tailor thresholds, patterns, unusual volumes, and entities.

- Use automation wisely: Even smaller credit unions should consider solutions that reduce manual burden, e.g., rule engines, segmentation, and prioritization of alerts.

- Escalation and investigation protocol: Have documented procedures for triage of alerts, review of exception reports, escalation to the compliance officer, and documentation of decisions.

- SAR filing process: Establish timelines, internal controls, and oversight (e.g., compliance-officer review) to ensure timely SARs with adequate context, linking to prior account/pattern history.

- Feedback loop and tuning: Regularly review alert performance (false-positive ratio, missed cases, time-to-resolution) and refine rules/parameters. Conduct periodic independent testing or review of the monitoring system’s effectiveness.

How AML Watcher Empowers Credit Unions to Meet Modern AML Standards?

Credit unions mostly face the same scrutiny as the big banks, but they lack resources and budget.

AML Watcher strengthens credit unions by making them fully compliant without stretching their budgets and teams.

Here is how AML Watcher helps credit unions in compliance with AML laws according to their needs.

- Customized risk scoring to check the score of each entity depending on its risk level.

- Ongoing monitoring to assist credit unions with emerging risks.

- Adverse media screening that highlights the negative news about potential clients and counterparties.

- Real-time updates every 15 minutes about the high-risk entities to track changes in sanctions, PEP, or watchlist.

Credit unions, faced with the challenge of complying with AML laws like big banks but with limited resources, can benefit from AML Watcher’s advanced features to meet compliance requirements aligned with their risk profiles.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries